TODAY’S S&P 500 SET-UP - June 13, 2011

Roll out the bearish on growth consensus – it’s career risk management time for the bulls and time to get the perma-bears back in the media (Roubini top story on Bloomberg this morn calling it the “Perfect Storm” – and Barrons Mid-Year Roundtable is actually funny when you read what their consensus was (side by side) 6 months ago).

Consensus, however, can remain a constant until its fully priced in:

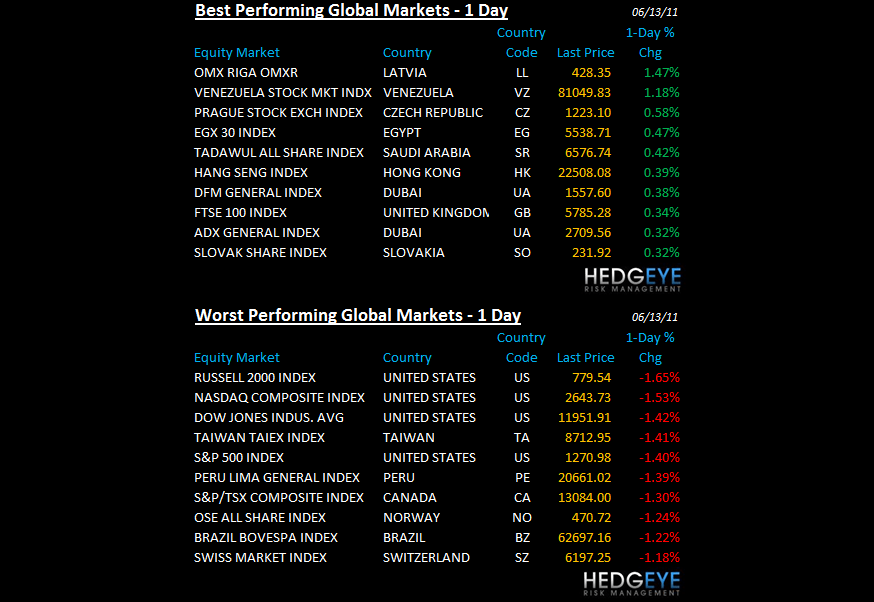

- ASIAN EQUITIES: no bid this morning, with Japan down another -0.7% to -7.6% YTD on a nasty machinery order print (-3.3%)

- EUROPEAN EQUITIES: no bid as Greek stocks and bonds continue to crash (Athex Index down -27% since mid-Feb)

- COMMODITIES: no bid for Copper in particular (down -0.8% this morn) as base metals (nickel smoked) and silver (I guess that “industrial demand” component are seeing Growth Slowing getting priced in.

As we look at today’s set up for the S&P 500, the range is 43 points or -1.26% downside to 1255 and 2.13% upside to 1298.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1920 (-2755)

- VOLUME: NYSE 1019.30 (+12.07%)

- VIX: 18.86 +6.13% YTD PERFORMANCE: +6.25%

- SPX PUT/CALL RATIO: 1.77 from 1.43 (+24.46%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.29

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 2,99 from 3.01

- YIELD CURVE: 2.58 from 2.58

MACRO DATA POINTS:

- 9 a.m.: ECB’s Trichet speaks at London School of Economics

- 9:30 a.m.: Fed’s Lacker speaks on manufacturing in Virginia

- 11 a.m.: Export inspections, corn, wheat, soybeans

- 11:30 a.m.: U.S. to sell $27b 3-mos. bills, $24b 6-mo. bills

- 4 p.m.: Crop conditions

- 7 p.m.: Fed’s Fisher speaks in Dallas

WHAT TO WATCH:

- Citi defends hacking disclosure delay - WSJ

- US banks to cut Treasury use - FT

- Best Buy may postpone its European expansion plans - FT

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Nickel Plunging Into Bear Market as Expanding Glut Outstrips Record Demand

- Aluminum Bookings From LME’s Asian Warehouses Jump as U.S. Fees Hit Record

- Oil Declines for a Second Day on Concern Over Economic Growth, Share Slump

- Palm Oil Has Longest Losing Run in Two Years on Malaysian Supply Outlook

- China’s Copper Imports ‘Low’ Last Month as Stockpiles Drop, Goldman Says

- Wheat Rises as Rains May be Too Late to Prevent U.S., France Yield Losses

- Rubber Drops to Two-Week Low as Chinese Demand May Ease on Slowing Economy

- Funds Boost Bullish Agriculture Bets for Third Week as Crops May Decline

- George Soros Urges G20 to Demand Mining Transparency, Le Figaro Reports

- Tanzania Plans to Discuss Proposed Super Tax With Miners, Minister Says

- Roubini Says a ‘Perfect Storm’ May Converge on the Global Economy in 2013

CURRENCIES

EUROPEAN MARKETS

- EUROPE: no bid; Greece continues to crash (down -27% since FEB hope highs); FTSE/DAX/CAC all breaking Hedgeye intermediate term TREND lines

ASIAN MARKETS

- A China banks issue CNY551.6B of new loans in May vs cons CNY650B - MarketWatch; M2 at end of May +15.1% y/y vs cons +15.5%.

- ASIA: no bid; China makes new YTD lows and Japan down another -0.7% (were short) as rest of Asia breaks down (Taiwan -1.4%, Indonesia -1.0%)

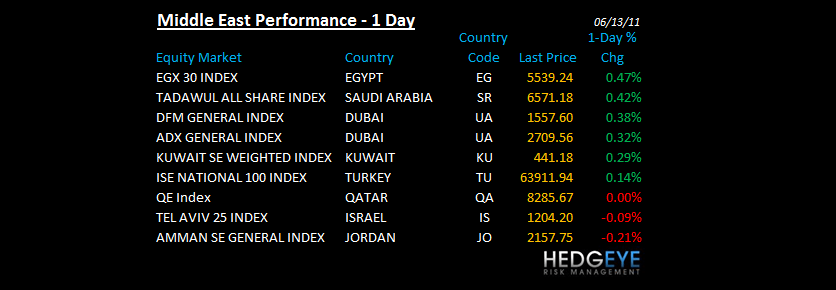

MIDDLE EAST

Howard Penney

Managing Director