It may not last but ASCA seems to be bucking the negative economic data and should put up a blow out Q2.

ASCA looks interesting with the recent pullback. We still think Q2 will be a blowout. In the meantime, May state gaming revenues will be released starting later this week and we suspect they will generally surprise on the upside – similar to April – especially for ASCA. Combined with April’s strength, May should provide confirmation of ASCA's terrific near-term earnings outlook. We are currently at $0.52 versus the Street at $0.44 and our number is looking too low. We believe analysts will be forced to raise estimates and there is still a lot of room for ratings upgrades.

The following chart shows how our estimates match up against the Street’s:

State Gaming Revenues

We remain concerned about the macro picture in general but so far in Q2, ASCA has seen no impact. One possible explanation for the recent strength could be the high grain prices which may be helping some of the Midwestern economies. Of course, with significant operations in Iowa and Missouri, ASCA’s customers are certainly tied to farming. Iowa, Missouri, and Indiana could all report May revenues this week, which represents 70% of the company’s property level EBITDA.

Risk

Expansion of gaming in Illinois is a real possibility and that would hurt ASCA’s East Chicago casino. However, even if a bill is signed into law, the impact wouldn’t be felt for 3 years or so. For ASCA, East Chicago is the least significant operation behind only Jackpot and supplies only about 12% of the company’s property level EBITDA.

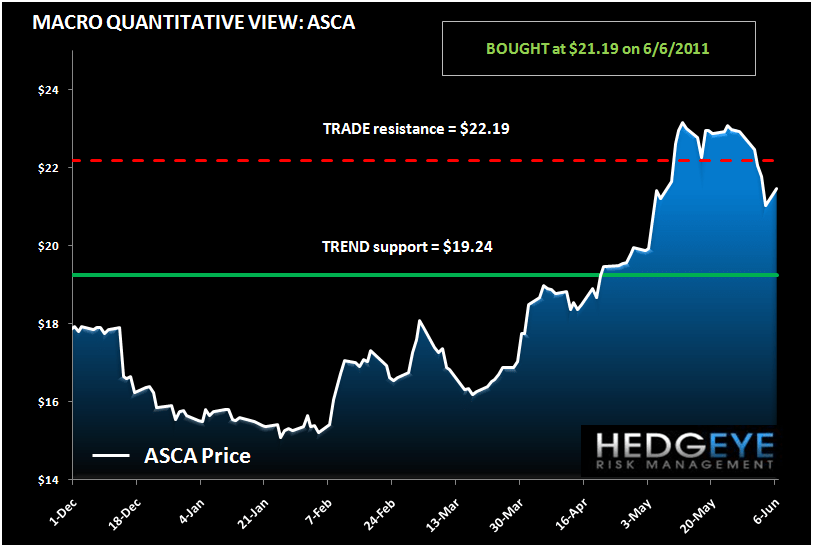

Stock Trading Update

Keith bought ASCA in the Hedgeye virtual portfolio today. He sees short-term upside to $22.19 and intermediate-term support at $19.24.