TODAY’S S&P 500 SET-UP - May 16, 2011

The USD is now breaking out above the Hedgeye immediate-term TRADE line of $74.55 this morning. In terms of The Correlation Risk, this only enhances the probability that we’re going to see oil test $93 and a continued unwind of The Inflation trade. The entire commodity complex (CRB) is now bearish TRADE and TREND, confirming what Copper has been signaling since mid-Feb when we started confirming that Global Growth Slows As Inflation Accelerates. As we look at today’s set up for the S&P 500, the range is 14 points or -0.51% downside to 1331 and 0.54% upside to 1345.

SECTOR AND GLOBAL PERFORMANCE

By week’s end the US Equity market saw one more sector (Industrials – XLI ) break our immediate-term TRADE line. That makes 4 of 9 Sectors bearish on our immediate-term TRADE duration (XLF, XLE, XLB, and XLI) and 3 of those 4 (XLF, XLB, and XLE) are also confirmed by bearish intermediate-term TREND breakdowns (which we flagged in a risk management note earlier in the week).

Tech (XLK) and Healthcare (XLV) remain our two favorite sectors on the long side (in that order of preference from last price).

Beta is starting to underperform as expectations for Growth Slowing get baked in.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1319 (-2118)

- VOLUME: NYSE 898.43 (-5.57%)

- VIX: 17.07 +6.49% YTD PERFORMANCE: -3.83%

- SPX PUT/CALL RATIO: 1.81 from 1.80 (+0.40%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 24.02

- 3-MONTH T-BILL YIELD: 0.03% +0.01%

- 10-Year: 3.18 from 3.22

- YIELD CURVE: 2.61from 2.65

MACRO DATA POINTS:

- 8:30 a.m.: Empire Manufacturing, est. 19.70, prior 21.70

- 8:30 a.m.: NOPA oil, soybean data

- 9 a.m.: Bernanke speaks on innovation/research in Washington

- 9 a.m.: Total net, net long-term TIC flows

- 10 a.m.: NAHB housing market index, est. 17, prior 16

- 11 a.m.: Export inspections, corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $27b 3-mo. bills, $24b, 6-mos. Bills

- 4 p.m.: Crop progress, grains

WHAT TO WATCH:

- State Street wants to expand by acquisition outside the US - FT

- Netflix announces strategic multi-year agreement with Miramax; terms undisclosed

- Wynn Resorts CEO Steve Wynn says company has not been investigated for violating Foreign Corrupt Practices Act - WSJ

- Japan earthquake came at unfortunate time for car dealers like AutoNation - WSJ

- Greece will plead for boost in its $155b bailout from European govts. in IMF talks clouded by arrest of Strauss- Kahn

- Primedia, majority-owned by KKR, may announce deal to sell itself to TPG Capital as soon as today

- A group of Canada’s biggest banks, pension funds made $3.7b bid for TMX Group, topping offer from London Stock Exchange

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Speculators Cut Bets on Higher Commodity Prices by 15% in Week to May 10

- China Said to Sell Soybeans to Cool Inflation at Fastest Pace Since 2008

- Goldman ‘Most Constructive’ on Copper, Raises Outlook For Aluminum, Nickel

- Steel Consumption May Improve This Year on Economic Recovery, Stemcor Says

- Gold May Advance as EU Finance Mininsters Discuss Greece’s Financing Needs

- Copper Drops in London Trading as Speculators Cut Holdings: LME Preview

- Coffee Falls as Vietnam’s Production May Increase; Cocoa Prices Advance

- Crude Declines on Concern Over Greek Bailout Talks, U.S. Economic Growth

- Corn Advances for Third Day as Wet Weather Delays Planting in U.S. Midwest

- Hedge Fund Gas Bets Tumble 26% in Commodity ‘Game Changer’: Energy Markets

- Europe Commodity Day Ahead: Gold-Coin Sales at a High Show Rally Not Over

- Sumitomo Metal, Sumitomo Corp to Invest $724 Million in Chile Copper Mine

- Aluminum Stockpiles in Japan Advance 8.9% After Quake Disrupts Shipments

CURRENCIES

EUROPEAN MARKETS

- European market are weak across the board

- Eurozone April final CPI +2.8% y/y vs consensus +2.8% and prior +2.8%; Eurozone April final CPI +0.6% m/m vs consensus +0.6% and prior +1.4%

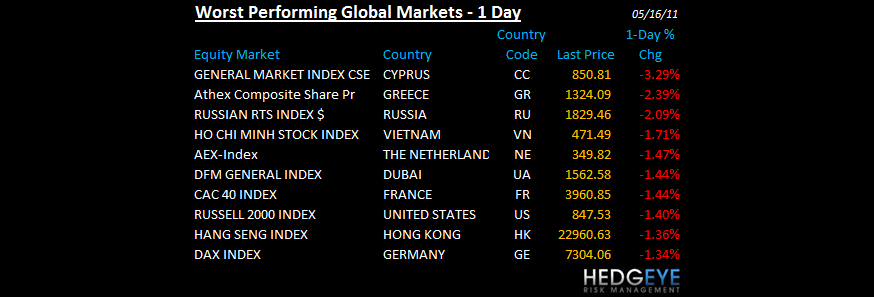

- Russia breaking intermediate term TREND line as Spain did last week

ASIAN MARKETS

- Asian markets were weak lead by Vietnam and Hong Kong

- India down another -1% to -10.6% YTD (we're short)

- Japan March core machinery orders +2.9% m/m vs consensus (9.9%). April domestic CGPI +2.5% y/y. April-June core machinery orders forecast +10%. April consumer confidence 33.1 vs 38.6 in March.

- Thailand was closed for a special holiday and will reopen 18-May.

MIDDLE EAST

Howard Penney

Managing Director