This has already been a fascinating day, starting at 5am when the futures were indicating that the DOW would be up over 100 points on the back of news that a new bailout package for Greece could be around the corner. AT the time of writing, the VIX is up 2%, USD is down 0.5%, the S&P 500 up 0.47% and the Euro is up 0.77%. The Correlation Risk is being put right back on the table for June.

Looking at the data closer to home the economic numbers continue to roll over, confirming that STAGFLATION is a real and present danger and increasing the likelihood that the United States could be heading towards another crisis. The major data points pertaining to the U.S. economy that were released today were all ugly. But who cares?

Today’s MACRO data points are ominous for this Friday’s employment report.

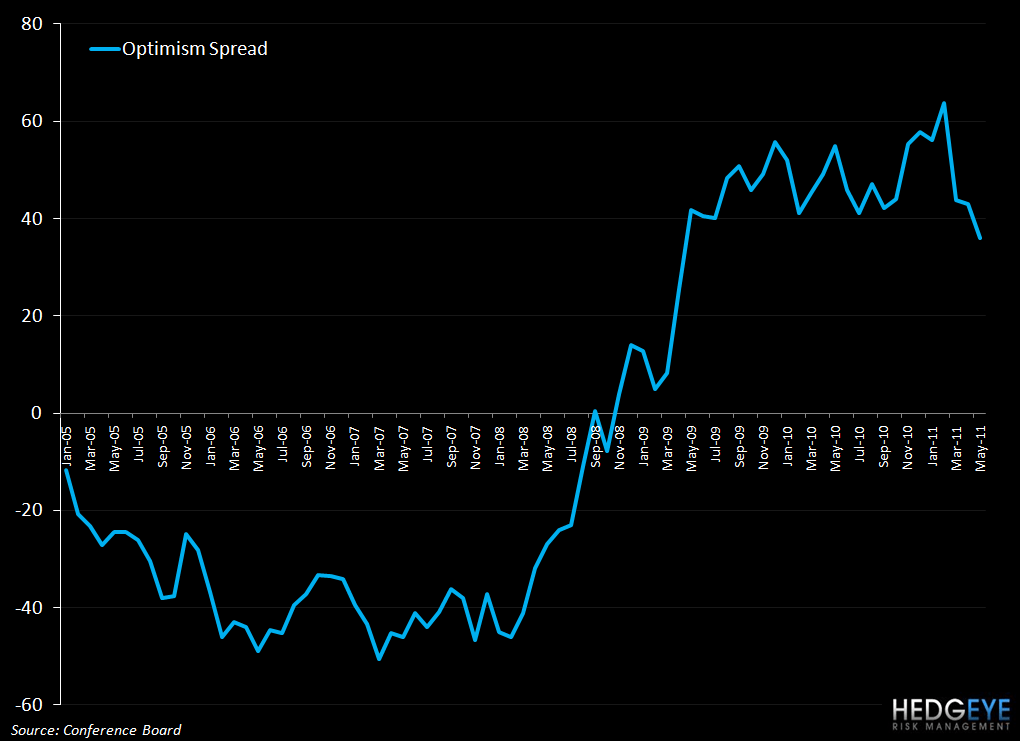

CONFIDENCE

The Conference Board index of consumer confidence dropped 5.2 points in May; the index is now at its lowest level since November. The Hedgeye Optimism spread continues to contract, as the expectations component led the decline falling to 75.2 from 83.2 (previously 82.6). The present situation component dipped to 39.3 from 40.2 (previously 39.6). Overall, the assessments of future business and labor market conditions fell in May.

