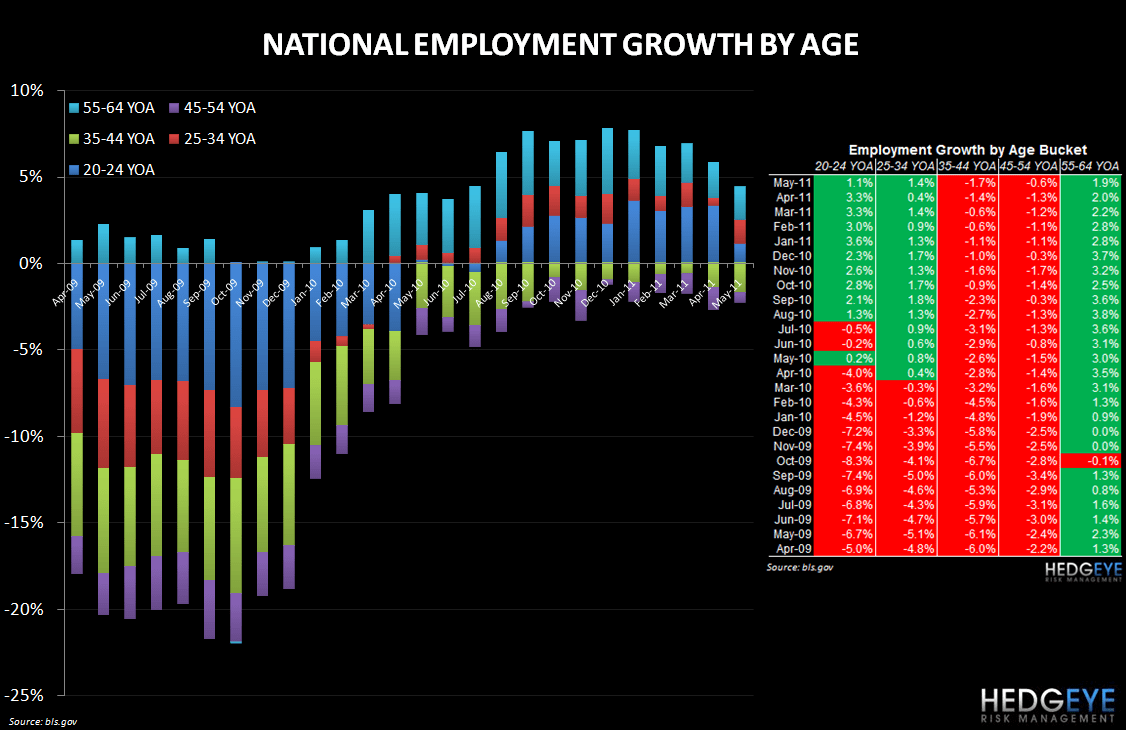

Employment data less positive for QSR, on the margin.

The overall jobs picture is causing concern here at the market open but, looking into the details that are most pertinent for QSR, it is the decline in the absolute growth level of employment in the 20-24 YOA cohort that caught our attention. January through April brought 3%+ growth in the employment level among 20-24 year olds. May’s number indicated a mere 1.1% in employment growth for that age bracket, which is a glaring red flag for QSR. As a reminder, much of the positive sentiment from management teams over the past number of quarters has anchored on an improving employment landscape. This view certainly doesn’t corroborate with Hedgeye’s macroeconomic view and, today’s news being the most recent instance, the data is also calling into question the idea of a sustained recovery in employment.

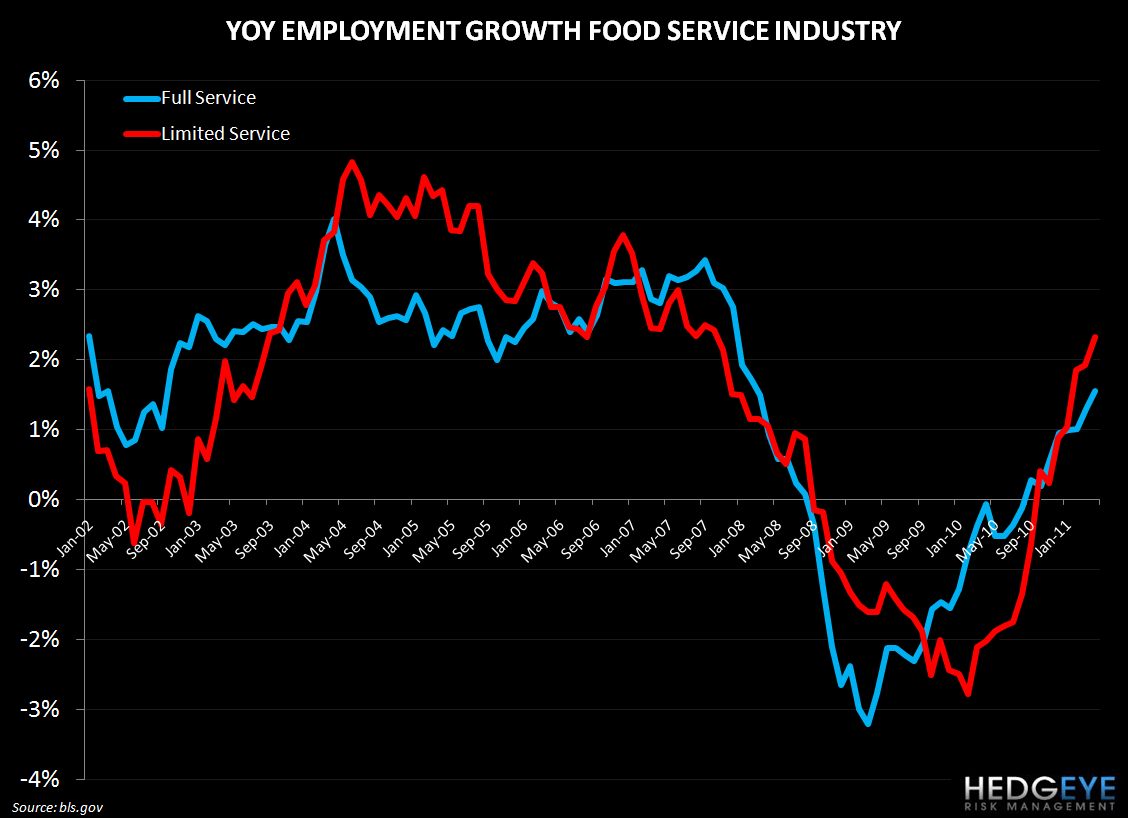

As the second chart below shows, employment growth in the food service industry continued its upward trajectory in April. Clearly, restaurant management teams can only react to the economic reality they are faced with, and the data is lagging one month behind the data in the first chart.

Howard Penney

Managing Directory