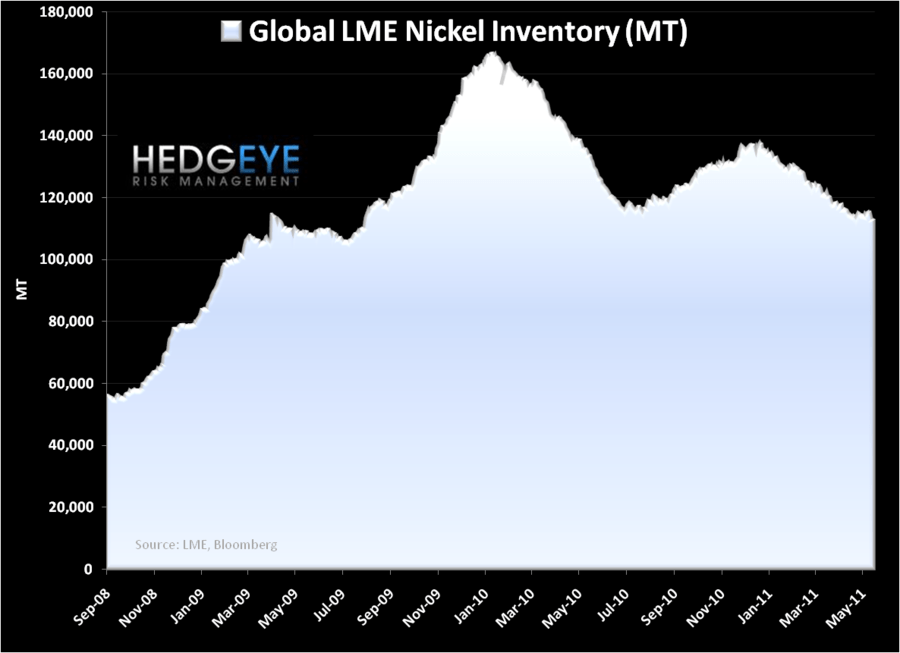

Conclusion: Inventories of nickel are set to increase due to more tepid demand and increasing production, which will lead to lower prices. Deflation of the Inflation is bad for commodity producers, but positive for consumers.

In the 1940s, the nickel industry was a monopoly in the literal sense of the word as Canada’s Inco controlled more than 90% of the global nickel market. Today, the production of nickel is much more diversified with the largest producer, Russia’s Norlisk Nickel, holding roughly 20% of the global market share. Just behind Norlisk in terms of market share is Vale SA, a Brazilian company, which acquired Inco in 2006. While still a concentrated industry in terms of production, the price of nickel is very much driven by supply and demand, especially as its correlation with the U.S. dollar weakens. (Incidentally, the United States has no active nickel mines.)

Nickel is a metallic element and is the fifth most abundant element in the earth, after iron, oxygen, silicon and magnesium. Close to two-thirds of new nickel is used to make stainless steel. Alloys containing nickel are known for their strength, toughness, and corrosion resistance. These attributes make nickel critical to many industries. Construction and transportation account for 37% of nickel demand and 18% is used in machinery and electrical applications.

