We are hosting a call this morning at 11 am with the Hedgeye Macro Team:

"MACRO & FINANCIALS: WHAT'S NEXT FOR THE FED?"

Contact us for access to the slide deck

Dial-in:

Code: 848675#

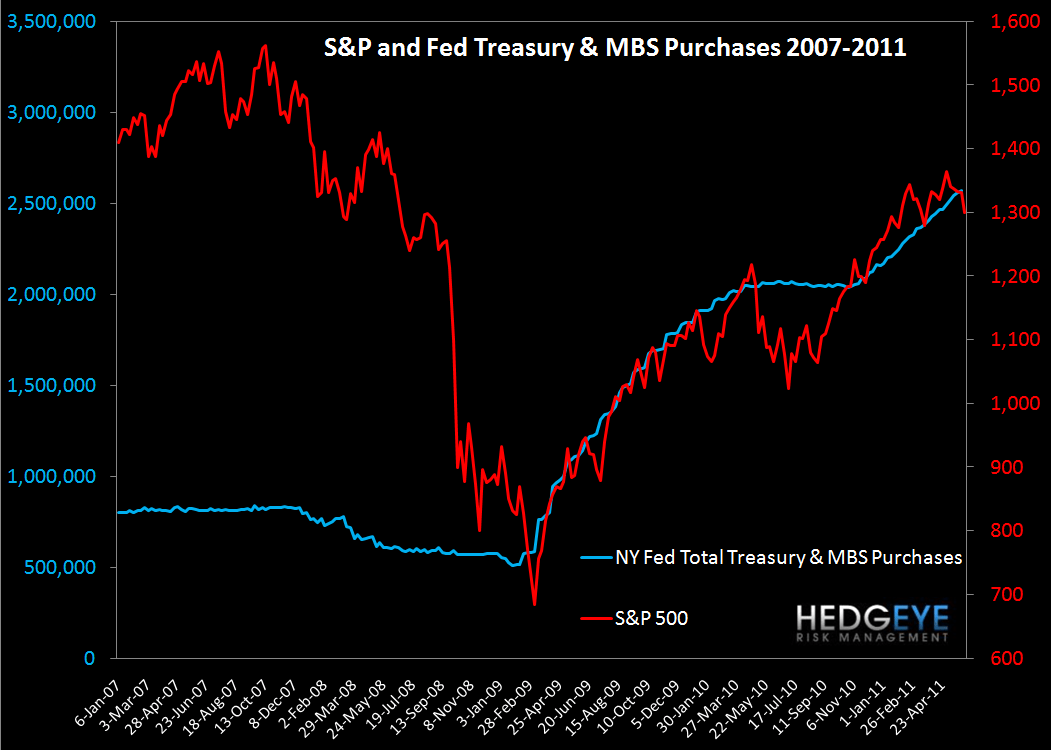

End of QE2 Presents Risks for Claims

At the end of QE1, claims stopped going down. When QE2 began, claims started falling again. While this model may be simplistic, it's shown to be effective over the last two years, as the chart below shows. When the Fed has the spigots on, the market has climbed and claims have dropped. In the drought between QE1 and QE2, claims tread water. We have been watching the charts below for several weeks with a sense of unease, and we expect that the end of QE2 in a few weeks will present another choppy period for claims.

Claims Rise 5k

Initial Claims rose 5k to 427k last week (+1k against the upwardly-revised print from last week). The 4-week rolling average dropped slightly, falling 3k to 424k. According to our model, claims must drop into the 375-400k range before unemployment can begin to improve.

