Late Friday, Becker Drapkin Management LP and Carlson Capital LP formed a group holding 5.6% of RT, with the intention to nominate three people to the board of Directors. Other that the wanting board representation, their strategy to create shareholder value was not made public. RT put out a canned response saying the board and management "are committed to maximizing the long-term value of our company for the benefit of all of our shareholders and are always open to hearing the views and opinions of shareholders as to how the board and management can continue to create such value."

I had been thinking at $9.50 RT might be interesting again on the long side, but I did not have the catalyst to see what would get the stock going again. As of Friday’s close, RT was trading at 5.6x EV/EBITDA, which represents great value, but without a catalyst it’s a value trap. The question is this: do we now have a catalyst from which we can see some upside.

From where I sit, there are three key reasons why RT might be attracting some activist shareholders.

- Attractive real estate assets and the potential for G&A rationalization.

- The company recent sales trends have put into question management current strategy.

- The CEO of RT is a controversial figure in the industry.

THE REAL ESTATE - Of the 656 Company-owned and operated Ruby Tuesday restaurants as of June 1, 2010, RT owned the land and buildings for 48% or 320 restaurants, owned the buildings and held non-cancelable long-term land leases for 215 restaurants, and held non-cancelable leases covering land and buildings for 121 restaurants. The company also owns its Restaurant Support Services Center in Maryville, Tennessee. The potential value from the Real Estate could approach $5-$6 per share, but – as is often the case – the narrative likely makes for a better story than what the reality of monetizing the assets would be.

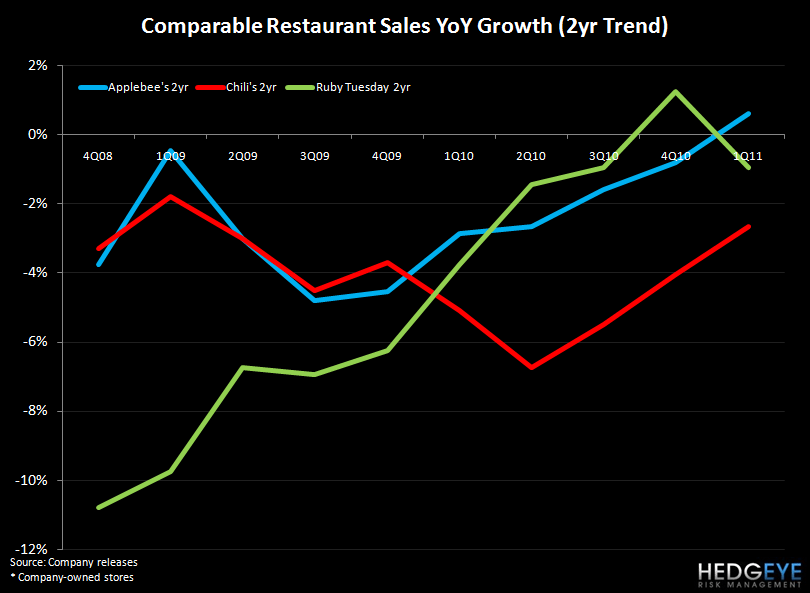

CURRENT SALES TRENDS - RT reported a decline of 1.2% in same-store sales for 3Q11, using the weather, the economy and higher gas as an excuse for the recent shortfall in sales. As a result, 2-year trends decline by 220 bps in the quarter. Clearly, the improvements in the trends at Chili’s and Applebee’s are having an impact on RT top line results. The idea of trying to provide “an ultimate $25 high quality casual dining experience” for $15 is not resonating with consumer when Chili’s is

focused on selling lunch for $6.

CREATING SHARHOLDER VALUE - Managements’ key strategy for increasing shareholder returns is through new concept conversions; converting low volume Ruby Tuesday restaurants to other high-quality casual dining concepts. The strategy is to run the entire company on what's right for each individual market instead of being a strong regional brand. As Sandy Beall said on the most recent conference call “it’s more of a roll-up or collection of communities in our company.” I’m not sure the use of the term “roll up” is appropriate or one that conjures up a high quality strategy to create shareholder value.

I take this strategy to mean that management wants to make the Ruby Tuesday concept less competitive in the marketplace, with fewer units which mean less convenience for consumers and the concept’s share of marketing voice will be declining. Essentially, management does not put a lot of value in the Brand Ruby Tuesday’s, so why should the investment community? Put another way, if you are Chili’s or Applebee’s, you are thrilled that there will be fewer Ruby Tuesdays. I understand the thought behind improving the productivity of the existing assets, but it’s hard to see how RT will build any scale with the current approach.

The other part of the company’s strategy to create value is through increasing revenue and EBITDA through franchise partner acquisitions. Overall this has limited upside, due to the fact that market is not placing a very high multiple on the cash flows of the existing Ruby Tuesdays business so why increase you exposure to that business.

I think the current group of activists share holders has an uphill battle from here although, depending on your broader market view, buying RT under $10 could yield some positive returns. As you can see from the charts below, the biggest issues RT faces is the stiff competition coming from Chili’s and Applebee’s. In a zero-sum game if the #1 and #2 brands are taking market share, a substantial piece of that probably coming from Ruby Tuesday’s.

The rhetoric from the activist group will definitely put a floor on the stock around $10 and the bull case will anchor on how they are able to influence Sandy Beall and management’s strategy. The upside may be limited, depending on how Sand Beall behaves following the press release on Friday. My gut reaction tells me that he will put up a fight and does not want to be pushed around. Sandy has controlled this company, and the board, for years so giving up some control will not be easy decision for him. I would think that bringing some fresh thinking to the board will be good news rather than bad, but whether or not Sandy Beall agrees with me is the only thing that matters.

Howard Penney

Managing Director