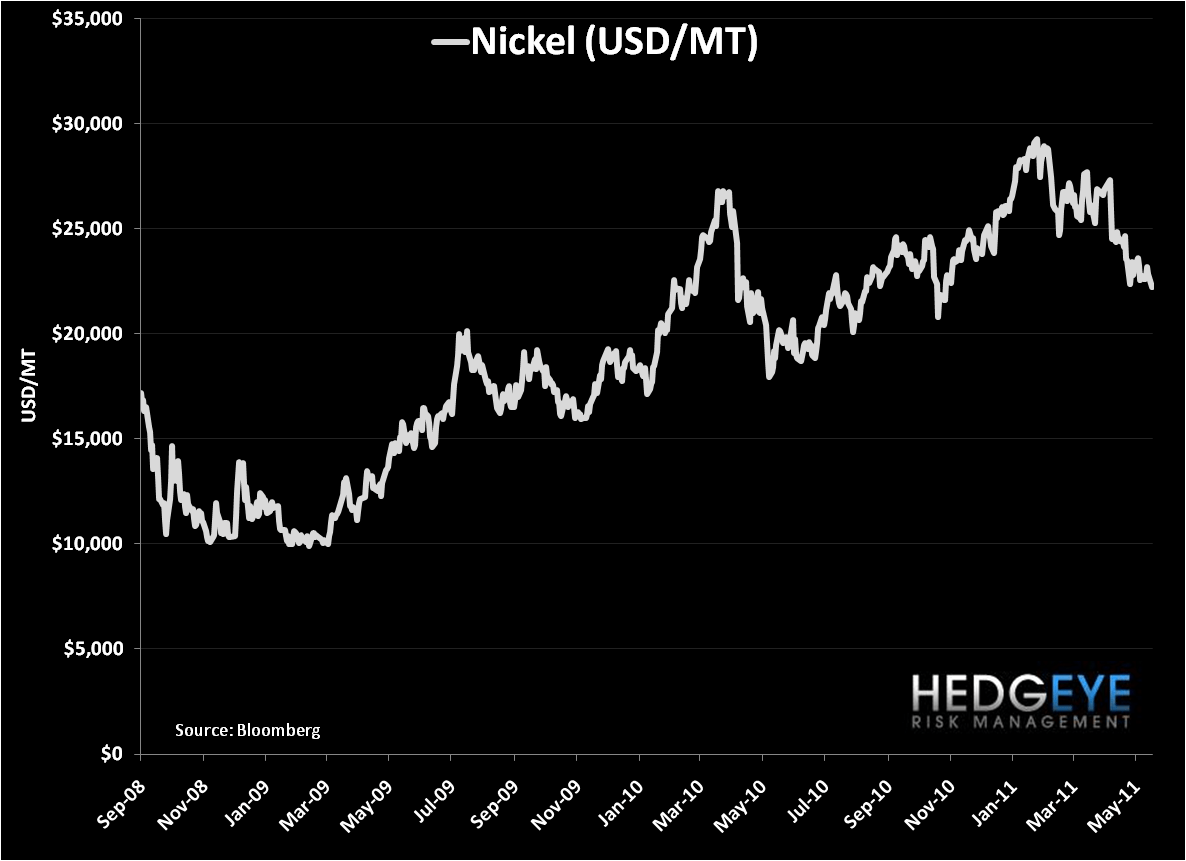

Similar to many commodities, China is a primary driver of global nickel demand given the vast urbanization trends. Specifically, China consumes about a one-third of the world’s nickel and is the world’s largest producer and user of stainless steel due to its rapid growth and urbanization. Not surprisingly then, much of the recent decline in the price of nickel, and really many commodities, can be attributed to slowing growth in China. In the chart below, we show the price decline over the past month, though it is still above its estimated marginal cost of $17,500 to $20,000 per metric tonne.

In the short term, decline in demand for nickel from China is being attributed to stainless steel mills being shutdown, Chinese power shortages (see a note by Darius Dale on this point from June 1st, 2011, “Asia’s Power Struggles Part 1”), and monetary tightening by Chinese authorities. In fact, Chinese steel giant Baosteel indicated that they expect Chinese steel consumption to grow 5-7% over the next five years, which is a deceleration, but consistent with the most recent 5-year plan from China. This is also consistent with recent comments from Norlisk, whose Chief Analyst indicated:

“Primary nickel usage will expand more than 5 percent this year, compared with 15 percent in 2010.”