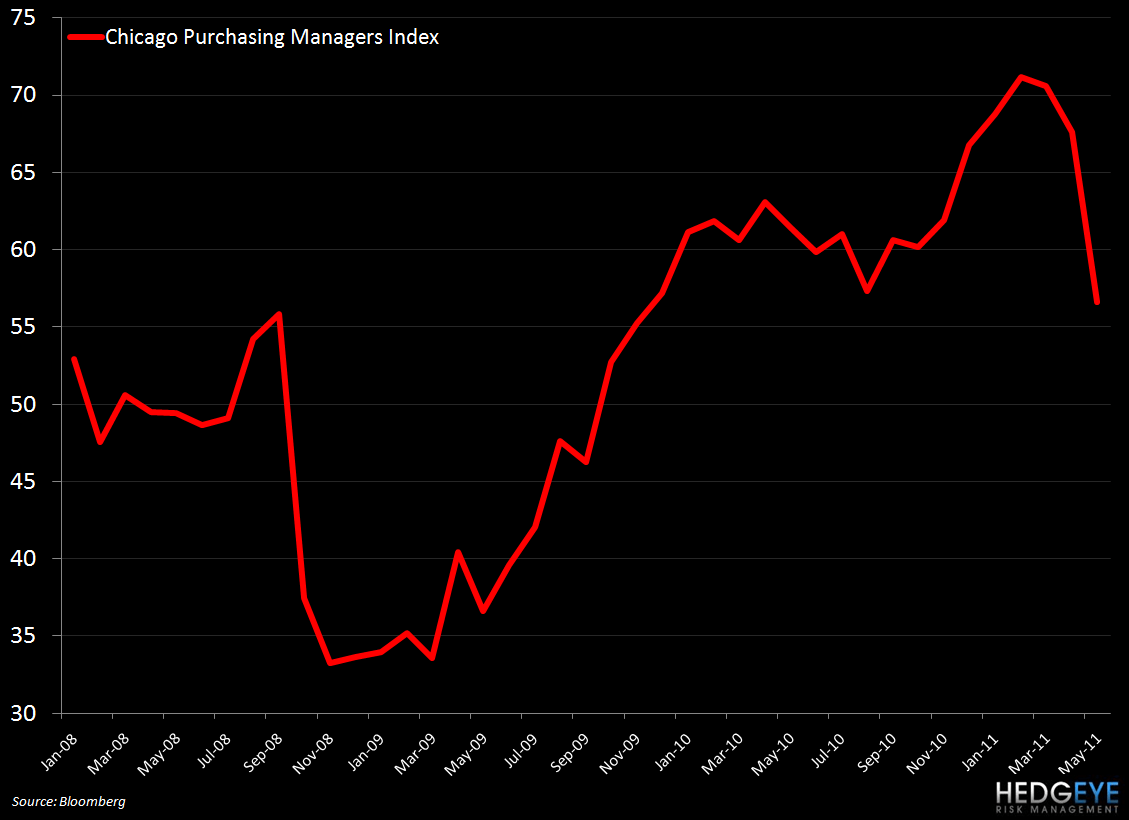

MANUFACTURING CONDITIONS

The downshift in U.S. growth has caught up to manufacturing sector as the ISM-Chicago index fell by 11 points to 56.6; the decline puts the index below its first quarter average of 70.2. The results look to be more than supply-chain disruptions, as new orders have fallen for three consecutive months, declining 22.4 points. In addition, the gap between new orders and inventories (a proxy for future production) was -8.1 in May, compared with April’s 12.8. The new orders to inventory/gap turned negative for the first time since March 2009. This puts STAGFLATION in play for the balance of this quarter and next.

HOUSING

Today’s Case-Shiller number was disappointing with home prices officially double-dipping in March. The Case-Shiller 20-city NSA series fell -0.77% in March versus February and -3.6% versus a year ago. 13 of the 20 cities included in the composite hit new lows in March. Hedgeye’s Financials team has been way ahead of this call, as the chart below shows, and their demand model is calling for an 18% downside in home prices in 2011 versus 2010.

THE FRIDAY JOBS CLOUD

Today’s MACRO data points are ominous for this Friday’s employment report. Manufacturers’ sentiment has been squeezed by higher fuel and food costs and the challenges being posed by the earthquake and tsunami in Japan are not helping. The recovery that has generated so much optimism in the U.S. has been largely led by manufacturers as exports rose and business investment picked up and could unravel in short order if manufacturing continues to slow. While housing’s double dip is not attracting much attention, joblessness is still the most pressing of consumers’ concerns.

Howard Penney

Managing Director