THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - May 26, 2011

Mean reversion bounces to lower-highs across all of the big macro stuff that matters (Euro, Oil, SPX futures, etc), but nothing has changed in terms of the big lines in the sand that ultimately matter – primarily USD support and UST yield resistance.

- USD immediate-term TRADE range = 75.65-76.26 (wants to make higher-lows and higher immediate-term highs)

- Euro immediate-term TRADE range is tight = 1.39-1.41, with $1.41 being its new TREND line of resistance

- Oil immediate-term TRADE range = 96.89-101.57, so we’re looking at shorting oil ahead of another USD rally

As we look at today’s set up for the S&P 500, the range is 19 points or -0.79% downside to 1310 and 0.65% upside to 1329.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 934 (+1172)

- VOLUME: NYSE 961.30 (+10.70%)

- VIX: 17.07 -4.21% YTD PERFORMANCE: -3.83%

- SPX PUT/CALL RATIO: 1.30 from 1.84 (-29.07%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 20.89

- 3-MONTH T-BILL YIELD: 0.06%

- 10-Year: 3.13 from 3.12

- YIELD CURVE: 2.61 from 2.61

MACRO DATA POINTS:

- 8:30 a.m.: GDP Q/Q: 2.2%, prior 1.8%

- 8:30 a.m.: Net export sales, cotton, corn, soybean

- 8:30 a.m.: Jobless claims, est. 404k, prior 409k

- 9:45 a.m.: Bloomberg consumer comfort, est. (-47.0), prior (-49.4)

- 10:30 a.m.: EIA natural gas storage change, est. 95, prior 92

- 1 p.m.: U.S. to sell $29b 7-year notes

WHAT TO WATCH:

- Google holds press conference in NY; may discuss mobile- payments system, Digital Trends says

- NY Fed said to probe Goldman Sachs’s mortgage allegations: FT

- Marriott expects to recognize several hundred million dollars in cash tax benefits from the spin off of its timeshare business

- Bank of America pressured by states to change mortgage practices - Bloomberg

- CEO Mark Zuckerberg says Facebook "[doesn't] have the DNA to be a music company or movie company" - GigaOM

- Starbucks raises bagged coffee prices by 17% - WSJ - The WSJ reports that the price increase will take effect 12-Jul, and comes after they raised supermarket bagged coffee 12% in March.

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Global Food Production May Be Hurt as Climate Shifts, UN Forecaster Says

- Oil Falls From Two-Week High in New York on Bets That Recovery Is Too Slow

- Wheat Gains for Second Day on Concern Dry Weather in Europe Damaged Crops

- Gold Falls as China Bond-Buying Speculation Curbs Demand; Silver Declines

- Sugar Rises for Third Day on Indications of Stronger Demand; Coffee Gains

- Copper May Rise in London Trading on Prospects for U.S. Demand on Growth

- Platinum Surplus Seen Jumping Eightfold After Japan Quake Cuts Car Output

- Gold Companies May Face $100 Billion Liability for Ill South Africa Miners

- Rusal Leads $10 Billion Borrowing in Metal Producer Revival: Russia Credit

- Rail-Car Orders at 13-Year High Ratify Buffett’s U.S. Bet: Freight Markets

- ‘Stressed’ Carbon Credits Drawing Record Demand in Europe: Energy Markets

- Natural Rubber Output Growth to Miss Estimate This Year, Association Says

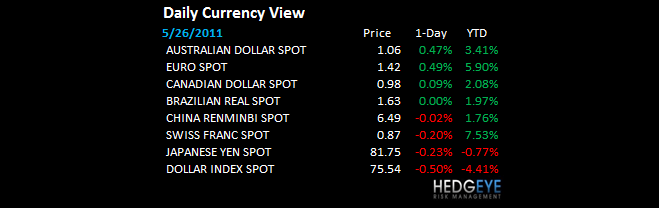

CURRENCIES

EUROPEAN MARKETS

- EUROPE: soggy Kleenex this morn w/ DAX, Denmark, and Russia all flagging negative divergences - not what the bulls need to see (sold Sweden)

- Switzerland calls for phasing out of country's five nuclear reactors - FT

- Germany Apr Import Prices +9.4% y/y vs consensus +9.9% and prior +11.3%

- France May Consumer Confidence 84 vs consensus 83

ASIAN MARKETS

- ASIA: wicked volatility off yesterdays bombed out lows; Vietnam +3%, KOSPI +2.8% - but China down for 4th day of 4 this wk; India still lags

- Japan April corporate services price index (0.8%) y/y, (0.1%) m/m

MIDDLE EAST

Howard Penney

Managing Director