THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - May 23, 2011

With the US Dollar Index holding the Hedgeye immediate-term TRADE line of 74.41, the question now isn’t will it hold support; how high will it go from here, and how low will everything that’s correlated to it fall? As we look at today’s set up for the S&P 500, the range is 19 points or -0.92% downside to 1321 and 0.50% upside to 1340.

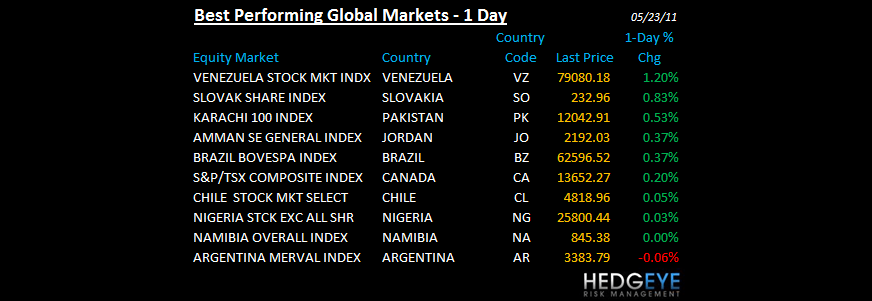

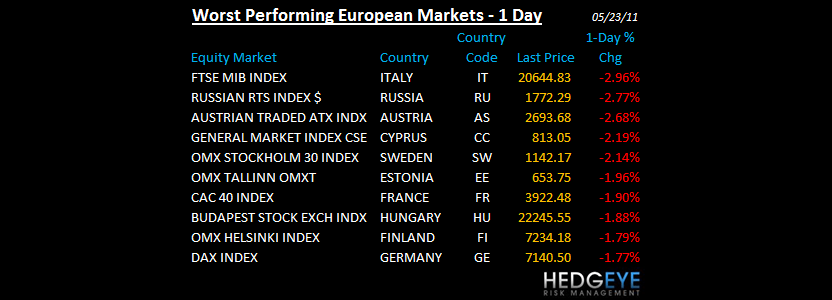

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -951 (+1503)

- VOLUME: NYSE 992.37 (+13.78%)

- VIX: 17.43 +12.31% YTD PERFORMANCE: -1.80%

- SPX PUT/CALL RATIO: 2.08 from 1.80 (+15.24%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 21.69

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 3.15 from 3.17

- YIELD CURVE: 2.60 from 2.62

MACRO DATA POINTS:

- 8:30 a.m.: Chicago Fed National Activity Index, est. 0.20, prior 0.26

- 11 a.m.: Export inspections: corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $27b 3-mo., $24b 6-mo. bills

- 4 p.m.: Crop conditions

- 8:10 p.m.: Fed’s Bullard speaks on economy in Missouri

WHAT TO WATCH:

- U.S. gasoline fell 9.24c to $3.9074/gallon over past two weeks, Lundberg Survey said; another dime drop is possible

- A congressional agreement to increase the U.S. debt limit may take until August, Paul Ryan, the Republican chairman of the U.S. House Budget Committee, said yesterday

- Dell to introduce $999 laptop 24-May - WSJ

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Oil Declines Amid Concerns Over U.S. Economic Growth, Greek Debt Default

- Speculators Cut Bets Food Prices Will Keep Rising as Supply Concern Eases

- Hedge Funds Cut Bullish Bets on Crude to Three-Month Low: Energy Markets

- Copper Slides Most in Two Weeks as Manufacturing Growth Weakens in China

- Rubber Futures in China May Extend Decline From Record: Technical Analysis

- Corn Climbs to Highest in a Month on Concern Rains to Delay U.S. Planting

- Cocoa Falls as Ivory Coast Inaugurates President Ouattara; Sugar Declines

- Gold May Advance for a Second Day on Increased Europe Debt-Crisis Concern

- Nickel Market to Return to Balance From Deficit, Norilsk’s Kuznetzov Says

- Coal Exports From U.S. Reach 20-Year High on Australia Floods, SSY Says

- Cocoa Is Poised for 13% Drop as Cargill Resumes Exports From Ivory Coast

- Mitsubishi Materials Cuts Copper Output 22% After Earthquake Halts Smelter

- Bonds Wrecked by Inflation Send Record Money Into Gold Funds: India Credit

- Bullish Wheat Bets by Hedge Funds Drop 54% as Concern About Supply Eases

CURRENCIES

EUROPEAN MARKETS

- A nasty selloff today with everything from Petro$ (Russia) to Pigs (Italy -3%) getting blasted; we're long DAX which is holding TREND (barely).

- Eurozone May Preliminary Manufacturing PMI 54.8 vs consensus 57.4 and prior 58.0; Eurozone May Preliminary Services PMI 55.4 vs consensus 56.5 and prior 56.7

- Germany May preliminary Manufacturing PMI 58.2 vs consensus 61.0 and prior 62.0; Germany May preliminary Services PMI 54.9 vs consensus 57.0 and prior 56.8

- France May preliminary Manufacturing PMI 55.0 vs consensus 57.0 and prior 57.5; France May preliminary Services PMI 62.8 vs consensus 62.0 and prior 62.9

- Greek falls behind on payments to medical suppliers - FT

ASIAN MARKETS

- A flat out ugly session with China down -2.9%, Indonesia -2.4% and India down another -1.8% to -12.3% YTD (we're short India and Thailand)

- Japan April supermarket sales (1.3%) y/y.

- China May HSBC preliminary PMI 51.1 vs April final 51.8

MIDDLE EAST

Howard Penney

Managing Director