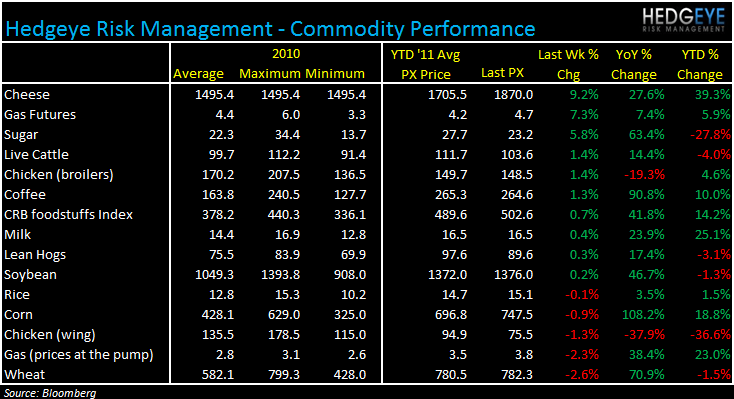

Now that 1Q11 earnings are well and truly in the rear-view mirror, the resounding message from management teams is that commodity costs are set to weigh on earnings over the next couple of quarters. While commodities took a brief pause in May overall, the direction last week was generally to the upside. Chicken costs remain low on a year-over-year basis, with wing prices declining 1.3% week-over-week while corn prices also declined slightly over the week.

Cheese

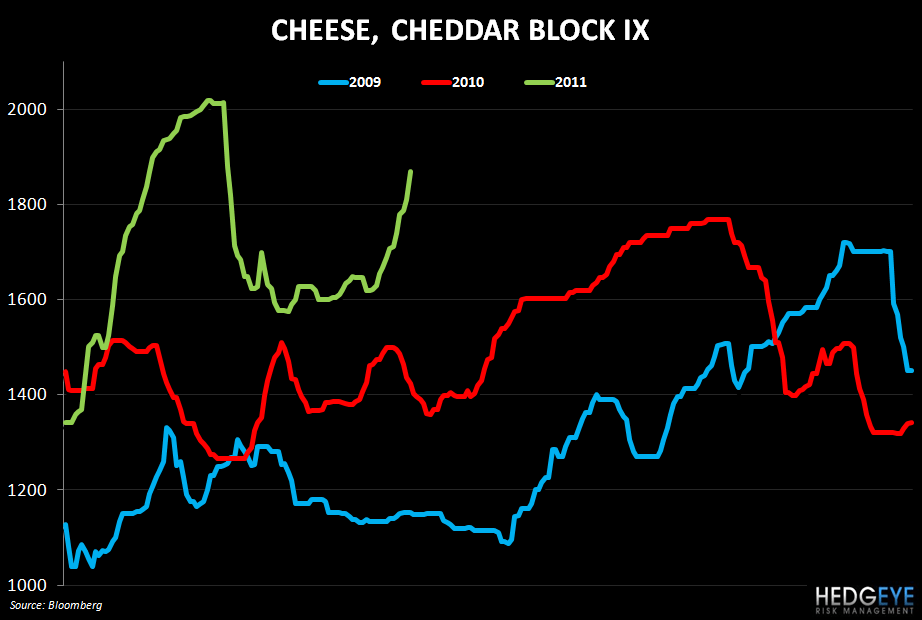

Cheese prices outperformed strongly last week as higher feed costs are squeezing dairy profitability to its worse levels since the summer of 2009, according to USDA data. 2009 was the worst year in the dairy industry since the Great Depression. While wheat and corn did decline week-over-week, price levels remain extremely elevated versus year-ago levels. The gain in cheese prices is a negative for DPZ, PZZA, and YUM’s Pizza Hut. While DPZ has cheese prices has a contract that eliminates one third of the cheese market volatility, the current trajectory of cheese prices is negative for restaurant operating margins. Below is some commentary on cheese prices from management teams:

JACK (5.19.11): Cheese accounts for 6% of our spend and we continue to expect a 15% increase for the year.

CMG (4.20.11): As we move into 2011, we’re expanding our use of cheese and sour cream made with milk from cows

CPKI (5.5.11): I’m estimating it’ll be around $1.80 on a go-forward basis, probably for the back-end of the year.

DPZ (5.5.11): But we've got a lot of things locked in through the end of the year. And really the one to watch as always is cheese and our best bet right now is that it's going to stay relatively close to where it is right now but cheese is the one that often gives the biggest surprises either up or down and that's the one to kind of watch but assuming cheese stays relatively flat from here on out then, the absolute food costs from – through the rest of the year are probably going to stay pretty consistent with where they were in Q1 which to your point means the percentage year-over-year increase will probably ease a little bit over the course of the year.

PZZA (5.4.11): We've got $1.70 or so built in for our full year cheese price.

CAKE (4.20.11): We expect to have slightly lower fresh fish costs, slightly lower cheese prices, than last year.

Beef

Beef prices are front and center for QSR companies as we head into summer. Increased traffic on the interstate should yield seasonally higher traffic for most QSR chains but, with gas prices elevated, the challenge facing management teams is meeting customers’ value demands while maintaining margins. WEN hiked its commodity guidance for 2011 to 5% to 6% from 2% to 3% largely due to higher beef prices. Elevated grain prices continue to point to higher meat costs as demand remains strong. Below is some commentary on beef prices from management teams:

JACK (5.19.11): Beef accounts for more than 20% of our spend and is the biggest factor driving the change in our guidance. For the full year, we are now anticipating beef cost to be up nearly 14% versus our previous expectation of 9% inflation. We expect beef cost to be up approximately 14% to 15% in the third quarter. Our third quarter forecast for beef 90s, in the low $2 per pound range and for beef 50s, we expect prices to average in the $0.95 to $1.05 per pound range in Q3.

WEN (5.10.11): Beef accounts for more than 20% of our spend and is the biggest factor driving the change in our guidance.

TXRH (5.2.11): Right now, we've got just over 65% to 70% of our commodities are locked for this year and that includes some floors and ceilings on certain commodities and, within that, 90% of our beef is locked and we've also got some floor and ceiling arrangements on some of our beef tips.

Chicken Wings

Chicken wing prices declined again last week, spelling good news for BWLD. Excluding chicken (wings and broilers), the commodities in our monitor are up almost 43% YTD. Chicken wing costs are down 38% YTD.

Howard Penney

Managing Director