TODAY’S S&P 500 SET-UP - June 14, 2011

The three things that matter this morning:

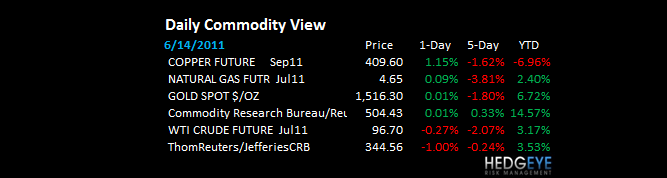

- Deflating The Inflation (our Q2 Macro Theme) was big yesterday = CRB Index down -1.1% on oil down hard

- Chinese Data for May was rock solid sequentially = Fixed Asset Investment up 40bps sequentially in May to +25.8%

- Global Equity Markets stopped going down

Bulls are dying for some bullish data to cling to at this point and, if you look hard enough, it's there today - what price do you pay remains the question. In SP500 points, I say just relax and manage risk around the range (1)

Being perma anything won't work in 2011. As we look at today’s set up for the S&P 500, the range is 31 points or -0.94% downside to 1259 and 1.90% upside to 1290.

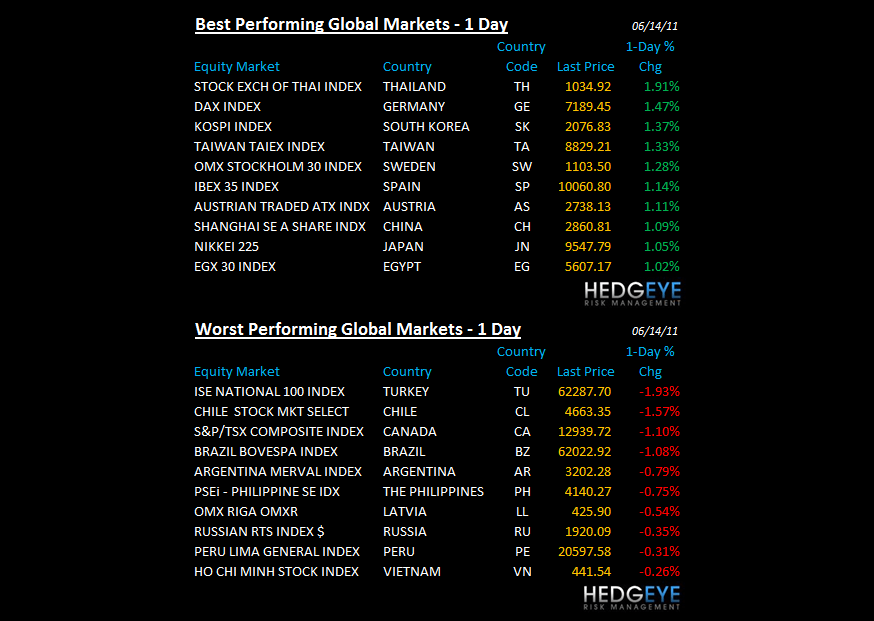

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -468 (+1452)

- VOLUME: NYSE 908.34 (-10.89%)

- VIX: 19.61 +3.98% YTD PERFORMANCE: +10.48%

- SPX PUT/CALL RATIO: 1.67 from 1.77 (-6.13%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 19.95

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 3.00 from 2.99

- YIELD CURVE: 2.60 from 2.58

MACRO DATA POINTS:

- 7:30 a.m.: NFIB Small Business Optimism, est. 90.5

- 7:45 a.m./8:55 a.m. ICSC/Redbook Weekly Sales

- 8:30 a.m.: Producer Price Index, est. 0.1%

- 8:30 a.m.: Retail sales, est. (-0.5%)

- 10 a.m.: Business inventories, est. 0.9%

- 11:30 a.m.: U.S. to sell $28b 4-wk bills

- 2:30 p.m.: Fed Chairman Bernanke speaks at the Committee for a Responsible Federal Budget Annual Conference

WHAT TO WATCH:

- Nokia and Apple agreed to settle all patent litigation between the companies in a deal that awards a one-off payment and royalties to Nokia

- BofA “significantly hindered” a federal review of its foreclosures on loans insured by the FHA, U.S. says

- U.K. inflation held at the fastest pace since October 2008

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Sugar Rising as Thailand Port Congestion Worst in Memory: Freight Markets

- Michael Coleman’s Trading Company Hires Ex-JPMorgan Coal Trader Chan Bhima

- Cotton Acres in China Seen Capped as Manufacturing Jobs Lure Farm Workers

- Record Corn Crop in India May Help Increase Exports, Limiting Global Costs

- Fees Punish Savers Seeking Hedge-Fund Cachet in Commodities Futures Funds

- Crude Oil Trades Near One-Month Low on Demand Outlook for China and U.S.

- Corn Drops for Third Day as Weather Improves, Pre-Export Inspections Fall

- Copper Climbs for First Day in Three as China Production Maintains Growth

- Sugar Falls on Reduced Concern About Brazilian Supply; Coffee Prices Drop

- Gold May Advance on Inflation Concern, Sovereign-Debt Crisis in Europe

- Violent Protests Increase at Chile’s El Teniente Copper Mine, Codelco Says

- Chicken Breeders Face Tax-Cut Hawks in U.S. Senate Showdown Over Ethanol

- Sino-Forest’s Investors Will Question Executives After Stock Plunges 73%

CURRENCIES

EUROPEAN MARKETS

- EUROPE: another dead cat bounce on hope of Keynesian resolve? DAX up +1.6% (we're long); Spain +1.4% (were short); Greek stocks, no dice

ASIAN MARKETS

- ASIA: better than bad; China rallies on "news" that inflation hits a new high; Hang Sang fails to confirm (down -0.05%); India +0.27%

- China May CPI +5.5% y/y, matching expectations. May PPI +6.8% y/y vs cons +6.5%.

- Japan April capacity utilization (1.1%) m/m. Revised April industrial output +1.6% m/m vs prelim +1.0%.

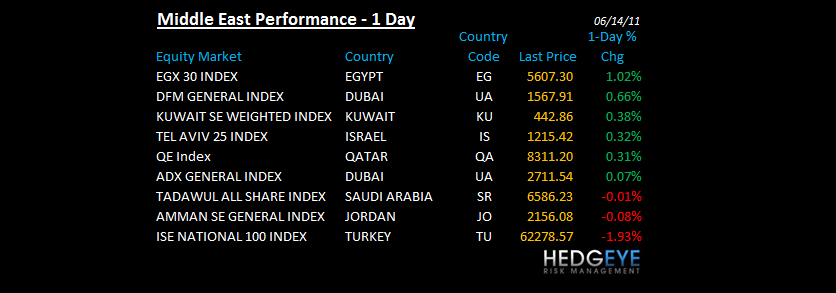

MIDDLE EAST

Howard Penney

Managing Director