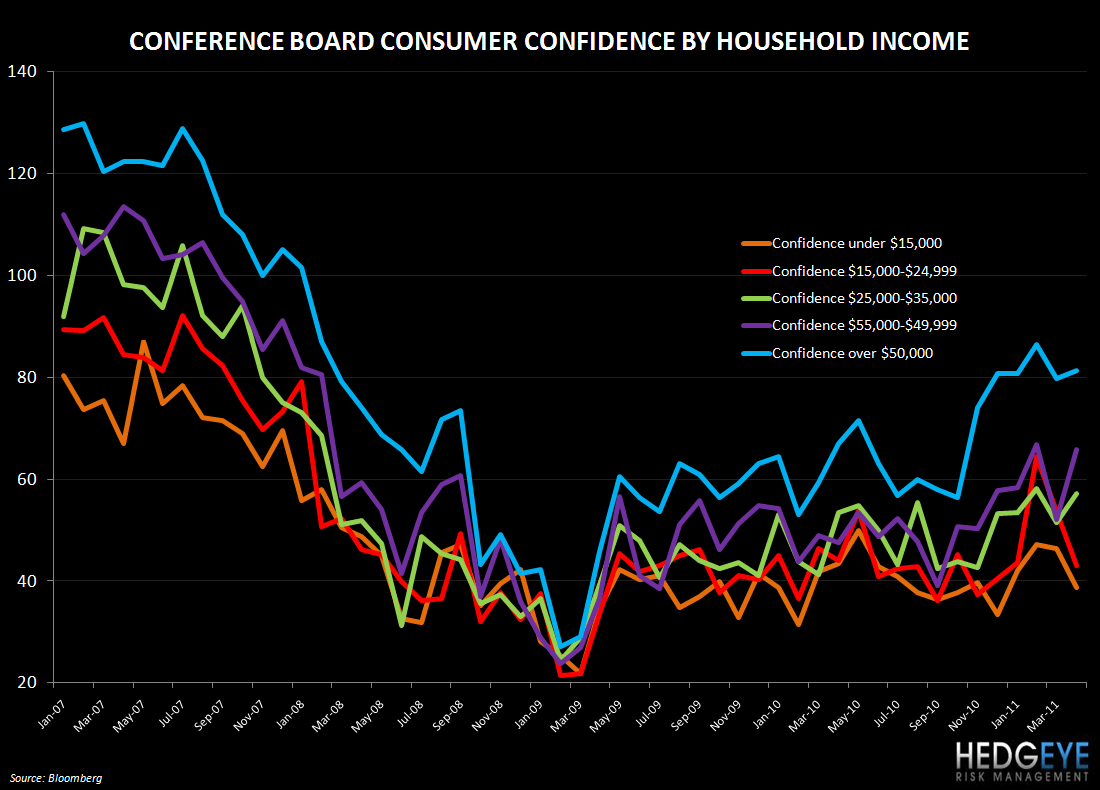

Consumer confidence was disappointing onTuesday in general and the trend among low income cohorts suggests that the discounting environment in the restaurant space is far from over.

As the chart below shows, confidence levels among households in lower income brackets is suffering while confidence levels among households earnings $50,000 or more per year remain high. The consumer at the high end is performing well; steakhouses and higher average check concepts have seen robust performance metrics of late while lower end concepts are continuing to rely on discounting to drive comps. With high food costs compressing restaurant margins, many companies are either taking price or signaling their intention to do so. Higher food and fuel costs are also impacting consumers, however; lower income cohorts’ confidence levels have declined sharply from February.

Some consumer data points have emerged over the past couple of days that corroborate with this view:

- Saks May comp sales were up +20.2% in May.

- Nordstrom reported May comps +7.4% versus StreetAccount +5.7%.

- TGT sales came in at +2.8%, below StreetAccount consensus, and the CEO commented that “guests today continue to shop cautiously in light of higher energy costs and inflationary pressures on their household budgets”.

- TJX reported comps +2.0% versus StreetAccount +3.2%.

- JCP reported May comps -1.0% versus +3.4%.

- DRI is focusing on value this summer with an LTO of a $15 four-course meal. The “$15 Seafood Feast” includes soup, salad, entrée, dessert and unlimited Cheddar Bay Biscuits and runs through July 25th.

Restaurant companies from CMG to SBUX are going to be taking price to offset inflation. How successful this strategy is will partly depend on where their core consumer is drawn from and how inelastic demand is for their product. Casual dining is particularly prone to this effect, in our view. While CBRL may continually raise prices, traffic is negative quarter after quarter. Other companies, like DRI, will continue to discount heavily to maintain traffic. For the foreseeable future, though, the economic health of each concept’s core consumer will be the primary driver of sales. The consumer confidence data, and company commentary, point to a continuing divergence between the high- and low-end concepts.

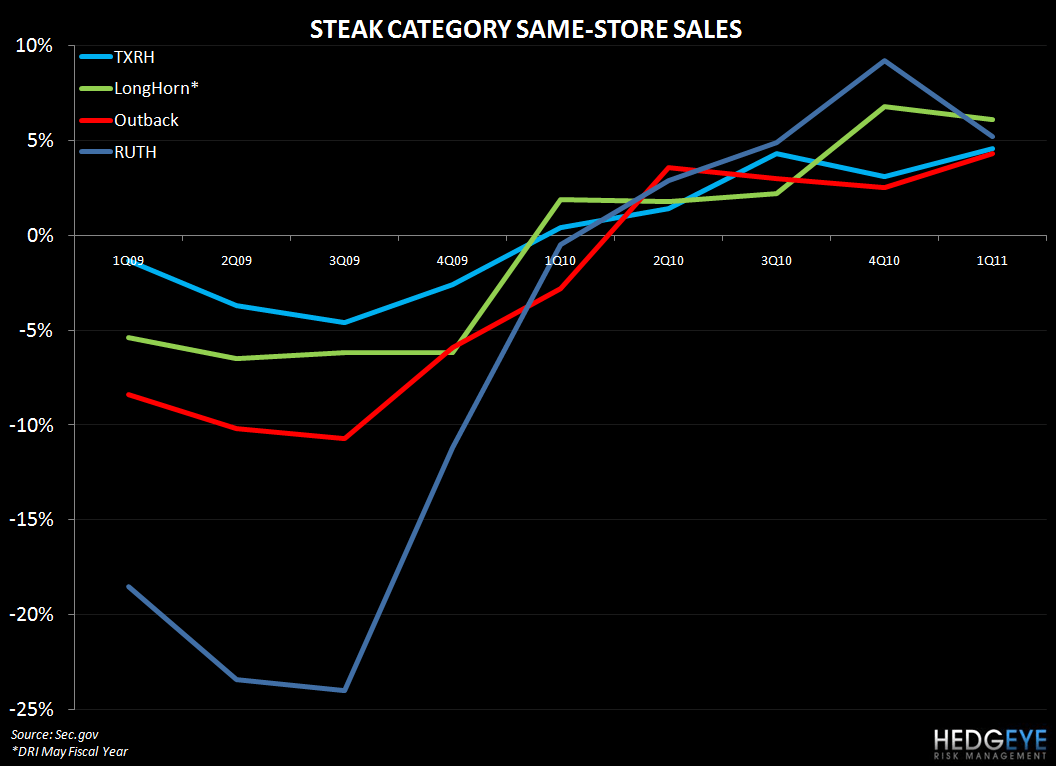

How long the robust confidence levels continue for the upper income bracket is uncertain. The Bloomberg Consumer Comfort Index for people with household incomes over $100,000 per year was -6.3, negative for a third week and below the 2010 and 2011 averages. According to Langer Research Associates, the firm that compiles the data for the Bloomberg Index, the 1.4% drop in the S&P 500 in May, the biggest monthly decrease in shares since August, may be starting to concern people in higher income brackets. Steak concepts, in the event of a further downturn in economic conditions, may begin to retrace some of the significant progress they have made in top-line growth, as the chart below shows.

Howard Penney

Managing Director