“The more we try to provide full security by interfering with the market system, the greater the insecurity becomes.”

-F.A. Hayek

I have been focusing my quotes for the last few weeks on the most pertinent parts of Hayek’s “The Road To Serfdom” in hopes of someone in Washington finding it within themselves to stop doing more of what got us into this mess.

The Audacity of Hope, unfortunately, is not a Global Macro risk management process. Neither is John Boehner telling Barack Obama, “let’s lock arms and jump out of the boat together”…

Boehner was talking about raising the US Debt Ceiling limit (which the US is technically in violation of today). All US Constitutional “technicalities” aside, this country hasn’t had much of a memory when it comes to the original provision to let the US Treasury print debt in 1917 (in order to finance war). When in doubt, fear monger the citizenry into believing centrally planned security is the only way out.

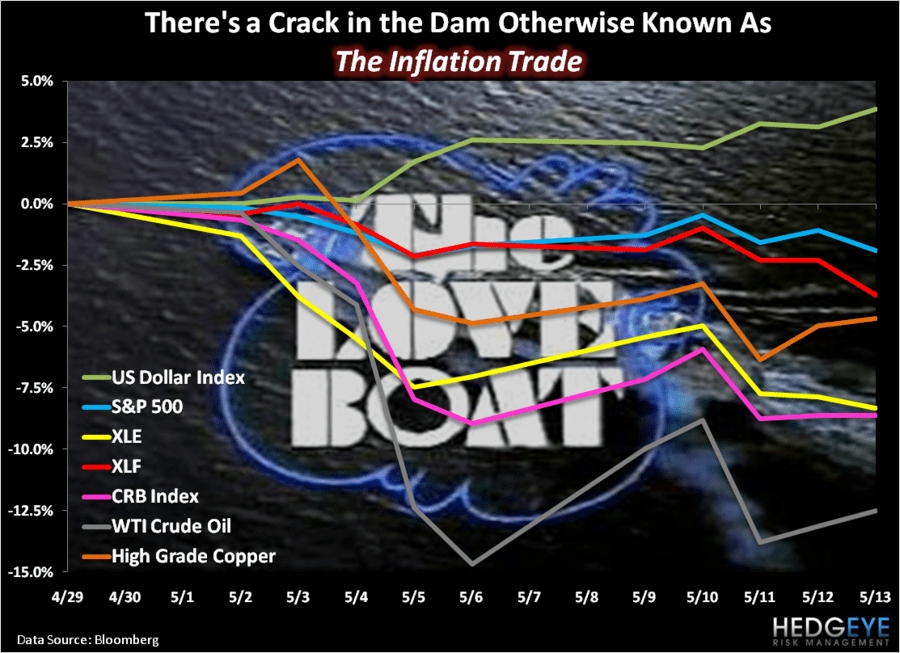

For the week, with the US Dollar Index closing up +1.1% at $75.78:

- The US Dollar Index has been up for 2 consecutive weeks for a cumulative recovery of +3.8% from its YTD lows.

- The US Dollar Index has been down for 14 of the last 20 weeks and remains bearish on an intermediate-term TREND basis.

- The US Dollar Index is down -14.4% since Obama and Geithner took over in early 2009.

From a Correlation Risk perspective, here’s the 2-week cumulative declines in stocks and commodities priced in US Dollars:

- US Stocks (SP500) = DOWN -1.9%

- US Energy Stocks (XLE) = DOWN -8.3%

- US Financial Stocks (XLF) = DOWN -3.7%

- CRB Commodities Index = DOWN -8.6%

- West Texas Crude Oil = DOWN -12.5%

- Copper = DOWN -4.6%

So, if you didn’t know that the Globally Interconnected Marketplace is highly correlated to a US Dollar UP move, now you know…

Those who interfere with the free-market system, experimenting with Fiat Fool policies that take the US Dollar to all-time lows, didn’t get The Correlation Risk they were imposing on stocks and commodities in Q208 - and they most certainly don’t get it now. The game within the hedge fund game is now called Gaming Policy – and it’s volatile.

If you disagree with me that The Bernank perpetuates The Price Volatility by promising the world to remain “Indefinitely Dovish” (Q2 Hedgeye Macro Theme), the market disagrees with you. Since pandering to the political wind at the latest FOMC presser, the VIX (volatility index) is up +15.8%.

Global Growth Slows As Inflation Accelerates – I think the world gets that now… but do the world’s Risk Managers know how to deal with the most levered long trade in hedge fund history as it unwinds?

We call this “Deflating The Inflation” (Q2 Hedgeye Macro Theme) – US Dollar UP is the only way out of creating the highest levels of US-style Stagflation since the 1970s.

Two important points on stagflation:

- Real-time inflation (commodities, rents, education, etc) is reported real-time…

- US Government reported “inflation” is reported on a lag

Last week’s US Consumer Price Index (CPI) was +3.2% for the month of April – whereas Deflating The Inflation has occurred in May. This is where it gets tricky for the stagflation bulls who don’t think they’ll ever see a 600 basis point drop in the SP500’s PE multiple (like we saw in the 1970s when reported inflation broke out above reported (lagging) US GDP growth). Sound familiar? US GDP for Q1 was +1.8%.

Two points on US Growth and Inflation:

- Growth Slowing (joblessness) is going to remain throughout the summer months (the 4-week rolling average of weekly jobless claims just hit a new YTD high last week of 437,000).

- Reported Inflation is going to remain elevated because rents continue to climb (as US Housing double dips) and The Inflation “compares” get a lot easier through August (putting an upward bias on reported y/y CPI).

So what do you do with that?

Last week I moved as aggressively to Cash in the Hedgeye Asset Allocation Model as I have since mid-February. Here’s where our allocations stand as of this morning:

- Cash = 52% (up from 43% last week and 34% two weeks ago)

- International Currencies = 18% (Chinese Yuan – CYB)

- Fixed Income = 15% (US Treasury Flattener and Long Term Treasuries – FLAT and TLT)

- Commodities = 6% (Gold – GLD)

- US Equities = 6% (Tech – XLK)

- International Equities = 3% (Germany – EWG)

Mr. Macro Market does not owe any of us a return. When The Correlation Risk hinges on insecure policy like it does today, sometimes the most secure move for my own money is to simply get out of the way.

The problem right here and now is that everyone is still long The Inflation because The Dare was to chase The Yield – so we’ll need to wait and watch for entry points (capitulation maybe closer to $93 oil) before we take up our invested position again.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1, $93.18-100.58, and $1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer