This note was originally published at 8am on June 08, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Whatever we are, it’s we who move the world, and it’s we who’ll pull it through.”

-Hank Rearden (Atlas Shrugged)

If that isn’t the quote of a self-made man, I don’t know what is. In Atlas Shrugged, Rearden Metal personified capitalism. Sometimes it’s harsh. Sometimes you win. Sometimes you lose. But you are always going to be held accountable to your own decision making.

Le Bernank showed that he stands for none of that last night in Atlanta. Since he’s never run a company, hired/fired employees, or assumed the responsibility of putting his own capital at risk – this should not surprise you. He is a Keynesian Central Planner.

Whether you are an Ayn Rand, Ben Bernanke, or Jaime Dimon fan is of no particular concern to me when I wake up to write this note to you every morning. I am concerned with making money so that I can confidently and gainfully employ a team of professionals that helps you manage risk.

If there are more than a few lines in Ayn Rand’s 1168 pages of Atlas Shrugged that resonate with me, that doesn’t mean I am an Ayn Rand lover inasmuch as I don’t have to love anything in this good life more than my wife and family. I like to read things that I disagree with. I like things that make me think.

I am a Risk Manager – and, unlike Le Bernank, that means I am tasked with considering multiple ideas across multiple risk management scenarios. Accepting anyone’s dogma in full, including the Holy Bible’s, lacks the intellectual honesty to question. I am tasked with not losing you money. That includes accepting when I am wrong. The goal is to be right.

What’s been right about cutting interest rates to ZERO percent and scaring the living daylights out of Americans in order to market the fear-mongering message? Has socializing losses made the capitalists in this country less or more confident in hiring? What’s the difference between jacking up short-term liquidity and eroding long-term demand?

These are critical questions that the Chairman of America’s Unaccountable Central Planning Board does not have an answer to. Last night he called GROWTH “frustratingly slow” and INFLATION “transitory.” In response, JP Morgan’s respected CEO, Jaime Dimon, asked Le Bernank, “do you have fear like I do?”

The context of Dimon’s question was also critical. He prefaced the question about fear by asking Bernanke if he thinks in “10 years someone will be writing a book about” how all of this Big Government Intervention was what perpetuated the slowdown itself. Atlas Shrugged is a 54 year-old fictional book. Jaime, get the paperback.

Back to the Global Macro Grind…

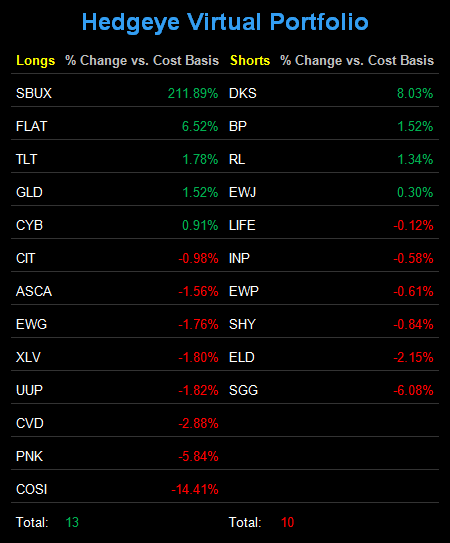

Yesterday, when the US stock market was up intraday, I cut my US Equity exposure in the Hedgeye Asset Allocation Model in half, selling down our long (and wrong) position in US Healthcare (XLV) from 6% to 3%.

If the US stock market closes down again today, it will be down for 6 consecutive days and 6 consecutive weeks. If that’s Le Bernank’s definition of success, using a massive amount of financial and societal leverage, I’d hate to see what losing looks like.

Why do I continue to sell strength in equity and commodity market exposures?

- The Market – real-time prices don’t lie; Keynesians do.

- The Data – I have yet to see sequential improvement in any of the high frequency data that we track

- The Fed – and Indefinitely Dovish Fed that can’t hike (or cut) has been a life preserver for Gold and UST Bonds

Away from the US, here’s The Market’s message:

- China (the world’s 2nd largest economy) remains bearish TRADE and TREND with the Shanghai Composite down -2.1% YTD

- Japan (the world’s 3rd largest economy) remains bearish TRADE and TREND with the Nikkei down -7.6% YTD

- Germany (the world’s 4th largest economy) just moved to bearish TRADE and TREND this morning with the DAX down a full -1%

In terms of The Data:

- South Korean GDP Growth slowed sequentially to +4.2% in Q1 (better than US, Japanese, or W. European Growth, but slowing)

- Brazilian Inflation (CPI) rose sequentially to +6.6% year-over-year in May vs +6.5% in April

- Philippines Inflation (CPI) rose sequentially to +4.5% year-over-year in May – a new YTD high

But The Fed (and I couldn’t make this up if I tried):

- Expects US employment to improve in the coming months

- Expects US Growth to re-accelerate

- Expects US Inflation to remain “transitory”

PROBLEM: The Market and The Data completely disagree with The Fed (as they have for the last 3-6 months).

That’s why Ben Bernanke having a smirk on his face when a Market/Data centric Risk Manager like Jaime Dimon was asking him THE question (what if your Keynesian Dogma is wrong?), made every red-white-and-blue capitalist in this country want to puke.

This is the beggar/bailout central planning that we ordered up folks. “Whatever we are”, it’s only we who can stop doing what we are doing to this country – so that we can start to pull it through.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $98.40-100.79, $1535-1555, and 1275-1313, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer