“As always, if you listen to my advice, be prepared to be early!”

-Jeremy Grantham, May 2011

If you have not yet read Jeremy Grantham’s most recent GMO Quarterly Letter titled “Time To Be Serious (and probably too early) Once Again”, I highly recommend it. He’s been managing Global Macro risk for a long enough time to know that the best lessons in this business are learned the hard way.

Managing interconnected Global Macro risk is hard. So is keeping up with the required risk management reading that’s readily available to you. If you read too much groupthink, you’ll miss the deep simplicity of Mr. Macro Market’s signals. If you read too little history, you’ll miss the context by which the patterns of human behavior rhyme. Your reading needs to be focused and timely.

For me, it’s taken almost 13 years to realize that I read too much garbage and too little history. So, in the last 3 years I’ve worked on changing that. The plan on this front is always that the plan is going to change, but currently my reading process falls into two buckets:

- My pile

- My books

My pile, as my teammate of many years Tanya Waite can attest, is perpetually mounting. From my desk, to my bag, to airplane pockets around the world, my pile is my Princeton hockey player. I will fight it until I knock it down. My pile is a series of print outs (Grantham, Gross, etc.), white papers, and whatever else my team sends me that refutes or augments my current thinking.

My books, like my emotional baggage, are always with me – that’s why you’ll see me cite books in the sequence that I am reading them. I just finished reviewing “The Road To Serfdom” and “Undaunted Courage.” My challenge is to read at least 1 book every 10 days. On the plane to Denver last night, I was reading “The World In 2050” – more on that book and being long Northern Rim Countries (NORCs) in the coming weeks.

Back to Grantham’s problem of Being Early…

- Being Early to work isn’t a problem – it’s cool

- Being Early to mentally prepare for a game is better than being late

- Being Early in our institutionalized world of chasing short-term performance is also called being wrong

That’s Wall Street. In evaluating our professional competence, our process and principles can always be trumped by our short-term P&L. Are you wrong today because you are about to be right? Or are you right today because you are about to blow up?

These are fair questions. Clients shouldn’t have to pay for my pile or performance problems. We are overpaid to over-deliver over long periods of time. As Risk Managers, we are tasked with explaining to our clients what it is that we are doing and why.

As Grantham points out in his Quarterly letter, “we often arrive at the winning post with good long-term results and less absolute volatility than most, but not necessarily with the same clients that we started out with.” Isn’t that the truth? Your clients need to know your duration too.

Back to the Global Macro Morning Grind…

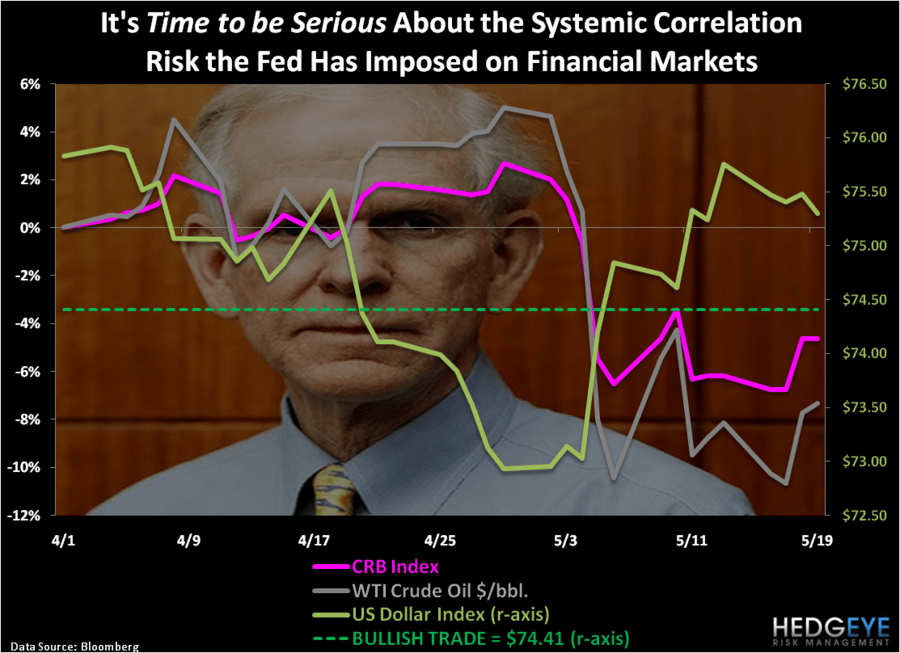

No matter where you go this morning, there it is – The Correlation Risk to the US Dollar Index. For the week-to-date, the US Dollar Index is down a measly -0.65%, but look at the pop you are getting in the big stuff that’s priced in those Burning Bucks:

- CRB Commodities Index = +1.7% week-to-date

- WTI Crude Oil = +1.3% week-to-date

- SP500 = +0.22% week-to-date

Ok, maybe a 22 basis point move in US Equities isn’t the kind of pop that would get you all fired up, but maybe that’s the point. Maybe people are starting to get the math. Since the immediate-term inverse correlation between the SP500 and the USD is -0.84% (extremely high), maybe people are starting to consider the other side of the immediate-term TRADE.

What if the US Dollar stops going down from here?

The answer to that question is a trivial one. US stocks and commodities corrected -3% and -9%, respectively, in the last 2 weeks of a USD rally. While a strong dollar is great for this country, it’s awful for stock and commodity markets in the immediate-term. Yes, Mr. Bernanke, the country and the markets are 2 very different things.

This is where all of my reading runs parallel with my risk management signals – and yes, there is also a huge difference between the research embedded in your reading and how you manage risk in your portfolio. Every once in a while a risk management signal jumps out at me that’s impossible to ignore. Currently that signal is an immediate-term TRADE breakout in the US Dollar Index.

If you were only to allow me one live market quote to manage all Global Macro risk on for the next 3 weeks, I’d take the USD Index. The line in the sand is currently $74.41. That’s my TRADE line – and my risk management process is to respect it until correlation scores tell me not too.

If $74.41 holds support, I sell stocks and commodities (that’s why I have sold all my Oil and Gold in the last 2 weeks). If $74.41 breaks, I’ll be forced to go back to speculating on what The Inflation trade can do.

Being forced to do things isn’t cool. But, like Grantham, I have learned to take a measurable level of risk to speculate in these correlation trades. On page 2 of his Quarterly Letter, Part 2 – “Time To Be Serious” – May 2011, this is how the self-effacing Grantham summed up the same:

“As readers know, driven by my increasing dislike for being early by such substantial margins, I have been experimenting recently with going with the flow. In defense of this improper behavior, rest assured that it was motivated not by chasing momentum, but by my growing recognition of the immense power – sometimes the thoroughly dangerous power – of the Fed.”

Being Early doesn’t work until it does.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer