TODAY’S S&P 500 SET-UP - June 21, 2011

The USD down = Commodity and Stocks up, but lower-highs on low volume across the board. Is the USD is back down for the week-to-date because:

A) Bernanke has his US Dollar Devaluation Presser in the next 48hrs?

B) Eurocrats are finding a way to hold $1.42 EURO/USD support?

We will get more bullish on Global Equities (China in particular) if the USD strengthens and we Deflate The Inflation - not the other way around. As we look at today’s set up for the S&P 500, the range is 32 points or -1.51% downside to 1259 and 0.99% upside to 1291.

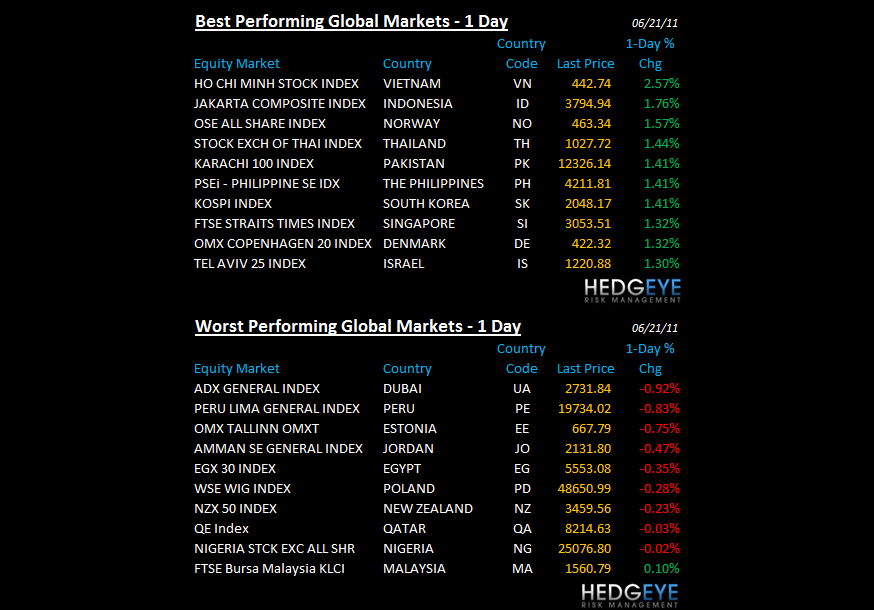

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1069 (+296)

- VOLUME: NYSE 786.44 (-50.99%)

- VIX: 19.99 -8.51% YTD PERFORMANCE: +12.62%

- SPX PUT/CALL RATIO: 1.65 from 2.03 (-18.51%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.12

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 2.97 from 2.94

- YIELD CURVE: 2.59 from 2.56

MACRO DATA POINTS:

- 7:45 a.m./8:55 a.m.: ICSC Retail/Redbook Retail

- 10 a.m.: Existing home sales, est. 4.8m (-5.5% M/m)

- 11:30 a.m.: U.S. to sell $58b in 4-wk bills

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- Germany June ZEW economic sentiment (9.0) vs consensus (2.0) and prior +3.1;Germany June ZEW current conditions 87.6 vs consensus 89.5 and prior 91.5

- Greek Prime Minister George Papandreou faces a confidence vote in his government

- Jon Huntsman to announce he’s running for president

- Spain Sells 2.4b Euros of 6-Month Bills - Avg 6-mo. yield 1.776% vs 1.766% at May auction.

