Conclusion: PSS couldn’t have printed a worse number if it tried. Any analyst worth his/her salt should question the business model and value proposition. We certainly are. In the end, numbers are coming down and the stock is cheap – but that’s not enough. The good thing is that Rubel will make the changes he has to – even if they are draconian – and in short order. We’re not inclined to sell into the puke with the rest of the herd. But rather wait and see where estimates shake out for the quarter and the year, and get a sense as to whether people are negative for the right reasons.

I think it’s fair to characterize this quarter out of PSS as an unmitigated disaster. With a -7% comp, 265bp Gross Margin hit, and 23% growth in inventories, I don’t think that they could have printed a worse number if they tried. No joke. Retailers can usually trade off these three factors such that one improves, while the other one or two erodes. Here, there appeared to be complete lack of control.

What I won’t do is sit here and try to blame the weakness in the business on weather, holidays, unemployment and economic malaise. The reality is that every other retailer is facing the same factors, and PSS underperformed all of them by a country mile.

Maybe the weather factors have some validity (mgmt noted that they were on plan until 3.5 weeks before end of quarter). But quite frankly, the ‘weak economy and high unemployment’ factor is getting old. In fact, it’s not the level of unemployment that matters as much as the delta, and that actually improved 90bp yy and 50bp sequentially. In other words, employment should be helping, not hurting.

Gas prices? We’ll give them a pass there – but that doesn’t mean that our growth expectations should come down, but simply that this team needs to have a proactive plan in place to grow in light of other challenges – however sudden they may rear their ugly heads. PSS lost share in its base business this quarter, and a lot of it. That’s unacceptable to us.

The big disconnect is that we genuinely think that this company has assembled a better management team than a company the size of PSS probably deserves – that is pretty clear to anyone that has met the top dozen-plus managers that Rubel confidently puts in front of the Street. And yet PSS STILL fails to perform.

On the call, Rubel made some kind of comment like “you’re all very good at your research, which is why the stock went from $22 to $18 in the past few weeks.” Perhaps he was right to an extent – but we’re sorry to inform that the market was in no way, shape or form expecting this mess. Based on after hours trading, we’re looking at a $14-$15 stock. That’s probably deserved.

So there are several questions to be asked and answered.

- What’s the earnings power of the company?

- Does it matter?

- Other ways to unlock value?

- Ultimately, what’s it worth, and is there any reason to own this stock?

1. Earnings Power

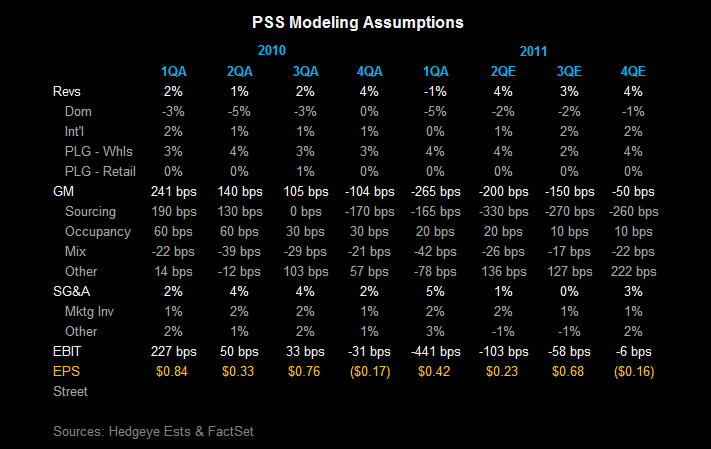

We’re shaking out at $1.17 and $1.66 for FY11 and FY12, respectively. Broadly speaking, our model calls for a slight sequential pick-up in comps – which by default needs to happen by way of clearing the 23% growth in inventory – though we have gross margins coming down accordingly. We’re holding PLG growth at 15% for this year, and conservatively at 11% next year. We’ve got gross margins up 100bp next year due to a better relative comp (a -7% has a nice way of destroying occupancy leverage), but are taking SG&A up to account for growth capital at Saucony and Sperry to maintain brand momentum and Payless International for expansion. Interest expense should continue to come down by about $1.5mm per quarter as PSS de-levers.

2. Does it Matter?

I wonder if people will really care one way or another about earnings power right now. It’s easy to put on the bear hat and view this as the levered, small cap, ultra-volatile name that it is, where the core business is structurally lackluster at best. Our view around PSS the name focused on having a flattish base business – that was +/- 3% in a given quarter/year – that funded a growth PLG businesses and enabled de-levering and repo. We still like that thesis…but unfortunately, EBIT in the quarter was down by $40mm, or 48% while PLG accounted for an incremental $1mm in EBIT. Our thesis simply did not work this quarter. It didn’t work in 4Q, either.

3. Other Ways To Unlock Value

Earnings power not mattering has pros and cons. The biggest ‘con’ is that the name is being taken outside behind the barn and shot. The level of concern with this business won’t be whether or not it will earn $1.50 – but whether or not it should actually exist as it appears today.

That brings us to the ‘pro.’ I don’t think that this company is afraid to make the draconian call and close a meaningful portion of its stores. Rubel knows his numbers. Talk to the guy… He knows store performance at the micro level – which is impressive when you have 4,800+ stores. He knows spending by consumer, by price point, geography, etc…better than most managers I know.

That said, let’s do some simple math. Core Payless accounts for $2.5bn in revs, with PLG at about $1bn. But PLG accounts for about $70-$75mm in EBIT. Yes, that means that core Payless stores are currently churning out about $70mm/year based on our model. $70mm on $2.5bn in sales? That’s a 2.8% margin business, which is simply awful for a model with relatively low operating asset turns.

The Hypothetical… So, if we’ve got 4,800 stores running at an average margin of 2.8%, do you think they’re all running at that rate? No. In fact, one of the most poorly understood parts of retail (due to GAAP reporting standards) is the massive gap that exists between a given company’s better vs. poorer performing stores. Our sense is that about a third of Payless stores are dilutive to the P&L, and upwards of half that number are cash-flow dilutive. If we assume that these stores have sales productivity that are 2/3 that of the average PSS store, and that 800 are taken out, it gets us to about $275mm in revenue lost, but $25-$30mm in EBIT gained. Our math might not be spot on, but we think it’s directionally accurate. In this situation, we think the Street would look right through a special charge – even if it’s all cash.

Most people would argue that this math is a bit extreme, as its clearly many times what management has referred to in the past as % of stores that are cash flow negative. But we think this is the new normal. A consistent low growth, high inflation environment is a game changer for evaluating the quality and consistency of a portfolio.

The Reality… This kind of math is useless if the CEO and the Board ignore it. But we think that Rubel is going to do what he has to. We’ve looked at stories like Liz Claiborne where sleepy Boards sat there and watched as shareholder’s capital eroded by the minute. This one is going to be more active. Keep in mind that Rubel is still young at 53. He’s was very successful at Cole Haan (Nike), and my opinion (he has not commented), the guy has another job left in him. But let’s be real, who will want to hire a CEO who has little Street Cred due to a rep of not making the tough decisions when it mattered? No one. He’s going to make the draconian call. Putting up inconsistently mediocre/poor results is not what he wants to be known for.

Getting rid of underperforming stores would give better transparency and consistency into the core, take up margins and returns, and would provide a better lever of stability for the core engine – which is PLG.

4. What’s It Worth? Reason To Own?

Let’s look at it a few ways…

a) Assuming it opens at $14.50, the stock is trading at 12.3x this year, and 8.7x next year. On this year, it’s probably fair. On next year, very cheap.

b) At that same price, we’re looking at 5.1x and 4.5x EBITDA for ’11 and ’12x

c) We know that stocks don’t trade on break-up values, but given the fact that numbers are a moving target, we think we should look at things in broader context. We’ve got PLG generating about $1bnm in revenue and $90mm in EBITDA. These businesses are growing in the mid-teens at a minimum, and we think that 8x EBITDA is fair multiple. That gets us to a $720mm value. The total EV for PSS, however, is $1,278. That suggests that the core business is being valued at $558mm, or 3.1x EBITDA, with an equity stub of $2.70.

In the end, numbers are coming down and the stock is cheap – but that’s not enough. 4x and 5x EBITDA is low, but why not 3-4x? There’s no reason why not while earnings risk remains. The good thing is that Rubel will make the changes he has to – even if they are severe. We’re not inclined to sell into the puke with the rest of the herd. But rather wait and see where estimates shake out for the quarter and the year, and get a sense as to whether people are negative for the right reasons.