Slowing growth is the story. Hold-aided Genting increasing its market share lead.

The Singapore gaming market generated US$4.9BN (S$6.5BN) in gross gaming revenues over the 4 trailing quarters. Over the same period, Macau casinos took home US$25.7BN and Las Vegas casinos reported US$5.8BN in gaming revenues. On an EBITDA basis, S’pore market cashed in S$3.0BN (US$2.3BN). Relative to 4Q, S’pore 1Q revenues jumped almost 10% to a new quarterly record of S$1.9BN, the highest QoQ growth rate among the three markets. However, Rolling Chip (RC) hold was high (3.3% vs a TTM rate of 3%) during the quarter which contributed virtually all of the QoQ growth.

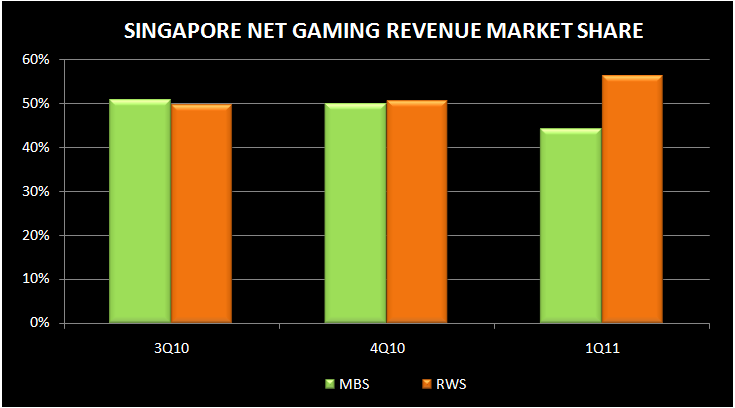

In terms of market share, Genting came out on top again in Q1. As the charts below show, Genting increased its lead over LVS in EBITDA and revenue share since Q4 due mainly to high hold. However, LVS regained 10 percentage points in VIP RC share after Genting reported an 18.5% sequential drop in VIP RC. The company blames high hold for some of the sequential drop explaining that players wager less when they are losing.

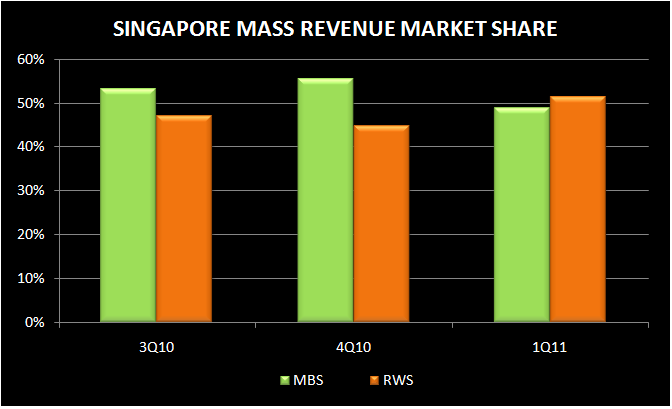

So where do we go from here? Expectations have been so high for the S’pore market in 2011 that modest growth (5-10%) for the rest of the year may not be enough to satisfy the Bulls. The 5% sequential drop in market VIP RC in Q1 is concerning (comparatively, Macau has not seen a QoQ drop in VIP RC since Q4 2008), and the junket licensing catalyst may not happen any time soon. Mass has been relatively flat since the sequential jump in 3Q 2010. Slots have exhibited decent sequential growth but that growth rate has slowed substantially. Of course, Golden Week may reverse these trends temporarily, but we would not be surprised to see some disappointed bulls expecting Macau type growth.