Positions in Europe: Long Germany (EWG); Short Spain (EWP)

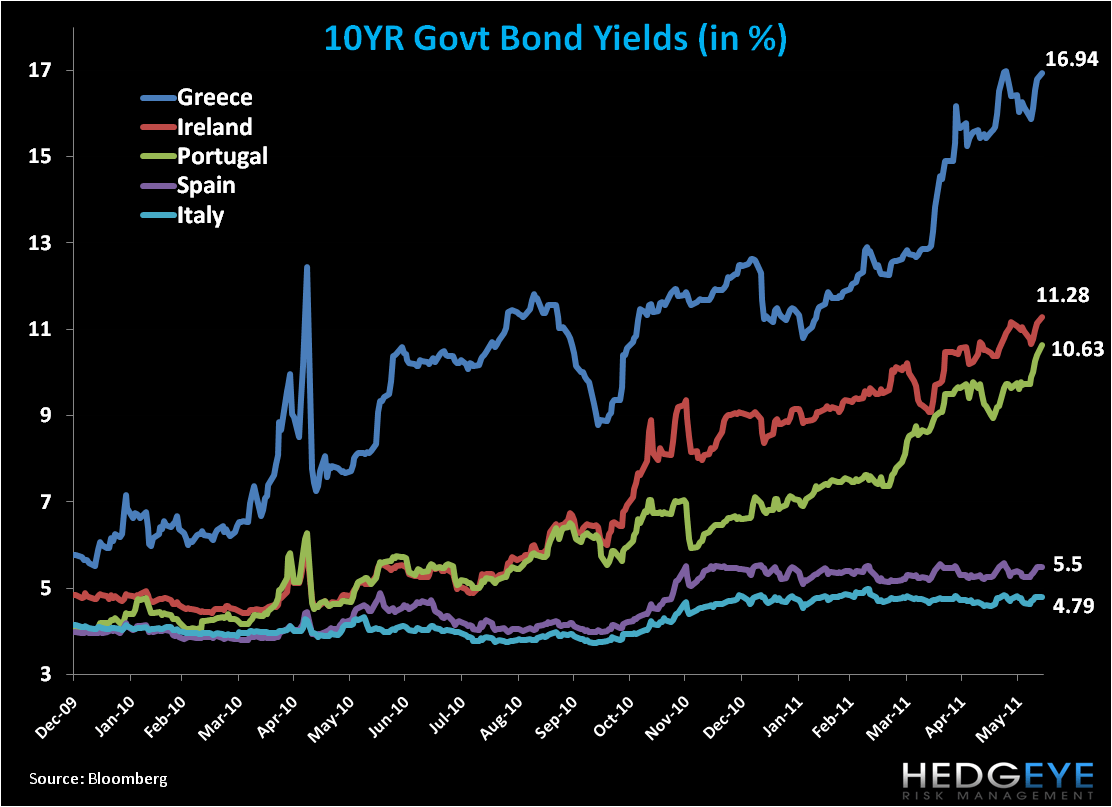

Below we show our weekly European Risk Monitor charts that indicate more of the same trend: risk premiums across the European peripheral continue to blow out over the intermediate term, a trend we expect to continue even as troika (European Commission, ECB, and IMF) continues to subsidize the PIIGS to prevent in their minds the “ugly” words of default and restructuring. Troika’s actions should however also continue to support the EUR-USD around $1.40, with upper resistance around $1.45.

The newest piece of “support” in the developing dynamic of the periphery’s sovereign debt imbalances and the growing counterparty exposures between domestic banks, the Eurozone National Central Banks, and ECB, is Germany’s increasing approval of a second bailout package for Greece. The latest band-aid proposed is ~ 90 B EUR, complicit with the Greeks selling off state assets worth ~ 30-50 B EUR and more strict enforcement of austerity measures. German Finance Minister Wolfgang Schaueble has called for investors to exchange all the Greek bonds currently in their portfolios for new ones with maturities extended by seven years. This presumes lower interest rates, with the original principal paid in full at the new maturity. The extent of this haircut, however, is not known, and obviously a very substantial risk. The ECB’s stance continues to be one against investors (namely private) taking on any losses, but in favor of any bailout to direction attention away from default and restructuring talk.

Our European Financials CDS Monitor shows that Bank swaps in Europe were wider last week on a week-over-week basis. 35 of the 38 swaps were wider and only 3 tightened, with Italian and Portuguese banks looking the worst.

We continue to take very conservative view of Europe, tending to favor the region’s fiscally sober countries with healthy growth profiles, like Germany and Sweden. That said, Germany, which we’re currently long via the etf EWG in the Hedgeye Virtual Portfolio, has not performed well, with the DAX at +2.8% YTD but down -4% over the last month. Alongside the swing our position has move to one of caution as the high frequency data has slowed over the last 2-4 months.

At the right price we’d re-short Spain (EWP) again. Macro data from the periphery continues to suggest marked headwinds as inflation accelerates, austerity chokes off growth from already anemic levels, unemployment accelerates, and consumer and business confidence shake.

Matthew Hedrick

Analyst