This note was originally published at 8am on May 18, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Those who would give up essential liberty to purchase a little temporary safety deserve neither liberty nor safety.”

-Benjamin Franklin

In “The Road To Serfdom”, F.A. Hayek ends an excellent chapter titled “Security and Freedom” with that very American quote from Benjamin Franklin in 1755. Compare and contrast that thought with this quote from America’s central planning elite last night at the Harvard Club:

“Fiscal problems are so pressing that they threaten to undermine the foundations of our future economic strength… and the country’s ability to protect our national security interests.” –Tim Geithner

Notwithstanding that Geithner has been a Government Gopher since 1988 (when he joined the Treasury department), the man has since blossomed into a full-fledged storyteller of fear mongering.

Whether it’s been Geithner serving as:

- 1998-2002 - Squirrel hunter and yes-man in chief of the Robert Rubin/Larry Summers’ era of ‘we’re bigger than markets’

- 2003-2009 – President of the Big Broker Club at the Federal Reserve Bank of New York

- 2009-2011 – US Treasury Secretary who has overseen a US Dollar Index decline of -16% since he assumed office

It’s no secret that I disagree with Geithner on many scores, but I wholeheartedly agree with him on this - the political strategy of scaring the hell out of whoever he can. With his track record of contributing to this country’s fiscal problems, you should be afraid – very afraid.

How we got here and why it’s not going to change where we are going anytime soon has been compiled in my Early Looks since I decided to start writing about real-time risk management matters 3.5 years ago. Of all the fundamental conclusions I have had about Big Government Intervention, here are two that have achieved the deepest simplicity:

- It shortens economic cycles

- It amplifies market volatility

“It”, being Big Government Intervention… and the Government Gopher being the last man standing who is dumb enough to fundamentally believe that it’s the American public that’s too dumb to understand what’s going on here.

Now when you call someone “dumb”, the elitists who are concerned with titles and resumes dismiss you – but I care as much about their opinion as I do someone who says there should be no fighting in hockey.

Dumb is as dumb does – and if they want to suit someone up in a Ph.D. in Economics dress and send them on over to 111 Whitney Avenue in New Haven, CT to tell me that what Geithner has been doing since 1988 has been smart, I’ll be waiting for them.

“It” is the Big Government Intervention. “They” are the bureaucrats. We are The People.

Back to this Global Macro Grind…

Stocks, Bonds, and Commodities all reminded us yesterday of one fundamental reality that virtually the entire sell-side has had wrong for the past 5 months – GROWTH IS SLOWING. So let’s go through that:

1. Stocks – closing down for the 3rd consecutive day, the US stock market has been down for the last 3 weeks. The rest of the world’s stock markets, started going down a few weeks before that – immediately following The Bernank’s pandering to the central planning elite to remain what we have coined as being “Indefinitely Dovish” (Q2 Macro Theme).

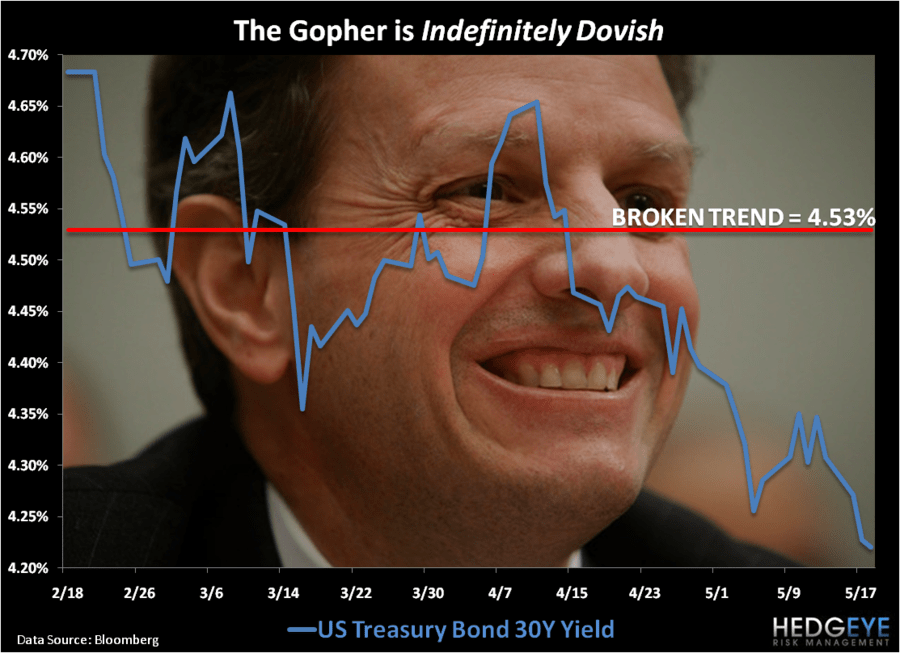

2. Bonds – US Treasury Bonds in particular have been ripping to the upside (see Chart of The Day) ever since The Bernank reminded the world that both his growth and inflation forecasts were wrong (again). Growth Slows As Inflation Accelerates. We remain long Long-term US Treasury bonds (TLT) as a way to play the “Indefinitely Dovish” Macro Theme. We’re also long a US Treasury Flattener (FLAT).

3. Commodities – May has been a mess. And a mess is what you should expect the likes of the Gopher to do to The Correlation Risk that’s imputed in daily US Dollar moves. You cannot experiment with blasting your currency to all-time lows and not assume unintended consequences. Temporary Safety, Mr. Geithner, this is not.

The good news here is that The People get it. They get the principles of individual freedom and national security. They also get that this is the only time in this country’s 235 years of economic history that some central planner has been able to politic on the platform that the markets are “national security” issues.

Geithner has spent the last 23 years of his life working on this. He’s only 49 years old. Imagine spending 47% of your life contributing to the “foundations” of America’s fiscal problems. Trust him – he knows his stuff.

Institutional money managers don’t trust the US stock market rally as much as they did while the stock market was going up – shocker. This week’s Bull/Bear Sentiment reading (Institutional Intelligence survey) saw the spread between Bulls and Bears narrow – big time.

- Bulls dropped from 51% last week to 45.6% this week

- Bears inched up to +18.5% last week to 19.6% this week

- Spread (Bulls minus Bears) narrowed from 32.5 points last week to 26 points this week

I certainly make my fair share of mistakes, but I generally don’t pose a “national security” issue to our country and I certainly don’t make a habit of chasing markets at YTD highs. That’s where we were 3 weeks ago when the Bull/Bear Spread was +38.5 points wide and I shorted US stocks.

Please don’t let America’s central planning storytellers promise you Temporary Safety in exchange for their long-term job security.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are $1472-1497, $94.91-99.67, and 1319-1336, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer