A Very Important Probe we completed suggests that Chinese Government tightening is a statistically significant, albeit lagging, driver of VIP volume.

Our sales force likes to make fun of me for promoting my “statistical background”. Just because they made fun of people like me in high school, doesn’t mean that there isn’t some real world applications for my passion. OK, passion may be a strong word but since the average sell side analyst thinks regression means to walk backward, I think we may have a “leg” up in this category. Man, that Michael Jackson was regressive! For the youngsters out there, that’s a moonwalk reference.

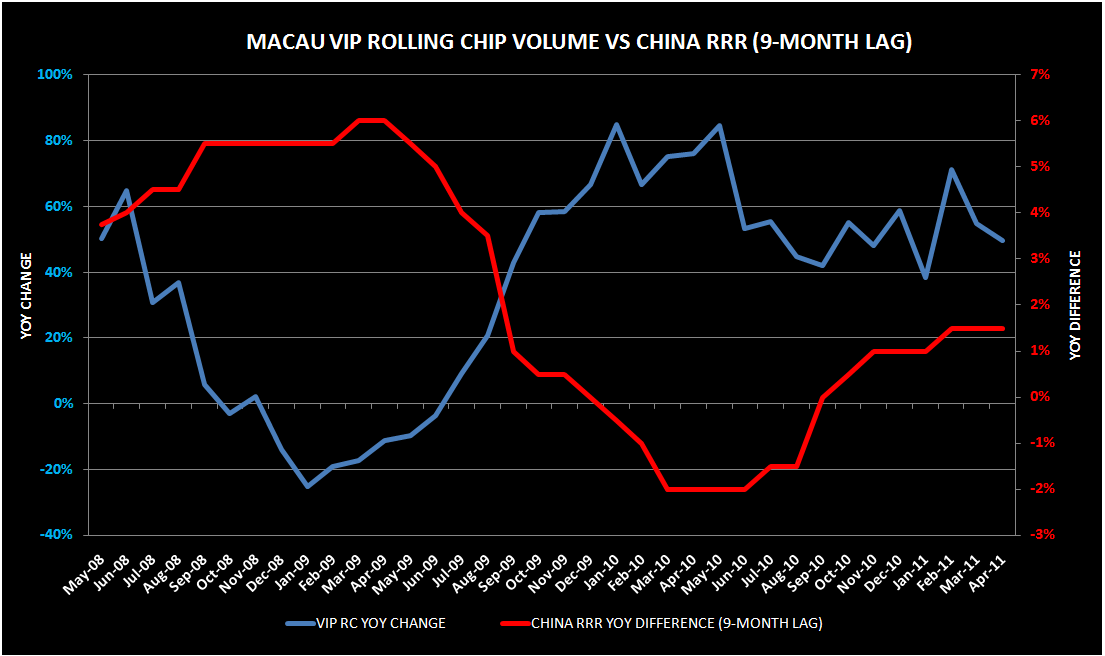

According to our regressions, VIP volume has an incredibly high correlation to the China Lending Rate and the China Reserve Requirement Ratio. The Rate and Ratio drives VIP volumes on a lag basis, peaking at 12 month and 9 month, respectively. The R Squares are a whopping 0.61 and 0.73, respectively, with T-Stats of -7.3 and -9.7. T-Stats above 2 or below -2 are generally considered statistically significant. Even though the statistical relationship between Rate and VIP Volume and Ratio and VIP Volume peak at lags of 12 and 9 months, respectively, they become significant at 6 and 3 months lag.

Theoretically, this makes a lot of sense. The junkets are fueled by liquidity and credit. A lower discount rate and lower reserve requirements drives higher liquidity and higher junket volumes, and vice versa. Many people thought that the Chinese tightening that began last fall would have had an impact on the VIP business, yet VIP kept on its explosive trajectory that it maintains today. The stocks have had great runs and not many people seem to be focused on a VIP slowdown. However, the statistical lag of up to 11 months could explain why we haven’t seen an impact from tighter money, yet.

If the historical relationship holds, we could see a slowdown this summer in VIP. If this happens, the Macau gaming stocks would be under significant pressure. We monitor Macau gaming activity on a weekly basis so hopefully we will be early on discerning a slowing trend. The companies most exposed to VIP are Wynn, MPEL, MGM Macau, Galaxy (post Galaxy Macau opening), SJM, and Sands China.

The charts below accurately depict the inverse relationship of both variables: