There’s a important callout to note between the quality of beat and raises we’re seeing in retail this morning. Let’s look at three specifically – WSM, DLTR, and ROST. Sales of the later were already reported on sales day, but both WSM and DLTR reported significantly stronger than expected top-line results, which drove SG&A leverage and earnings upside in Q1. Interestingly, despite more robust sales growth gross margins came in largely as expected – a trend that we’ve been seeing from many retailers with earnings out so far this quarter. Therein lies the callout. On the contrary, ROST reported gross margins up +60bps while growing SG&A relative to Street expectations. All three took up full-year guidance. WSM by the amount of its Q1 beat, DLTR by twice the amount of its beat, and ROST by an incremental 4% on a $0.01 beat in the quarter.

With all three companies guiding next quarter to earnings in-line or below consensus, results are becoming increasingly back-end loaded. The primary difference here is that WSM and DLTR are banking on some level of pricing to get there. ROST on the other hand has greater visibility due to its pack-a-away strategy that ensures lower costs product regardless whether or not the consumer decides to accept higher prices in the 2H. As the saying goes, a bird in the hand is worth two in the bush – for that reason we continue to like how ROST is positioned relative to most retailers heading in the 2H.

WSM: BEAT

EPS: 0.30 vs. 0.28E

Revs: +7.4%

Inv: +6%

- Beat driven by leveraging SG&A on stronger sales

- Comps +6.7% vs. 4.3%E (Guid of +3-5%)

- Increased FY Guidance by amount of beat

DLTR: BEAT

EPS: 0.82 vs. 0.75E

Revs: +14%

Inv: +9%

- Increasing FY guidance by $0.14 vs. $0.07 beat > taking up FY

- Took up low end of revs outlook

- Increased EPS range implying stronger profitability

- Reaffirming FY comps up LSD-MSD

- Comps +7.1% vs. +4.9%E

- Also beat by leveraging SG&A on stronger sales

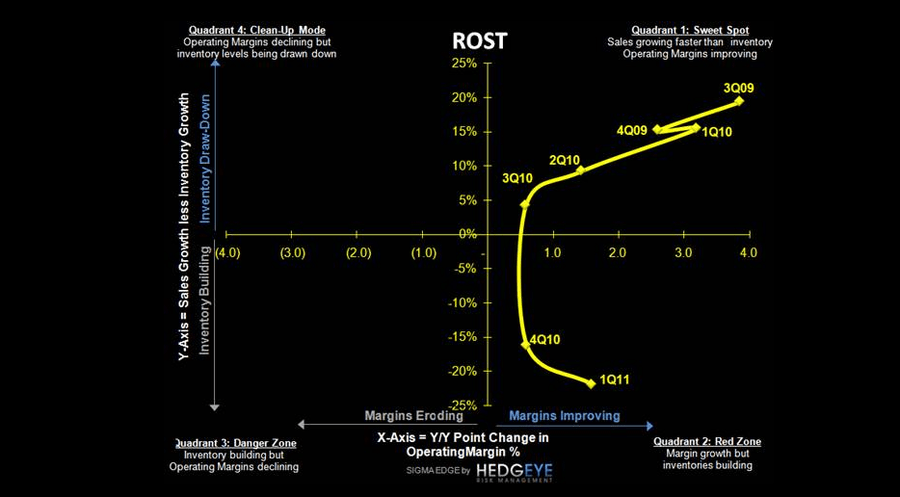

ROST: BEAT

EPS: $1.48 vs. $1.47E

- Guiding to Q2 below Street

- Taking FY outlook up $0.20-$0.25 to $5.16-$5.31

- GM expansion driven by pack-a-way driving results and earnings upside

Casey Flavin

Director