Following management’s recent visit to NYC, I spent some quality time with the CAKE model and here are some of my initial thoughts.

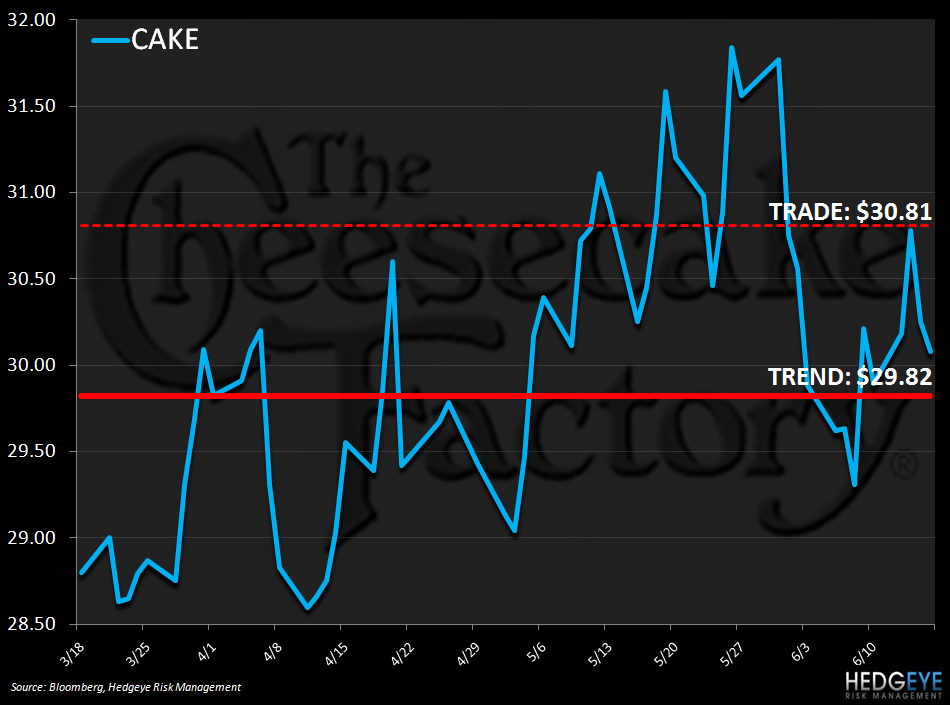

Keith covered CAKE in the Hedgeye Virtual Portfolio today. I remain bearish on the fundamental side of the stock. Below are some key details to my perspective:

- I am coming in a little higher than guidance for Q2 and then closer to the low end of guidance for the FY.

- I think they can probably do more than their guidance of "at least $100M in share repurchase” given that high ending cash balances.

- Relative to recent trends, CAKE's comparable restaurant sales guidance seems reasonable.

- The bakery sales line slowed significantly in 1Q (on a 2-year average basis); the economy is keeping this business at bay.

Here a few other important things to remember:

- CAKE has an extra week in Q4

- They are doubling openings in FY11, which will impact preopening expense and capex; two important items that are hardly ever factored in correctly by consensus.

I still favor cake on the short side, particularly on any strength.

Howard Penney

Managing Director