As sequential inflation has slowed or, at least, become less broad-based in agricultural commodities, many of the key items we monitor seem to be at potential inflection points. Grain prices declined week-over-week and, while corn will likely see year-over-year inflation for the entirety of 2011, it seems increasingly possible that wheat purchasers could benefit from easier compares in the fourth quarter. This would obviously benefit PNRA and, to a lesser extent, the pizza concepts. Chicken wing prices, empirically, trade relatively higher in the second half of the year as football season kicks off. Clearly, this year, the NFL shutout is the $64,000 question for wing prices and, more importantly, BWLD sales.

The dollar remains the key driver and, any incremental bid that is placed under the value of the US currency will “deflate the inflation”, as Hedgeye CEO Keith McCullough, points out in his Macro notes.

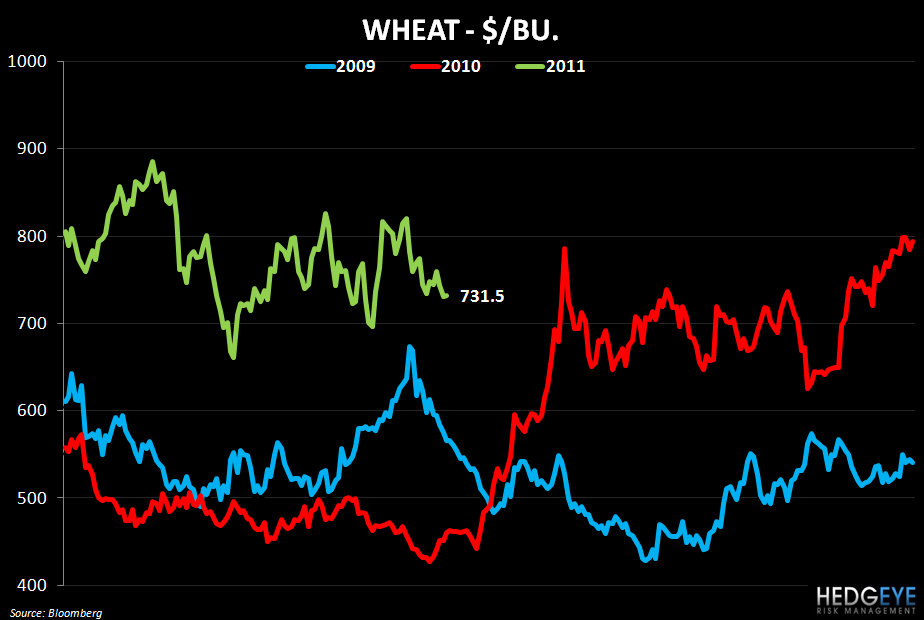

Wheat/Corn

Wheat may rise going forward, despite the 2.2% decline last week, due to speculation that wet weather in Canada may impair sowing. This data point, in addition to concerns that dry weather hurt the winter crop in the U.S. and France, the world’s two largest exporters, could provide support for wheat prices from here. In addition, the fact that corn inflation has outstripped inflation in wheat has caused a substitution effect as farmers turn to wheat, instead of corn, to feed their livestock. Wheat prices are a key concern for PNRA and the pizza concepts.

Corn prices are also likely to increase from here, at least judging by the supply and demand dynamics. While the dollar can absolutely trump these factors, in terms of what U.S. companies pay for input costs, corn demand is, according to Bloomberg, accelerating beyond farmers’ ability to boost yields. This is causing stocks to become depleted as Chinese demand grows and demand from ethanol factories also continues to be a bullish factor. Corn is really an important input cost for the broader restaurant industry because of its derivative impact on protein costs. CMG is one company that does not hedge its commodity costs in general. While Chipotle has corn locked for the year, any further impact on meat prices as a result of higher feed costs could impact margins.

Coffee

Coffee prices gained 1.8% week-over-week as weather continues to impact coffee production in Latin America. Demand remains strong for coffee and this has also helped keep prices high. Following its 1Q earnings call, PEET highlighted the significant impact high coffee prices can have on its gross margin in the second quarter. Coffee prices have come down since that earnings call took place but the absolute price remains extremely high.

Chicken Wings

Chicken wing prices gained last week. This cost change is not a concern for BWLD given that, on a year-over-year basis, prices remain highly favorable.

Howard Penney

Managing Director