Notable news items and price action from the past twenty-four hours as well as our fundamental view on select names.

- SBUX was initiated “Market Perform” at Wells Fargo.

- SBUX has stopped buying coffee as it waits for price to pull back from a 34-year high, according to John Culver, President of Starbucks International. Culver was quoted in Swiss newspaper Tages-Anzeiger as saying, “these prices are not based on facts given there is no supply problem. Speculators are at work here”.

- Coffee production in Columbia fell 19% to 523,000 bags in April, year-over-year, after storms last year hampered plants from flowering. Output was 647,000 bags in April 2010.

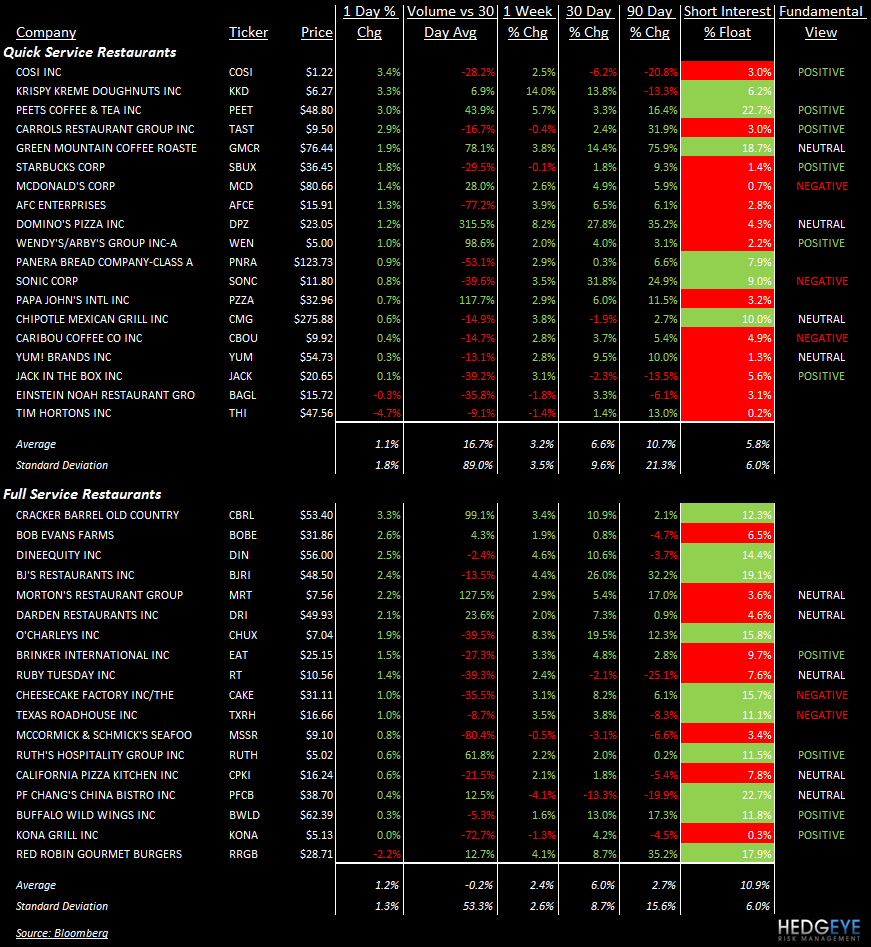

- KKD, PEET, GMCR, MCD, DPZ and WEN all made significant gains on accelerating volume.

- CBRL, BOBE, MRT, and DRI were the gainers on the casual dining side that traded with high volume yesterday.

- YUM has offered to pay HK$6.50 per share for most of the shares it does not already own of Little Sheep, the Chinese hot pot restaurant operator.

- Burger King has struggled of late, with first-quarter same-store sales falling 6 percent in the United States and Canada.

- OSI Restaurants reported Q1 comps. Comps by concept (systemwide):

- Outback Steakhouse +4.1%

- Carrabba’s Italian Grill +3.9%

- Bonefish Grill +9.6%

- Fleming’s Prime Steakhouse and Wine Bar +11.4%

- COSI reported a loss of $0.04 per share for 1Q and company same-store sales of +3%.

Howard Penney

Managing Director