This note was originally published at 8am on June 16, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“I'm just ready to move forward.”

-Tim Thomas

After watching a generational win for the Boston Bruins last night in Game 7 of the playoffs, I am sitting here in my hotel room watching a gorgeous sunrise in the Boston Harbor. It must be Lord Stanley’s way of smiling.

Was I smiling yesterday? Am I smiling this morning? Big time. We love winning here at Hedgeye. And we support anyone who has a transparent, accountable, and winning attitude. Our vision for American Optimism is as old as America itself.

Yesterday’s price action in markets did nothing but solidify our conviction in our Global Macro Themes:

- Growth Slowing (bearish on Wall Street/Washington US GDP Growth estimates)

- Deflating The Inflation (bearish on housing, stocks, and commodities)

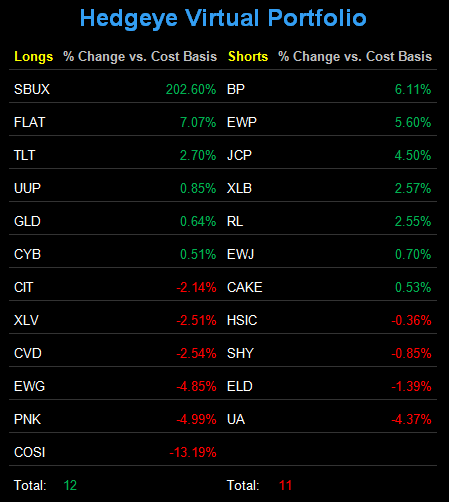

- Indefinitely Dovish (bullish on long-term Treasuries, UST Flattener, and Gold – TLT, FLAT, and GLD)

We’re not celebrating the other team’s losses - someone always has to lose (Goldman is bullish on commodities; JP Morgan is bullish on Equities, etc). We are championing a winning Risk Management Process that’s saving our clients from losing money in 2011.

Winning starts with not losing. It’s pretty difficult to lose if you don’t get scored on. Swedish offensive skills of the Sedin Sisters last night aside, defense won The Stanley Cup. Bruins goalie Tim Thomas was as focused as any professional athlete I have seen in a long time.

Focus, discipline, confidence – you either have it, or you don’t.

I certainly don’t have it all of the time. But the challenge isn’t to overcome my emotional capacity. The goal is to build a team and process that can pick me up when I am down. And Lord Stanley knows I’ve had my fair share of downs in life.

“I’m just ready to move forward.”

Yesterday’s wins are over with. Today we have to deal with today. It’s time to play the game that’s in front of us.

From a risk management process perspective, before we move forward, we always look back. We need to absorb what’s been priced into market expectations so that we can handicap what the probabilities are for prices to change.

From an immediate-term TRADE perspective, oversold lines in Global Equities are now as follows:

- SP500 = 1261

- Nadaq = 2613

- Russell2000 = 771

- Japan’s Nikkei = 9367

- China’s Shanghai Composite = 2661

- India’s Sensex = 18,066

- UK’s FTSE = 5662

- Germany’s DAX = 7011

- Spain’s IBEX = 9811

- Brazil’s Bovespa = 61,109

From an immediate-term TRADE perspective, oversold lines in Commodities are:

- WTIC Oil = $94.70

- Copper = $4.07

- Gold = $1520

From an immediate-term TRADE perspective, oversold line in US Treasury Yields are:

- 2-year UST Yield = 0.36%

- 10-year UST Yield = 2.91%

- 30-year UST Yield = 4.15%

The corollary to oversold bond yields, of course, is overbought bond prices – so, while it’s popular for US stock market centric pundits to trash anyone who isn’t Perma-Bullish on “stocks for the long run”, we’re quite happy that they wake up every morning thinking that way. There’s always risk to be managed somewhere. Being bullish on bonds yesterday was a big win.

There are winners and whiners in this profession. We subscribe to the principles of the former. Being Perma-Anything generally doesn’t work. In the last few years I have written a few Early Look notes about Bears and Bruins:

- “Bullish Bruins” = April 17, 2009 (when we went bullish on US Equities – bought SBUX April 21, 2009)

- “Ragingly Bullish Bears” = May 5, 2011 (when we pressed the short case for Growth Slowing)

What’s interesting about the timing of the “Ragingly Bullish Bear” note is how quickly sentiment has changed. In that May 5, 2011 missive I highlighted the following sentiment setup in the II Bullish-to-Bearish survey:

- Bulls up 100 basis points week-over-week to 55%

- Bears down 200 basis week-over-week to 16.5%

- The Spread (Bulls minus Bears) widened by 150 basis points week-over-week to +38.2% for the Bulls

Again, relative to itself, there are a few critical risk management callouts in this long-dated survey to consider:

- Bulls are not ragingly bullish

- Bears are not allowed to be bearish

- The Spread between Bulls and Bears is only 200-300 basis points from its all-time wides (all-time is a long time)

“All-time “wides” is risk management locker-room speak at Hedgeye for something you don’t want to mess with – kind of like being a man dressed in orange last night drinking a smoothie with your i-pod on in the bowl of the Boston Garden – it’s just a bad position to be long of.”

Back to today…

The only worse position to be “long of” was probably a Blue/Green Canucks jersey at a bar in Boston last night. This morning, the good news for Perma-Bulls (US stocks) is that this morning the II Bullish-to-Bearish Spread has narrowed to +11% for the Bulls (37% of people now admit to being Bullish and 26% being Bearish).

That’s a huge narrowing of an exceptionally wide spread. But my and the Boston Harbor’s Smiles are still beaming.

My immediate-term support and resistance ranges for the Gold, Oil, and the SP500 are now $1520-1554, $94.70-99.58, and 1261-1281, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer