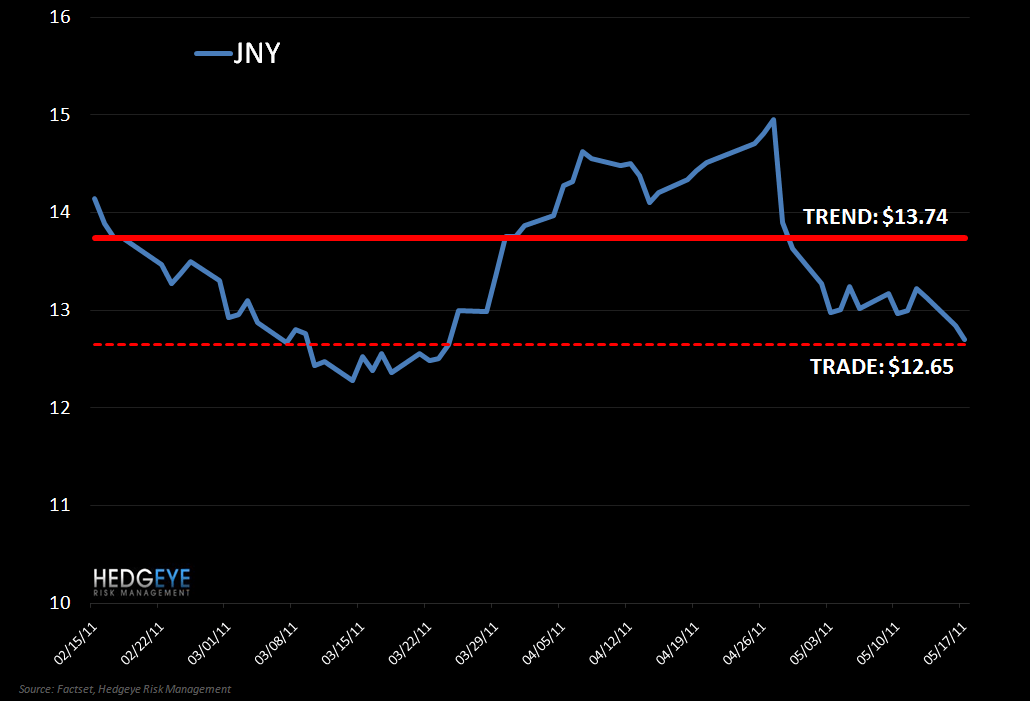

KM covering - Immediate-term TRADE oversold. McGough remains bearish on Jones Group for the intermediate term TREND. Fundamentally, we still don’t think that this company will earn over a buck ever again without major internal change.

KM covering - Immediate-term TRADE oversold. McGough remains bearish on Jones Group for the intermediate term TREND. Fundamentally, we still don’t think that this company will earn over a buck ever again without major internal change.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.