Conclusion: Keith just shorted JCP in the Hedgeye virtual portfolio. And I quote... "Very few things are easy in the life of a short seller - but re-shorting iJCP here is." People are looking for a 'transformational change', but they'll need to wait til Spring 2012 for a clear articulation -- and it will need plenty of capital. Margins going down before they go up again.

I’m not saying that the guy is not a retailing genius, but when you have the best content in the world, no competition, a customer that has no price boundaries, and an unlimited SG&A budget, it does make it a bit easier to be a ‘visionary’.

JC Penney, on the other hand, has some of the worst content (over-indexed to mid-tier private label), endless competition, a cash-poor customer, and the most limited SG&A budget in retail. I don’t care if you took the equivalent of what Sam Walton was to retail when he founded Wal-Mart in 1962…if you don’t deploy capital, you can’t grow.

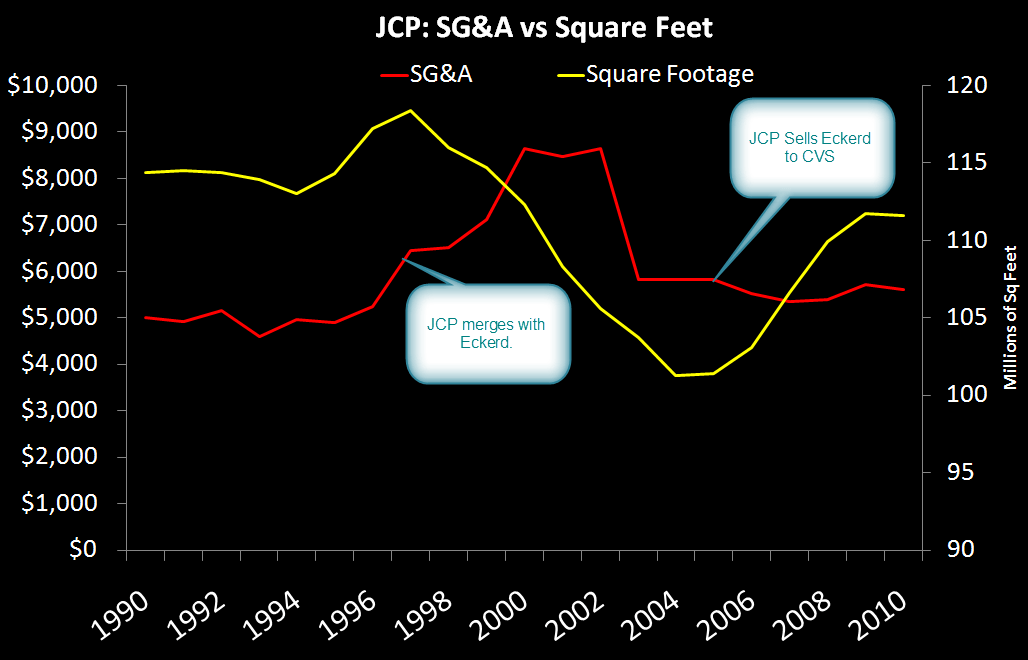

Look at JCP over time. Can anyone explain to me how JCP grew square footage by 12% over the past 8 years (after they sold Eckerd to CVS), but held SG&A flat at $5.7bn? This thing has been cut bone dry. Opportunities to cut more costs to improve margins are extremely slim. It needs to invest in SG&A, Capex and the right working capital (which is tough to do without the R&D/marketing [i.e. SG&A] to back it) in order to turn JCP around. All of the ‘retailing 101’ best practices have been put in place.

I cannot imagine that anyone coming in from a place as high-profile as Apple with such a wide-open checkbook would come into JCP and not demand the same.

Heck, maybe Mr. Johnson a retailing god, and he does things in a way that none of us can imagine (a la Apple). But it won’t be without taking JCP’s margins down – by a long shot – to make it happen.