This note was originally published at 8am on May 10, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Who plans whom, who directs and dominates whom…?”

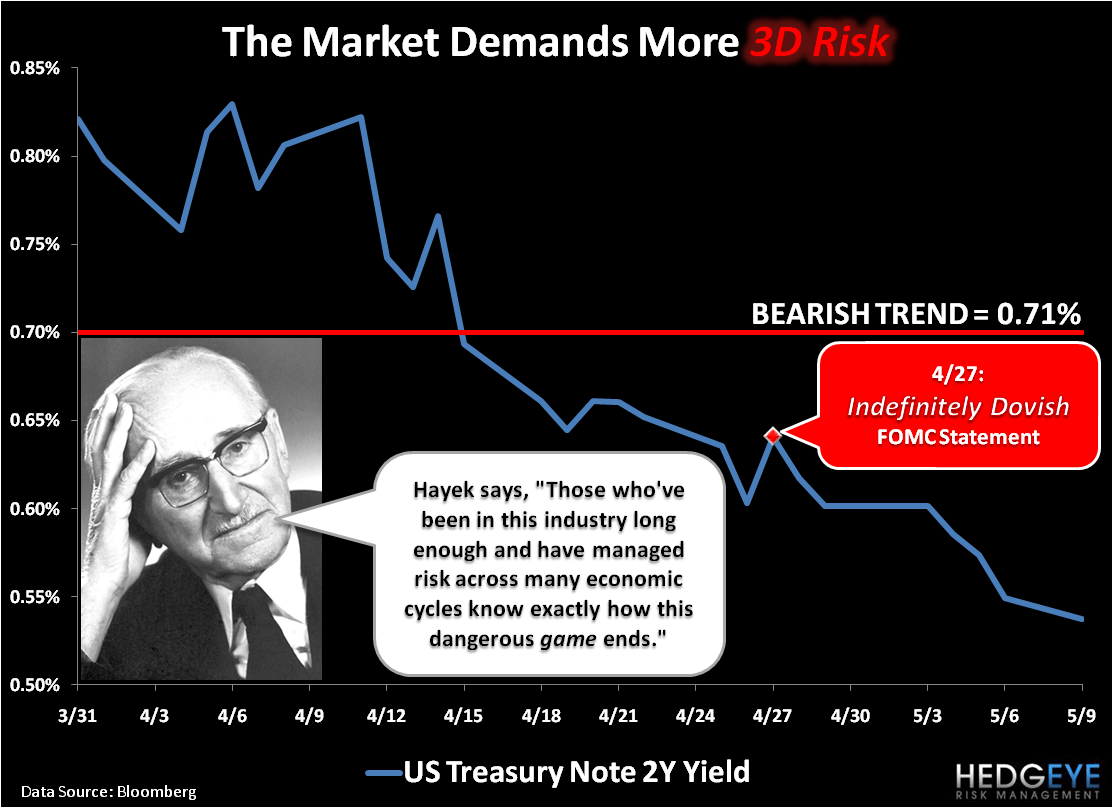

-F.A. Hayek

As long as our central planning overlords keep coming up with new plans for our said “free markets” (regulating oil margin requirements, compromising a Constitutional debt-ceiling debate for political favors, etc.), I guess I’ll just keep rolling through a full frontal review of their Keynesian dogma.

This isn’t to say that the Austrian and Chaos Theory schools of math & economics don’t have their faults. All schools do. It is simply a reminder that all independent research starts and ends with finding the right answers. Sometimes those answers are different, depending on who you are, and who dominates you…

Being directed and dominated by bureaucrats isn’t cool. That’s why hard core American patriots are so upset. If you live in a different country where socialist planning isn’t new, you’ve probably been bitter for a while now and this email is likely regulated away from your inbox too.

The aforementioned quote comes from a chapter Hayek wrote in 1944 titled “Who, Whom?” He borrowed this metaphor from Lenin in order to ask some very basic questions about individual freedoms and liberties: “Who, whom? - during the early years of Soviet rule the byword in which the people summed up the universal problem of a socialist society.” (“The Road To Serfdom”, page 139)

Something to think about while you watch The Price Volatility trade in your increasingly planned markets this morning…

Evidently, markets that are rigged, planned, or regulated inspire lower and lower trading volumes and/or higher and higher levels of volatility. If this is what the end-game for the Keynesian Kingdom is supposed to look like, no one should be surprised.

Whether or not I like it, I have to deal with managing risk around it this morning. I know it won’t end well, but that’s not what I’ll get paid for saying today.

Sadly, what we are all getting paid to do is chase short-term returns. The Bernank perpetuates this performance pressure by marking the short-term “risk free” rate to model (or the ZERO bound) and, as a result, this gargantuan experiment of starving savers of returns imputes 3D Risk (3 D’s) into markets:

- The Dare – zero % rates dare you to chase yield across asset classes where you can justify it

- The Delay – zero % short-term financing for banks delays the financial restructurings that free market prices would impose

- The Disguise – zero % expectations disguise the interconnected risks associated with carry trading, correlation risk, etc

Bloomberg data quantified The Dare and The Delay in their “Weekly Commitments of Traders Report” yesterday with the following data point on short-term US Treasury speculation:

“Non-commercial accounts purchased 48,460 contracts on two-year Treasury notes during the latest reporting period. The long position of 235,621 contracts is 3.4 standard deviations above its one-year average.”

In other words, never mind who is planning whom for a minute and realize that the entire Institutional Investor community is getting paid to beg The Bernank to keep the status quo on remaining what we’ve labeled as being “Indefinitely Dovish” (Q2 Macro Theme).

Again, I may not like it – but I do have to deal with it. So here’s the read-through so far this morning, alongside our positioning across asset classes (which you can see daily in the Hedgeye Portfolio at the bottom of the Early Look):

Currencies

- US Dollar = down for the 15th week out of the last 20 (we’re short)

- Euro = flat for the week, holding immediate-term TRADE line support of $1.43 (no position)

- Chinese Yuan = hitting new all-time highs this morning at $6.49 (we’re long)

Equities

- US Equities = up for the 2nd day out of the last 6 making lower-highs on almost record low volume (we’re short SPY)

- US Tech = up in the pre-market on the heels of big M&A (MSFT for Skype) – we’re long Tech (XLK)

- Chinese Equities = up for the 5th day in the last 7 after an outstanding trade balance report (we’re long)

- Indian Equities = down again overnight to -9.8% YTD as USD debauchery driven inflation is forcing rate hikes (we’re short)

- Germany Equities = up a full percent this morning to +8.3%, outperforming SP500 like they did last year (we’re long)

- Greek Equities = up a full 2 percent this morning after crashing in the last few weeks (down -19.7% since February 18th)

Commodities

- WTI Crude Oil = down small this morning on margin whispering, and up +4.1% for the week (we’re long)

- Gold = up again this morning, recovering from its -4.2% down week, up +1.8% week-to-date (we’re long)

- Copper = up over +2% for the week-to-date but still bearish/broken on both our TRADE and TREND durations (no position)

So what do I plan on doing with all of these moves and positions? Who is planning to plan moves on me next?

I really don’t know.

And I guess that’s probably a good thing to admit, given that US stock centric cheerleaders of “Dow 13,000” from early 2008 are still telling you with 100% conviction that they know exactly where this baby is going next.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1488-$1522, $98.63-$109.11, and 1334-1351, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer