European Positions: Long Germany (EWG); Short Spain (EWP)

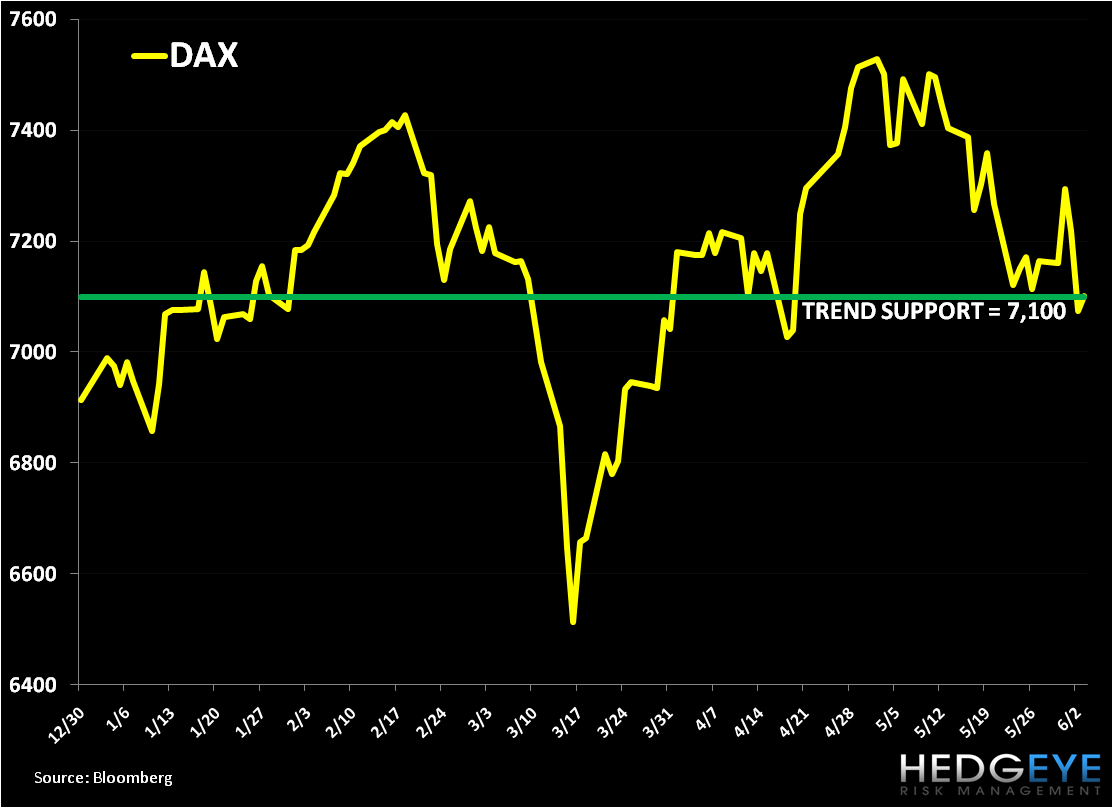

To borrow a phrase from Keith, Europe’s latest high-frequency data feels like a Wet Kleenex, which is to say not great and leaving an uneasy feeling. In particular, our conviction in Germany (in the Hedgeye Virtual Portfolio via the etf EWG) has recently waned. PMI (Services and Manufacturing) and confidence surveys have declined in recent months as inflation accelerates and broadly sovereign debt contagion risk remains in the forefront. From a quantitative setup the equity markets of Germany to Sweden to the PIIGS are all broken on the intermediate term TREND: this often is an indication to short a market, or get out of the way. Therefore we will be managing our long position in Germany accordingly as the DAX is trading right at its TREND line of 7,100 (see below).

PMI Services data out today for May confirmed the Manufacturing readings released on Wednesday—declines month-over-month for the major economies and the Eurozone average (see charts below). On the PMI survey, 50 is the line in the sand, with figures above 50 indicating expansion, and below indicating contraction. Spain is firmly in the latter camp, with Manufacturing at 48.2 and Services dancing on the line at 50.9. Equally Italy’s Services is flirting with the line (50.1) as is Ireland Services (50.5). While Greece is taking the spotlight, we remain decidedly bearish on all the PIIGS (we’re currently short Spain via EWP), as we expect them to underperform their target debt and deficit reduction targets.

On the EUR-USD, we’re bearish as the pair reaches the top side of our trading range at $1.44, and believe it will bounce around in a range to $1.40 alongside headline risk, but ultimately find support as the EU continues to socialize the periphery’s fiscal imbalances at every step.

Matthew Hedrick

Analyst