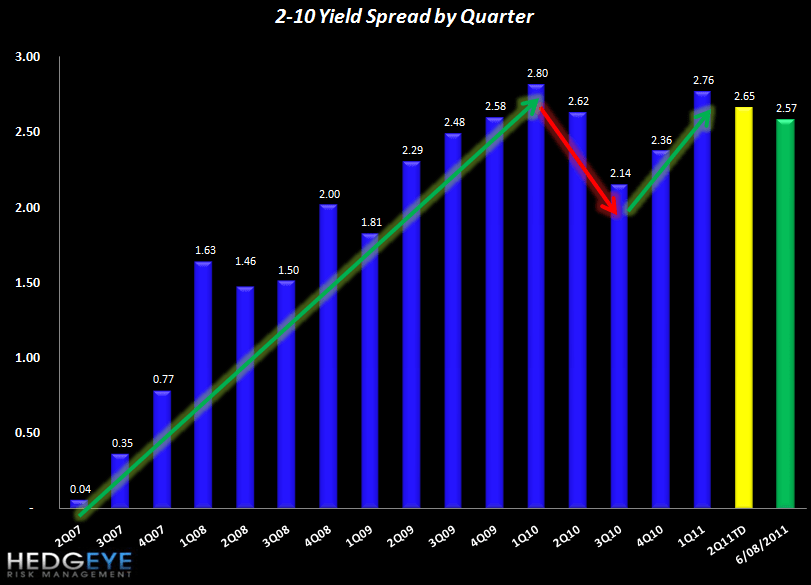

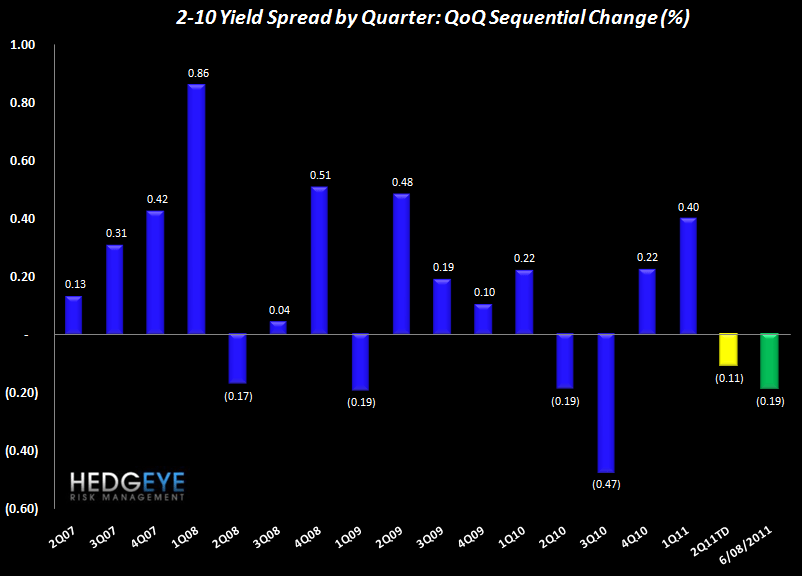

2-10 Spread

We track the 2-10 spread as a proxy for NIM. Thus far the spread in 2Q is tracking 11 bps tighter than in 1Q. This week's spread level of 257 bps compares to 250 bps last week.

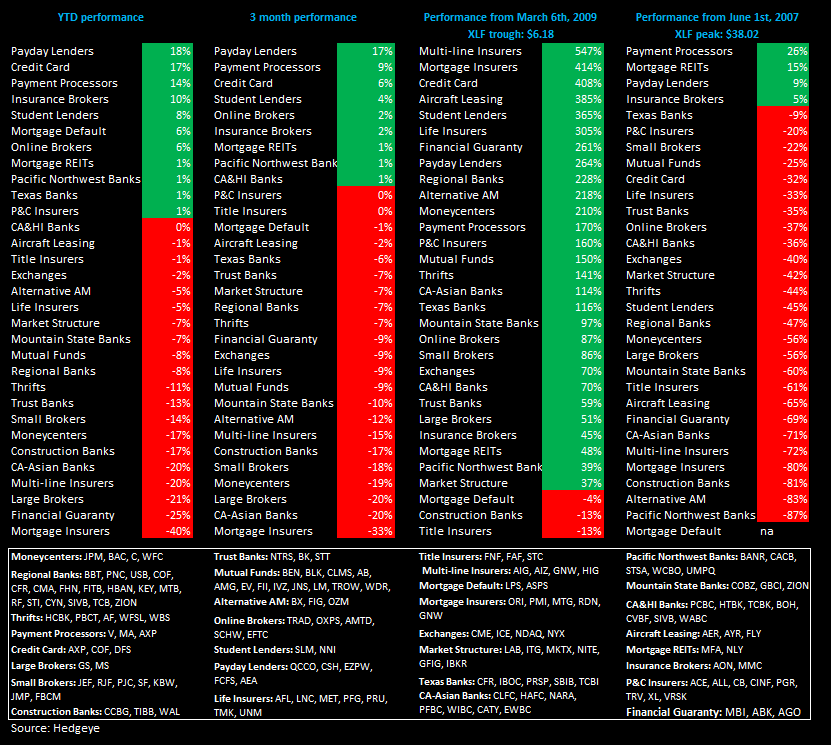

Financials Subsector Performance

The chart below shows the price performance of subsectors over four durations.

Joshua Steiner, CFA

Allison Kaptur