TODAY’S S&P 500 SET-UP - June 10, 2011

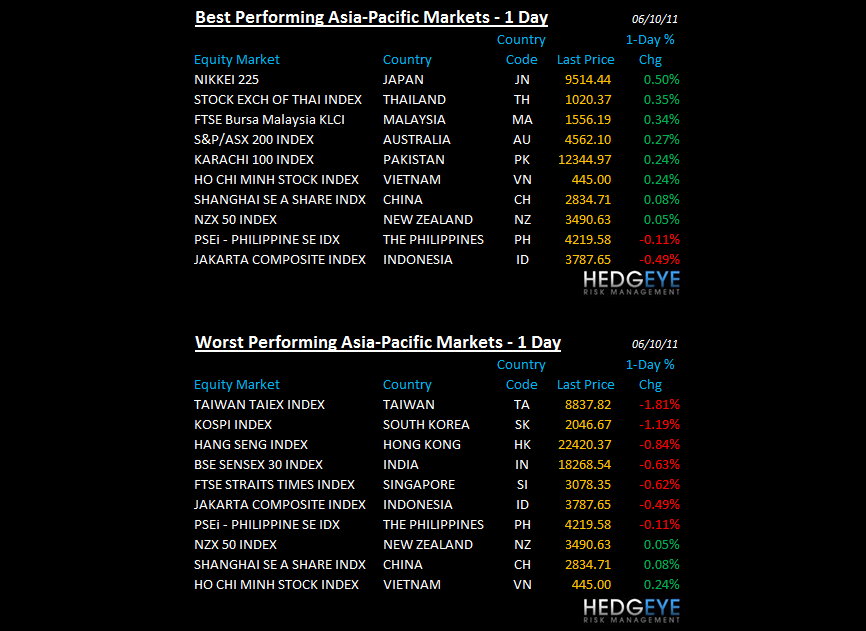

This morning’s early look on the data will look “quiet” to US centric investors, but the rest of the world doesn’t cease to exist. Asian Equities (and currencies) look flat out ugly right now as the data continues to support Growth Slowing.

- India’s Industrial Production dropped again in April to +6.3% y/y vs +8.8% last month (we’re short INP)

- Chinese imports were fine (internal demand) but Exports were another miss (external demand) at +19%

- KOSPI finally broke its intermediate term TREND line of support (2077), down -1.2% overnight

Oil and Russia both rallied yesterday to lower-highs but remain broken on intermediate-term TREND (WTIC Oil TREND resist = $102.96), so we’ll be looking to short Russian and Energy stocks today. As we look at today’s set up for the S&P 500, the range is 43 points or -2.17% downside to 1261 and 1.16% upside to 1304.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +835 (+2272)

- VOLUME: NYSE 909.51 (-10.21%)

- VIX: 17.77 -5.43% YTD PERFORMANCE: +0.11%

- SPX PUT/CALL RATIO: 1.43 from 1.77 (-19.53%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.39

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 3.01 from 2.98

- YIELD CURVE: 2.58 from 2.59

MACRO DATA POINTS:

- 8:30 a.m.: U.S. Import Price, est. (-0.7%), prior 2.2%

- 9 a.m.: Fed’s Dudley to speak in Brooklyn

- 1 p.m.: Baker Hughes rig count

- 2 p.m.: Monthly budget statement, est. (-$136.0b), prior (-$135.9b)

WHAT TO WATCH:

- Bundesbank sees German 2011 GDP +3.1% and 2012 GDP +1.8%

- German Bundestag votes in favour of motion to approve new aid for Greece -- wires

- UK Apr Manufacturing output +1.3% y/y vs consensus +3.3% and prior revised +2.2 from +2.7%

- Ally Financial delayed plans to start marketing an IPO until equity markets improve

- Obama may name Thomas J. Curry head of the Office of the Comptroller of the Currency, the New York Times said

- Samsonite sold shares at the bottom end of a revised price range in its Hong Kong IPO, raising $1.25b

- The California Public Utilities Commission opened an investigation of AT&T Inc.’s proposed purchase of T-Mobile USA

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Crop Weather Mayhem Delays U.S. Corn, Rice Planting as Prices Extend Gains

- Oil Near Highest This Month Heads for Weekly Gain on U.S. Economy, OPEC

- Copper Declines on Reduced Imports Into China, World’s Biggest Consumer

- Soybeans Fall for Second Day as Stocks Estimate May Signal Weaker Demand

- Soybean Imports Climbing in China Poised to Increase Domestic Inventories

- Gold May Advance on Concern About Europe’s Debt Crisis, Weakening Growth

- Copper Imports by China Drop in May as Consumers Run Down Local Stockpiles

- Cocoa Output From Indonesia May Slump 13% as Black Pod Spreads, Group Says

- U.S.-South Korea Trade-Accord Delay to Hurt Pork Exports, Official Says

- Oil May Decline Next Week on Signals Economic Growth to Slow, Survey Shows

CURRENCIES

EUROPEAN MARKETS

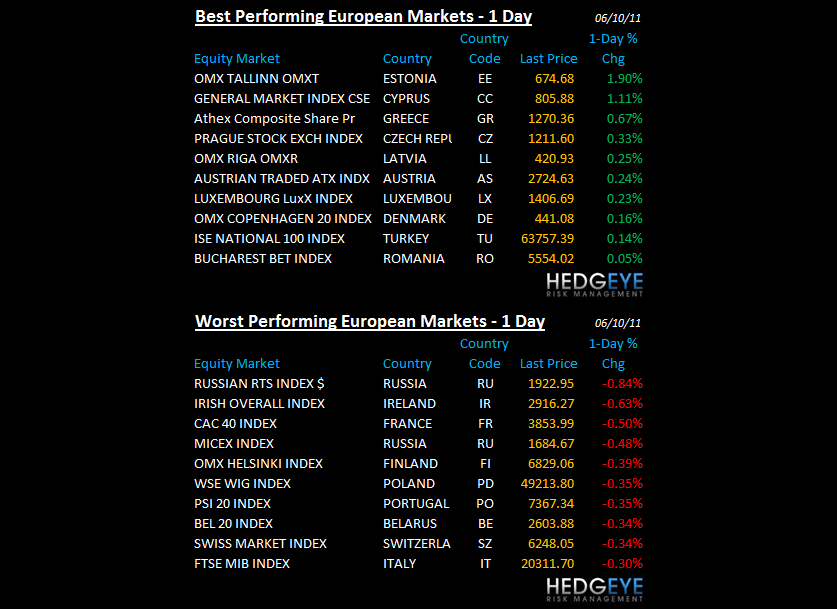

- EUROPE: an ugly day away from DAX (up small on better CPI), Spain/Italy/Greece remain broken and now Russia failing at the TREND line 1,959.

- Germany: May final CPI +2.3% y/y vs prelim +2.3%; May wholesale price index +8.9% y/y vs consensus +8.6%

- France Apr Industrial Output (0.3%) m/m vs consensus +0.4%

- UK Apr Manufacturing output +1.3% y/y vs consensus +3.3%; Industrial output y/y (1.2%) y/y vs consensus +1.3%

- UK May PPI Core +3.4% y/y vs consensus +3.4%, prior revised +3.6% from +3.4%

ASIAN MARKETS

- ASIA: mixed except Japan; KOSPI down -1.2% breaking its TREND line of 2077; India down another -1% to -11.2% YTD (were short); China no bounce; HK broken

MIDDLE EAST

Howard Penney

Managing Director