Foot Locker reports Q1 earnings next Thursday after the close, followed by a conference call on Friday morning. We expect a positive 1Q result with our model coming in at $0.46 ahead of the Street at $0.44. The key differential in our forecast is a +6.5% same store sales increase (vs. +5%E) with gross margins slightly ahead of full-year expectations offset in part by higher SG&A. Our forecast for the year is $1.42 in EPS above the Street’s $1.34E.

Is it super cheap at 6.2x EBITDA? No. But we still think that after the call, this will slowly but surely convert some of the perennial perma-FL-haters’ into viewing this as a story that can manage double digit EPS growth and can buy back 30% of the float within 3-years. That’s not half bad… While not our favorite stock, it is one we think should keep working in 2H.

Here’s a look at some of the key modeling considerations for the quarter:

Sales: +5.8% on a +6.5% comp - This represents a 2-year acceleration of about 300bps. A few factors to bear in mind…

a) First and foremost, this is a period during which the ‘new’ management team should really start to execute. We’ve had the closure of poor performing stores, and a big merchandise push by the likes of Nike. While Toning, however, is a concern vs. last year the trends at retail from a POS perspective have been encouraging. Higher sales and ASPs at a point where the space needed to ‘comp the comp.’

b) In looking at the results of the performance footwear categories to which FL is over-indexed (i.e. Running, Basketball, Casual Athletic, and Cross-Training), 1Q results look encouraging up +10% on +5% growth last year.

c) In addition, athletic apparel has been strong up +9% in Q1. With the category growing as a percent of sales, we expect it be an additional driver and likely recipient of another positive management callout similar to Q4.

d) Also, keep in mind that FX should be a factor here. About 19% of store count, 17% of square footage, and 15% of sales originate outside the US. Given the dollar having tanked vs. last year, it nets out to be around 1-1.5% FX benefit on the top line.

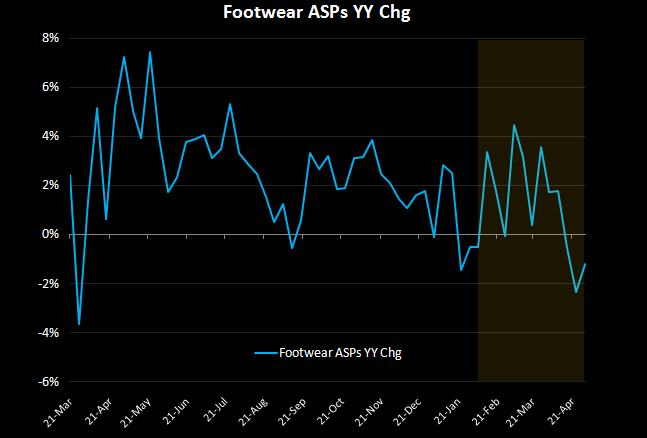

e) According to our blended comp chart, sales are up +4.3%. As you may recall, this indicator has consistently tracked sales within a +/- 2-3% range and has been low by -2.2% and -3.8% respectively over the last two quarters – a +6.5% comp suggests its low by -2.2% in Q1. It’s important to note the change at NPD as well since Q4 with the weekly data now including the department and family channels, which understates the performance in athletic specialty. In fact, according to the monthly data set (see chart below) athletic specialty (+6.9%) outperformed both dept (-6%) and family (-4.2%) channels significantly through the first two months of the quarter suggesting further upside to the +4.3% blended comp providing added cushion and confidence in our +6.5% comp estimate.

GM: +85bp

Even though ASPs have been hanging in there, we cannot ignore the interim hit at Nike last quarter and in its May quarter. That pain will be shared. But the reality is that with a +6.5% comp, the occupancy leverage combined with better merchandise margins here is meaningful. We expect the later to be the primary driver of gross margins in the quarter driven primarily by further improvements in mix and more modest promotional activity due to both higher ASPs and inventories that remain in check and continue to grow at a rate below management’s target of 50% of sales.

SG&A: +2%

Management suggested that Q1 would come in below full-year SG&A growth expectations of +1-2%, Given the strength in the dollar, we’ll assume the higher end of the range.