“If we are to build a better world, we must have the courage to make a new start.”

-F.A. Hayek

Last week I received a tremendous amount of positive feedback on my note titled “American Optimism.” So I’d like to start this week off by thanking you for inspiring me. I am very bullish on the prospects of building a better world – I am very bullish on change.

Interestingly, but not surprisingly, Hayek wrote the aforementioned quote in the concluding chapter of “The Road To Serfdom” (page 237) in 1944. His summary thought stood in the face of British-style Keynesianism that had dominated the economic theory of his time.

What was Keynes’ response to Hayek’s conclusions?

Bruce Caldwell (who edited the most recent edition of “The Road To Serfdom”) captures the moment best in his Introduction:

“John Maynard Keynes read the book on the way to the Bretton Woods conference, and delighted Hayek when he wrote him that it was “a grand book” and that “morally and philosophically I find myself in agreement with the whole of it; and not only in agreement with it, but in a deeply moved agreement.” (Letter, John Maynard Keyens to Hayek, June 28, 1944)

Alrighty then – we have a consensus!

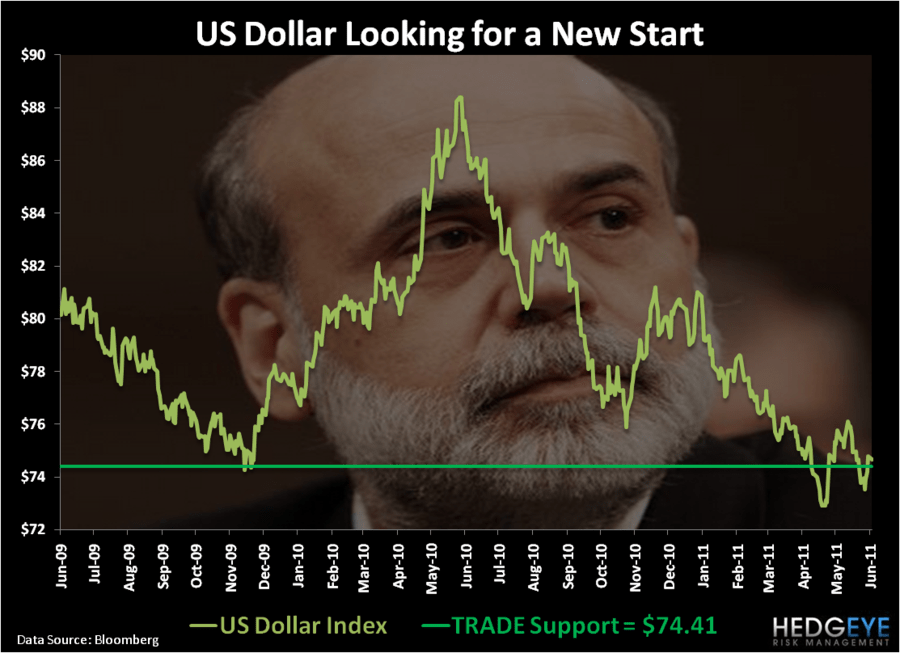

Last week, the most bullish week-over-week moves in all of Global Macro came right where I think the prospects for change are going to be measured – in the real-time price of the US Dollar Index.

I’m not so concerned about US stocks being down for 6 consecutive weeks when it’s crystal clear that Growth Slows As Inflation Accelerates. What I need to see change (to get bullish on stocks) is a Deflating of The Inflation (Hedgeye Q2 Macro Theme).

With the US Dollar Index UP a full +2% last week to $75.60, here’s what happened to things priced in US Dollars:

- US Stocks = DOWN -2.3%

- WTI Crude Oil = DOWN -0.9%

- Copper = DOWN -1.4%

Le Mucker’s SERIES 66 TEST QUESTION: Which of those 3 things matters most to the US Economy?

- La Bernank says stocks

- Le Consumer says gas prices

- Le Industrialist says cost pressures

I’ll go with #2 and #3.

If you want a New Start in this country you have to see a Deflating of The Inflation. Otherwise you’ll continue to see a slowdown in 70% of US GDP (Consumption) and margin compression at the companies who are supposed to employ these consumers.

The Stagflation is not hard to understand (Growth Slowing below the rate of Inflation). It just isn’t palatable for the Keynesian Kingdom to accept responsibility for it. That would be called holding themselves accountable.

Until I start seeing data that implies that both of these things are occurring at the same time:

- Growth is slowing at a decelerating rate

- Inflation is accelerating at a decelerating rate

Why would I stop protecting my family’s hard-earned wealth?

Being in Cash in 2011 has obviously beaten 48 of the country stock markets in the Hedgeye Global Macro Stock Market Index for the YTD (there are 66 country indices in our Index). And, depending on where you bought them (or what index you are in – both the Nasdaq and Russell 2000 are DOWN for 2011 YTD), the +1% YTD return in the SP500 has been slim pickings!

Here’s how the Hedgeye Asset Allocation Model was positioned going into and out of Friday’s US equity market swoon:

- Cash = 52% (UP +3% week-over-week after selling ½ our US Equity Allocation on mid-week strength)

- International Currencies = 21% (Chinese Yuan and US Dollar – CYB and UUP)

- Fixed Income = 18% (Long-term UST Bonds and US Treasury Flattener – TLT and FLAT)

- Commodities = 3% (Gold – GLD)

- US Equities = 3% (US Healthcare – XLV)

- International Equities = 3% (Germany – EWG)

And no, being in 52% Cash wasn’t enough!

On a week-over-week basis, I lost money in 4 of 6 of these asset allocation positions:

- US Dollar (UUP) = +1.5%

- Long-term Treasuries (TLT) = +0.8%

- Chinese Yuan (CYB) = -0.4%

- Gold (GLD) = -0.7%

- Healthcare (XLV) = -1.1%

- Germany (EWG) = -2.7%

It’s a good thing I have shorts – and there’s plenty to be optimistic about on that front. There’s always risk to be managed somewhere.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, $98.60-100.45, and 1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer