Everyone has to eat. The question is, do they eat at home or eat out?

On today’s Kroger conference call they stated the obvious; “[during the first quarter] the higher income customers are spending more”. This should come as a surprise to no one. The stock-market recovery over the past two years has seen a pronounced divergence emerge between the consumer confidence indices for higher and lower income households.

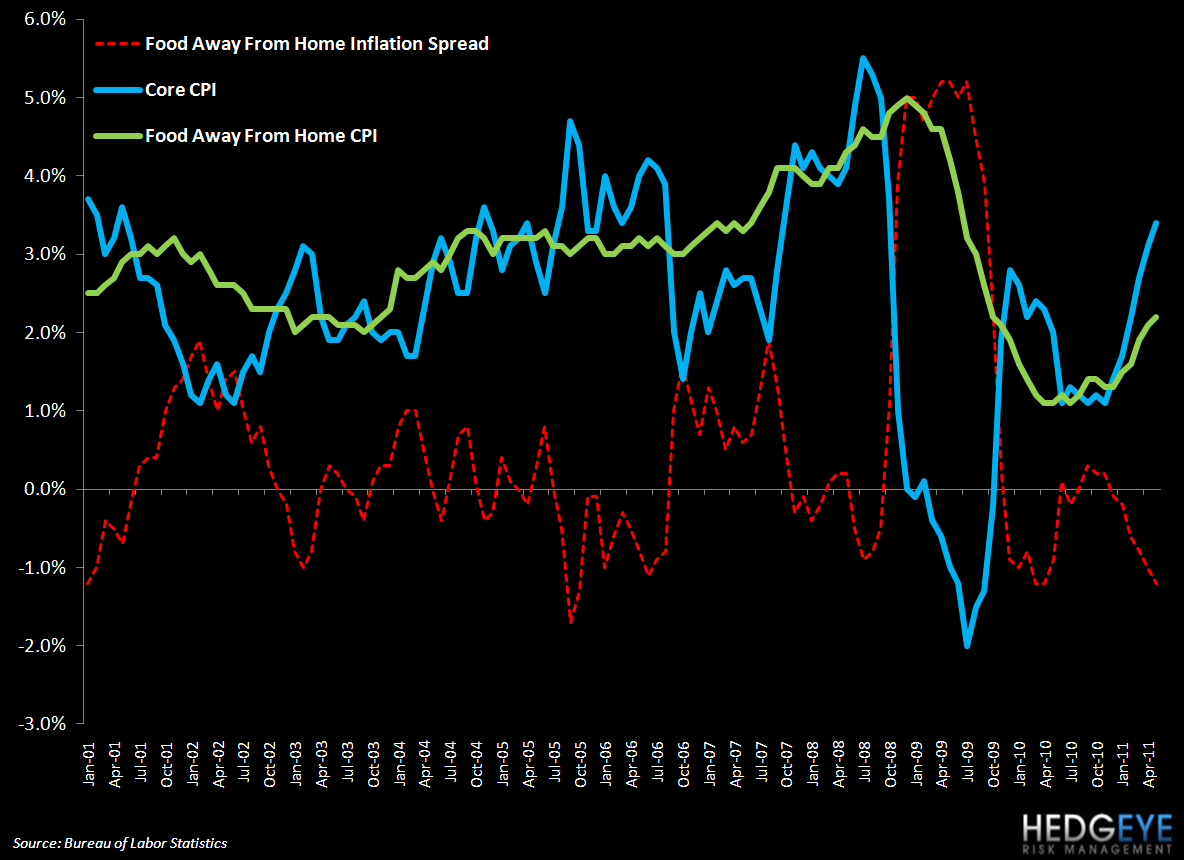

KR management went on to say, “just the last few weeks, we are starting to see some behavior changes even in the higher income customers, our data is showing that people are eating out less. Obviously when people eat out less, that's a benefit for us because, you know, they are going to get their meals from us, versus going out to a restaurant.” CPI data shows that, as inflation has ramped up from the trough in 2009, inflation in “Food at Home” has outstripped inflation in “Food Away From Home”.

The Kroger management team – like any other management team speaking on an earnings call – is always going to frame their situation in the best light possible and stated that KR’s price checks “show that most competitors are passing higher costs on to customers”. However, as the charts below indicates, restaurants may have seen a benefit from – on a relative basis – raising prices less than their “Food at Home” competitors, if the BLS data is anything to go by.

What the data suggests is that supermarkets and other retailers whose prices are represented by the “Food at Home” Consumer Price Index are increasing prices at a faster rate than core CPI is climbing. The “Food Away from Home” Consumer Price Index, on the other hand, is increasing at a slower rate than core CPI. This could be aiding traffic trends in the restaurant industry, which, have generally been robust over recent quarters. Additionally, the price action in the space – on a relative basis – has been particularly strong of late.

With KR comps this quarter at 4.6%, clearly the business is healthy whereas overall, restaurant industry is seeing comparable store sales running at around 2%. Within the restaurant space, the chains focused on the higher end are running same-store sales that are above KR.

The CPI data published by the BLS would suggest that the restaurant industry has been more cautious about taking price, as it should be. At this point, the main question in this area of the consumer space is, “when might the supermarkets’ aggressive stance with regard to pricing backfire?” As yet, it seems that customers are still being cautious about spending and perhaps manage their own food consumption more closely by eating at home. However, to the degree that price increases begin to turn away traffic from the grocers, restaurants would be the primary beneficiaries. As things stand, the restaurant industry is poised to transition into a more competitive position.

Howard Penney

Managing Director