TODAY’S S&P 500 SET-UP - June 17, 2011

Politicians may be market morons, but they understand career risk management. The Euro finding a bid this morning tells us the immediate-term TRADE coming out of this weekend's European meetings is UP to 1.43-1.44. That's why we sold our long USD position yesterday (I want to buy it back lower).

Overall, the dominating intermediate-term TREND of Deflating The Inflation (housing, stocks, commodities) remains - but today's prices finally started to show some quantified exhaustion in the Hedgeye immediate-term TRADE models (VOLATILITY = overbought; VOLUME studies = oversold). I'm looking for the SP500 to hold 1260 - and if it does, we could easily see another immediate-term +2.5-3% short covering rally.

Our favorite 3 sectors remain (in this order):

1. Healthcare (XLV)

2. Utilities (XLU)

3. Consumer Staples (XLP)

On the short side, we covered Basic Materials (XLB) on the down move and wouldn't short any sector until we see 1260 tested and the bounce. All of the Hedgeye TRADE and TREND levels are attached in the spreadsheet. Call sales@hedgeye.com if you have any questions. As we look at today’s set up for the S&P 500, the range is 18 points or -0.60% downside to 1260 and 0.82% upside to 1278.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -320 (+1778)

- VOLUME: NYSE 1050.56 (-1.71%)

- VIX: 22.73 +6.61% YTD PERFORMANCE: +28.06%

- SPX PUT/CALL RATIO: 1.92 from 2.86 (-32.95%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.09

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 2.93 from 2.98

- YIELD CURVE: 2.55 from 2.60

MACRO DATA POINTS:

- 9:55 a.m.: UMich Consumer Confidence, est. 74.0, prior 74.3

- 10 a.m.: Leading indicators, est. 0.3%, prior (-0.3%)

- 1 p.m.: Baker Hughes Rig Count

WHAT TO WATCH:

- Texas state court hearing in suit between AMR/Sabre over Sabre’s attempt to move entire action to federal court

- Basel Committee considering extra capital requirements of as much as 3.5%: two people familiar with talks

- Vice President Biden and U.S. lawmakers determined to find $4t in savings, Biden tells reporters after group’s third closed-door meeting this week

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- UBS Limits Commodities Hiring Expansion as Boom Leaves Scarcity of Talent

- Food Prices Will Stay High for Next Decade on Slowing Output, UN, OECD Say

- Oil Heads for Biggest Weekly Decline in Six on Concern Over European Debt

- Soybeans Fall to Lowest Price in a Month on Slowing Chinese Import Demand

- Gold Drops on Strengthening Dollar, Selling to Cover Losses in Commodities

- Sugar Advances on Increasing Demand Before Ramadan; Coffee Prices Climb

- Copper May Decline for a Third Day on Concern About Greece’s Debt Crisis

- India Rules Out Ending Ban on Wheat, Rice Exports as Food Demand Increases

- Oil’s Declines in Middle East Show No End on Saudi Offers: Energy Markets

- Commodities May Decline 3.3% as S&P Index Falls Short: Technical Analysis

- Mongolia to Offer Tavan Tolgoi Coal Mine to ‘3 or 4’ Bidders, Batbold Says

- Defunct Gold Mines Lure Investors on New Technologies, Record Price Gains

- Blood-Diamond Curbs Imperiled for De Beers, Tiffany by Zimbabwe Violence

- Gold May Climb Next Week as Europe’s Debt Criss Spurs Demand, Survey Shows

CURRENCIES

EUROPEAN MARKETS

- EUROPE: gong show continues; we're covering all shorts into the weekend though and going naked long (and worried) Germany; Greece crashing.

ASIAN MARKETS

- ASIA: end of darkness? awful week for Asian equities; we are getting long China on fear; staying short Japan on reality

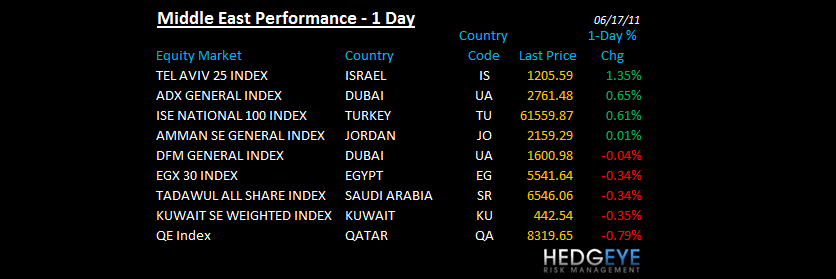

MIDDLE EAST

Howard Penney

Managing Director