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Copper Imports by China Slump 47% as Consumers Prefer to Drain Stockpiles

- Oil Gains a Second Day as Euro Crisis Eases, U.S. Crude Supplies Seen Down

- Copper Rises From One-Week Low on Reduced Concern About Greek Debt Default

- Pork Prices in China Seen Staying at Highs as Domestic Shortage Persists

- Raw Sugar Falls on Forecast for Increased Thai Production; Cocoa Advances

- Corn Gains After Slump as Flooding Threatens China Crop Amid Rising Demand

- Gold May Advance as Weaker Dollar, Greek Debt-Default Concern Spur Demand

- Qaddafi Tanks Deprived of Diesel as Ships Shunning Libya: Freight Markets

- Australia Keeps Sugar Forecast as Cyclone Damage Offsets Increased Acreage

- Russia Fails to Win Back Egypt, World’s Biggest Wheat Buyer, After Halt

- Rubber in Tokyo Declines to One-Month Low on Concern Demand Remains Slow

- Rubber Production in India Jumping 22% as Car Sales Fuel Demand for Tires

- Crude Supplies Fall in Survey as Gasoline Output Increases: Energy Markets

- China’s Rare Earth Quotas May Limit Supply to Japan, Europe, Lifton Says

CURRENCIES

EUROPEAN MARKETS

- EUROPE: green across the board, but on low-volume to lower-highs; DAX back above my 7139 TREND line; Spain and Greece below TREND lines

- S&P reaffirms view it would likely treat voluntary debt restructuring for Greece as a default, Moritz Kraemer, head of European sovereign ratings tells Die Welt

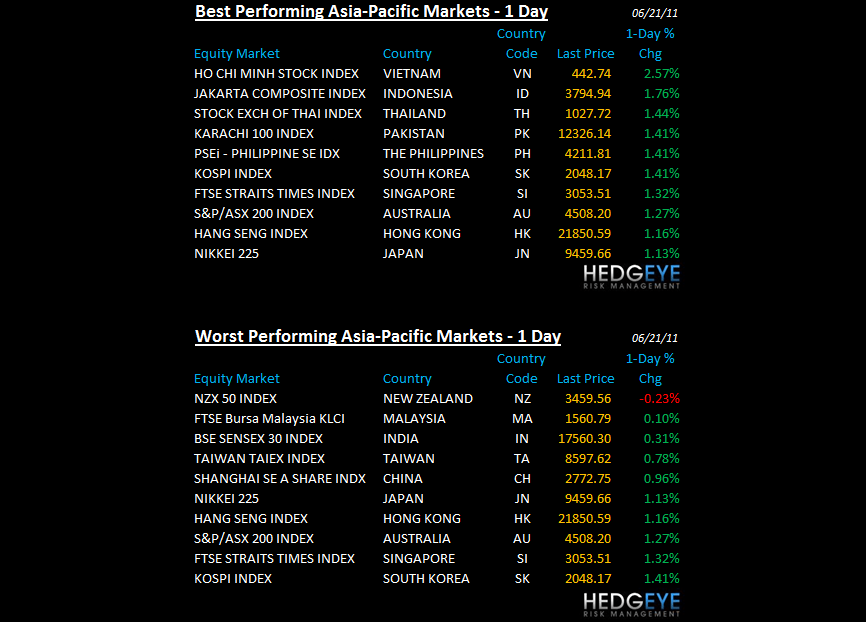

ASIAN MARKETS

- ASIA: green across the board, with China (which we just bought) up +1% and India finally stopped making lower-lows, +0.33%.

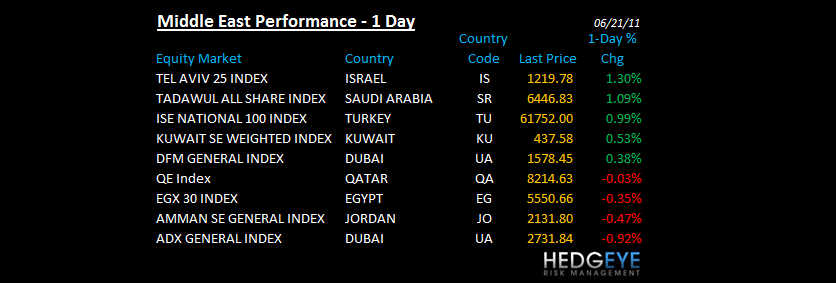

MIDDLE EAST

Howard Penney

Managing Director