Another deal for DKS? Accretive, perhaps. But incremental? Perhaps no. keep in mind that this might not be entirely incremental. Check out the timing of DKS’ prior acquisitions. July 2004. Feb 2007. Nov 2007. ALL of these deals occurred when the base business was slowing. We don’t want to suggest bad behavior in this instance when there’s not even a bid on the table. But this is an important factor to keep in mind if you see something hit the tape.

It looks like Texas-based Academy Sports may be on the block.

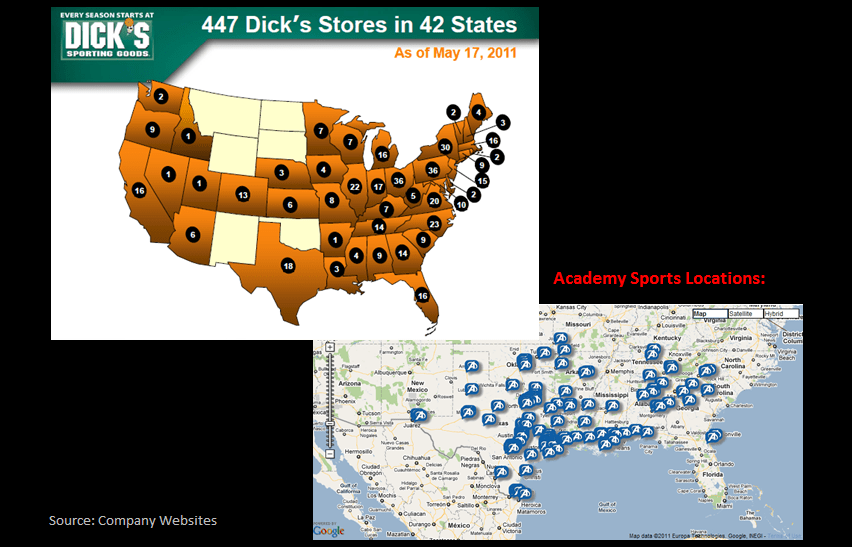

This shouldn’t come as much of a surprise given the lack of a clear succession plan following the passing of Academy’s founder Arthur Gochman this past October. It’s been a family run business through and through and while Arthur’s son has taken over at the helm, it makes sense for the family to shop the company to see what they can get with deal activity picking up in retail. With over 125 locations, Academy surpassed $2Bn in revenues back in 2007 according the company’s website and currently generates approximately $100mm in EBITDA – owners are looking for a 10x takeout offer.

A quick look at the company’s profile suggests that if competitors are looking at the deal, DKS is the most likely candidate. HIBB’s store format at an average size of 7,000 sq. ft. is a completely different concept altogether compared to Academy’s 60,000 sq. ft. box – they’re out. The Sports Authority while more similar in footprint at an average of 45,000 sq. ft. has a high degree of overlap with Academy locations so they would be forced to either close a substantial amount of stores or face some degree of cannibalism neither of which sounds appealing. Plus, TSA is still under the wing of Leonard Greene and waiting to come out. We cannot imagine that sponsors are willing to pump a billion dollars into this ill-timed investment.

That leaves us with Dicks. There’s virtually no overlap between the two companies and the average footprint is nearly identical with DKS over 50,000 sq. ft. Also, Academy and its bankers are no dummies… They’re throwing out a 10x EBITDA multiple. Look at DKS’ past deals. Golf Galaxy and Galyan’s for 10.2x and 10.1x, respectively. (Chick’s, which it bought in 2007, was a small real estate play with undisclosed financials).

Academy is a quality retailer, and it dominates the space in perhaps the most important sporting goods market in the country. Will DKS pay 10x EBITDA? Without a doubt. Does the balance sheet allow it to do so? Probably. With $500mm currently on the balance sheet and another ~$200mm in FCF expected this year, DKS could certainly make a bid and stay below 30% Net Debt/Cap.

In addition, DKS leases EVERY single store, and even most of the fixtures in its stores. Its strategy there is very aggressive. Could it restructure parts of Academy in a way that puts obligations off balance sheet? Probably. Does it bug the heck out of us that the Street continues to look through this for DKS – as if its most important asset (its stores) were free of a capital charge? Absolutely! But that probably won’t matter.

Depending on the financing structure – AND assuming that the reported $100mm in EBITDA is a real number -- a $1Bn price tag could be anywhere from $0.10-$0.20 accretive to the P&L.

But keep in mind that this might not be entirely incremental. Check out the timing of DKS’ prior acquisitions. July 2004. Feb 2007. Nov 2007. ALL of these deals occurred when the base business was slowing. We don’t want to suggest bad behavior in this instance when there’s not even a bid on the table. But this is an important factor to keep in mind if you see something hit the tape.