TALES OF THE TAPE

- The Coffee trade continues - CBOU, GMCR, PEET and KKD continue to power ahead on good volume

- JACK sales remain down - LA Times - The article talks largely to analysts and notes that the company's attempts to attract a slightly wealthier client base might actually backfire. Maybe the LA Times should be talking to analysts that know that they are talking about, because the strategy is not to go after wealthier client base. Here are the comments from the CEO speaking at the latest conference “Lastly I want to reiterate that our number one priority this year is to drive sales and traffic at Jack in the Box through investments we made to enhance our food, service and facilities. We recognize that these investments may depress margins in the near-term but should build sales and brand loyalty over the longer term. To recap the steps we are taking, we are investing resources to improve many of our top-selling core products and continuing to emphasize both premium products and value promotions in our marketing calendar. We're investing resources to improve the guest service by delivering a more consistent experience. And Phase two of this system-wide plan is focusing on improving speed of service and other key drivers of guest satisfaction.”

- Yesterday, BWLD was added to short term buy list at Deutsche Bank

- THI is still MUM on CEO’s departure; down for the second day on accelerating volume

- MCD was weak in a strong tape….. If the USA prints a 3% SSS for the month of May that suggests traffic is slowing

- Overall Casual Dining had a great day yesterday

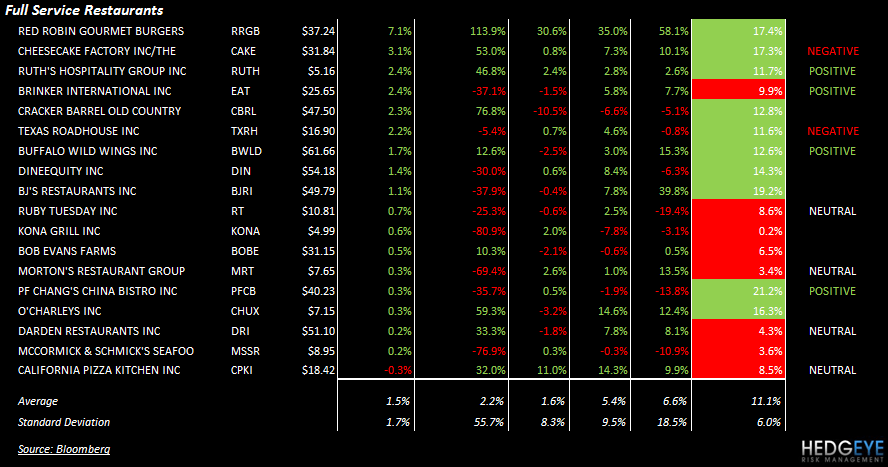

- RRGB - The good news is getting baked in

- CAKE - Up on strong volume and Im negative

- RUTH and EAT (two names I like) were up on strong volume

- Corn prices rose for a second day Thursday on concerns that heavy rains could hurt this year's harvest. Corn rose 0.4%, while wheat rose 2.3% and soybeans rose 0.6%. Wet weather in parts of the Midwest has made it difficult for farmers to plant corn, even as demand remains high around the globe.

- Google has partnered with MasterCard and Citi in its Wallet application, which is designed to be a combination credit card, rewards program and coupon case when customers tap their smartphones at the register. Also on hand were Google's posse of retail and restaurant partners, including Subway, American Eagle and Macy's, which will enable Wallet payments and offers when the platform launches this summer.

Howard Penney