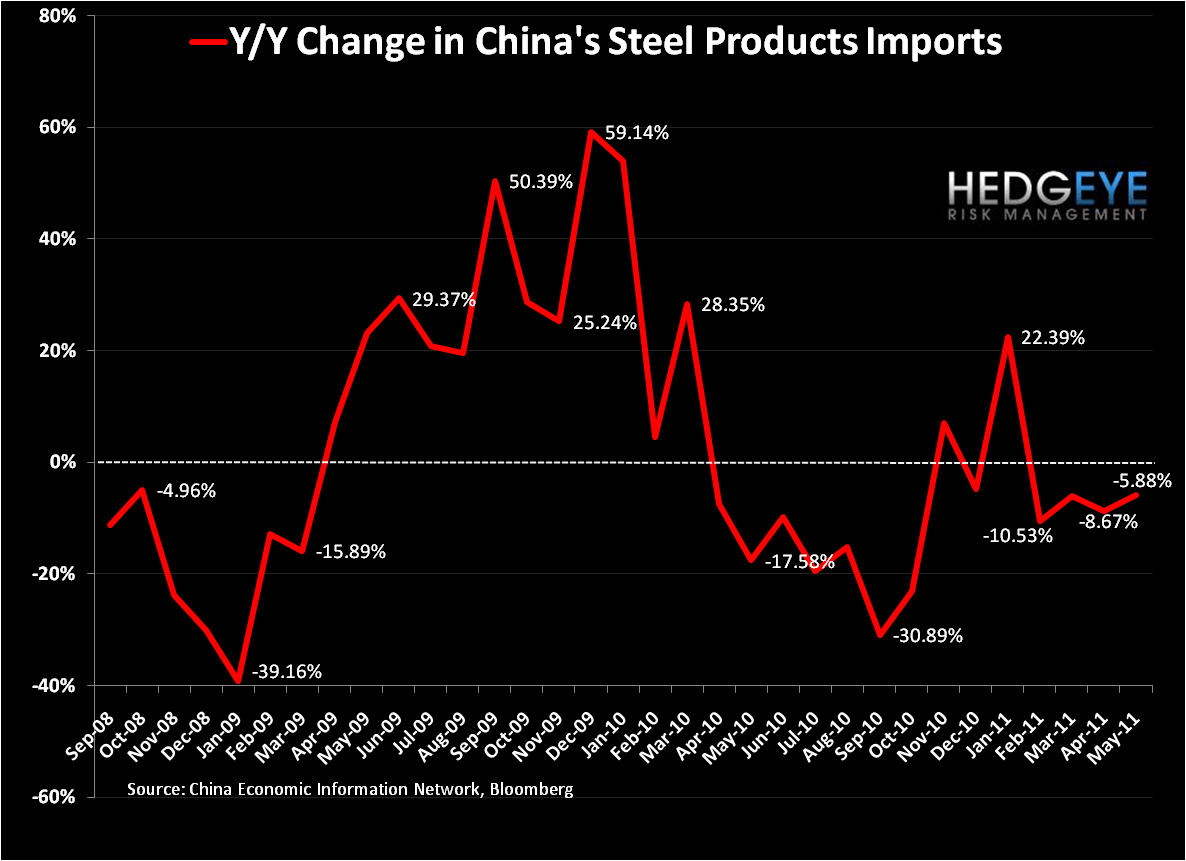

More broadly, we’ve charted below Chinese steel imports and nickel and alloy imports, both of which highlight a decline in demand from China in 2011 versus 2010.

Interestingly, nickel inventory, as measured by the London Metals Exchange, has actually been trending down since the start of the year, which is obviously a bullish factor for price. That said, over the past three years, the trend of nickel inventory has been up and to the right, as we show in the chart below. Looking past the short term drawdown in nickel inventory, there are two factors that should drive a growth of inventory: 1) growing use of nickel pig iron by China and 2) accelerating global nickel production.

On the first point, Chinese production of nickel pig iron, which is a low cost substitute for refined nickel, is set to increase up to 50% this year from 160,000 tons in 2010 to 240,000 in 2011. Production of nickel pig iron will continue to accelerate into 2012. To the second point, there are a number of projects that are coming over the next five years that will add significant production. In fact, according to Wood MacKenzie, the largest five projects alone will produce 220,000 tons of nickel, with the bulk coming online in 2012 and 2013.

As commodities prices continue to trade more in line with their fundamental supply and demand drivers, nickel is a commodity that is increasingly looking like it has price downside over the intermediate term.

Daryl G. Jones

Managing Director