TODAY’S S&P 500 SET-UP - June 15, 2011

What's interesting about yesterday’s low-volume rally to lower-highs is that neither the volume nor the volatility signals confirmed anything but the same. The Hedgeye S&P 500 Sector Risk Management Model continues to flash bullish on 0 of 9 Sectors. As we look at today’s set up for the S&P 500, the range is 49 points or -2.01% downside to 1261 and 1.80% upside to 1311.

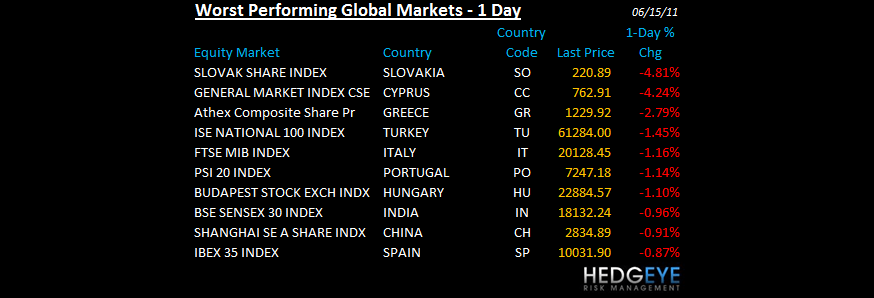

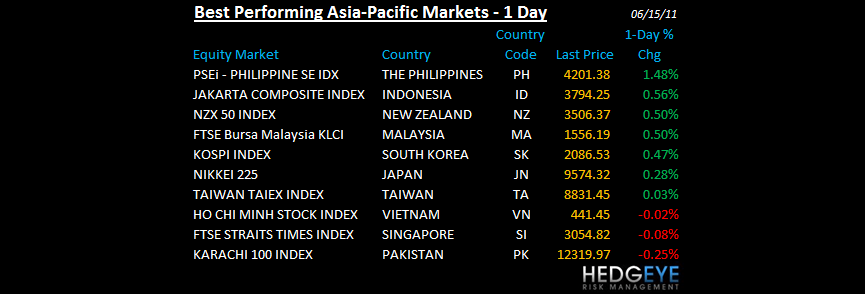

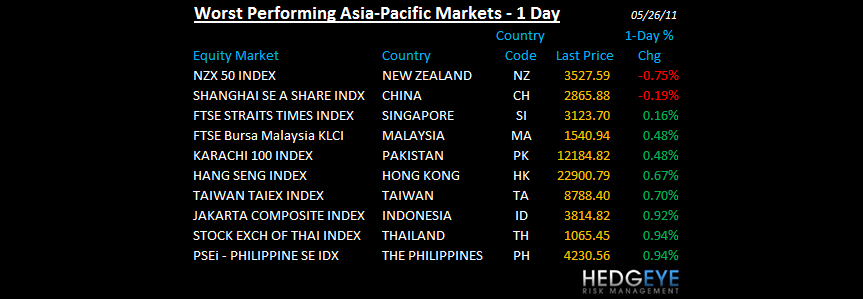

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1919 (+2463)

- VOLUME: NYSE 915.34 (+0.78%)

- VIX: 18.26 -6.88% YTD PERFORMANCE: +2.87%

- SPX PUT/CALL RATIO: 1.50 from 1.67 (-6.13%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 19.95

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 3.11 from 3.00

- YIELD CURVE: 2.66 from 2.60

MACRO DATA POINTS:

- 7 a.m.: MBA Mortgage Applications, prior 0.4%

- 8:30 a.m.: CPI, est. 0.1%, prior 0.4%

- 8:30 a.m.: Empire Manufacturing, est. 12.00, prior 11.88

- 9 a.m.: Total Net TIC Flows, prior $116.0b

- 9:15 a.m.: Industrial production, est. 0.2%, prior 0.0%

- 9:15 a.m.: Capacity utilization, est. 77.0%, prior 76.9%

- 10 a.m.: NAHB Housing Market: est. 16, prior 16

- 10:30 a.m.: DoE inventories

WHAT TO WATCH:

- Euro-area finance chiefs emergency session fails to break deadlock on how to enroll investors in second Greek bailout

- Bullish sentiment decreases to 37.0% from 40.9% in the latest US Investor's Intelligence poll; Bearish sentiment increases to 26.0% from 22.6% - those expecting a market correction increases to 37.0% from 36.5%

- Federal Reserve deciding whether to set explicit inflation targets - Bloomberg

- Consumers ditching cable for satellite, phone companies - LA Times

- Conneticut AG asks Citi for data on its security after hacking attack - FT

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Oil Declines as Concerns Over European Debt Counter U.S. Inventory Drop

- Copper Falls in London Before Industrial Production Reports: LME Preview

- Gold to Extend Gains as Buyers Seek ‘Safety’ Against Inflation, Fund Says

- Wheat Harvest Forecast Increased by Australia as Rains Boost Crop Outlook

- Natural Gas Production at Record as Shale Puzzle Solved: Energy Markets

- Copper Users in China Plunder Stockpiles as Goldman Forecasts Record Rally

- Canadian National Beating Canadian Pacific With Investors: Freight Markets

- Gold May Slide as Strengthening Dollar Saps Alternative Investment Demand

- Cotton Shortage in China May Worsen on Lack of Land, Increasing Imports

- Cocoa Arrivals From Brazil’s Bahia Decline by 5.3%, Analyst Hartmann Says

- Rio’s Hu May Get Chance to Exit China With Australia Plan for Jail Treaty

- Rubber in Tokyo Climbs for First Day in Six as Oil Price, Yen Boost Appeal

- European Commodity Day Ahead: Copper May Rally as China Stockpiles Plummet

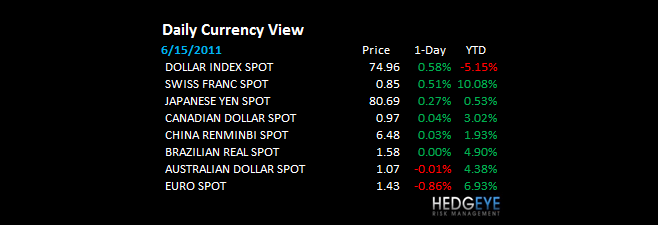

CURRENCIES

EUROPEAN MARKETS

- EUROPE: no follow through across European stocks; Greece crashing again, down another -1.5%; Spain down -0.7%; Italy -1% - tick tock

- Euro-area finance chiefs emergency session fails to break deadlock on how to enroll investors in second Greek bailout

ASIAN MARKETS

- ASIA: no follow through to Chinese short covering-China down -0.9% and were long it yet; HK down another -.7%; India down -.9% to -11.5% YTD

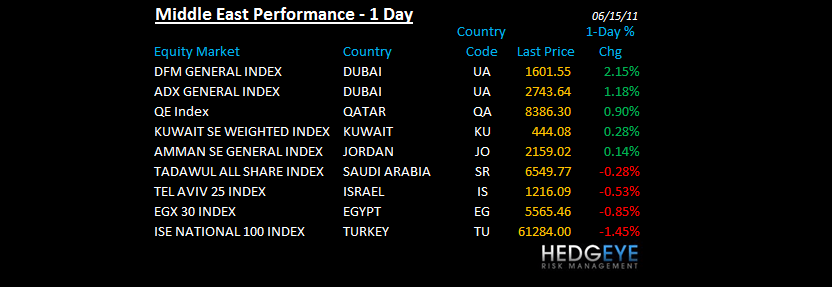

MIDDLE EAST

Howard Penney

Managing Director