THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - May 12, 2011

In our Q2 Global Macro Theme slide deck, we call this stage of asset prices (relative to USD) “Deflating The Inflation” – send an email to if you need those slides and scenario analysis (we also have the conference call replay on the Hedgeye Portal).

Obviously with last week’s hyper correlation risk (USD +2.6% week = Oil down -14.7%, CRB -8.9% on the week, etc), yesterday’s unwind was proactively predictable. USD UP = CRB index down -2.9% on the day – and oil hammered (we made a call to sell Oil on Tuesday).

The Hedgeye models are registering immediate-term TRADE (3 weeks or less) downside in WTI Crude Oil this morning of $93.33/barrel. That’s eye opening – and the other side of the biggest net long position in hedge fund history should be. The only “commodity” we are long here is gold. The Immediate-term TRADE ranges to watch on the way up to USD immediate-term TRADE overbought line = 75.79:

The reason why the Hedgeye models have USD and Euro “neutral” in the immediate-term is that the big moves in both are now in the rear view mirror! USD is bullish TRADE, bearish TREND whereas Euro is bearish TRADE (resist = 1.44), bullish TREND (support = 1.40). As we look at today’s set up for the S&P 500, the range is 18 points or -0.83% downside to 1331 and 0.52% upside to 1349.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1431 (-3326)

- VOLUME: NYSE 975.04 (+16.76%)

- VIX: 16.95 +6.54% YTD PERFORMANCE: -4.51%

- SPX PUT/CALL RATIO: 2.20 from 1.54 (+43.06%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 24.70

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 3.19 from 3.23

- YIELD CURVE: 2.62 from 2.60

MACRO DATA POINTS:

- 8:30 a.m.: Fed’s Plosser speaks in Aventura, Florida

- 8:30 a.m.: Initial jobless claims, est. 430k, prior 474k

- 8:30 a.m.: Net export sales (commods)

- 8:30 a.m.: Producer price index, est 0.6% M/m, prior 0.7%

- 8:30 a.m.: Retail sales, est. 0.6%, prior 0.4%

- 9:30 a.m.: Senate Banking committee votes on Fed nominee Diamond; Fed Chairman Ben Bernanke then testifies in oversight hearing on Dodd-Frank law

- 9:45 a.m.: Bloomberg consumer comfort, est. (-45.9), prior (-46.2)

- 10 a.m.: Business inventories, est. 0.9%, prior 0.5%

- 10:30 a.m.: EIA natural gas storage, est. 71, prior 72

- 1 p.m.: U.S. to sell $16b 30-yr bonds

- 8 p.m.: Bernanke gives brief remarks at award ceremony in Wash.

WHAT TO WATCH:

- AT&T to cut lots of jobs if its purchase of T-Mobile USA is approved - NY Post

- China raises reserve requirement ratios for banks by 50 bp to 21%; The reserve requirement ratio increase is effective 18-May

- EPS season ending ugly with the CSCO quarter - Soon it will be MACRO time

- Reserve-rich Asian countries still see US Treasuries as the safest bet - Reuters

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Commodities Drop for Second Day as Higher Rates May Curb Economic Growth

- Crude Oil Declines After IEA Cuts 2011 Global Demand Forecast on Prices

- Copper Slides to a Five-Month Low as Tightening Cuts Into Demand in China

- Gold, Silver Decline as Dollar Gain Reduces Alternative Investment Demand

- Cocoa Falls as Ivory Coast Exports Add to Supply; Arabica Coffee Declines

- Investors Shifting to Cash From Commodities as Outlook Dims in Global Poll

- China’s Sugar Imports May Be 28% More Than Forecast by U.S., Olam Says

- Corn, Wheat Extend Decline as Crude Oil Trims Gains, Dollar Strengthens

- West African Oil’s Two-Year High Threatens Growth in India: Energy Markets

- Shanghai Exchange May Widen Silver Trading Band Tomorrow After Price Drop

- Food Prices May Extend Advance, Adding to Inflationary Pressure, FAO Says

- Japan Orders Slaughter of All Cattle Around Fukushima Nuclear-Power Planth

CURRENCIES

EUROPEAN MARKETS

- EuroZone Mar Industrial production +5.3% vs consensus +6.2% and prior revised +7.7% from +7.3%; EuroZone mar Industrial Production (0.2%) m/m vs consensus +0.3% and prior revised +0.6% from +0.4%

- UK March Manufacturing output +2.7% y/y vs consensus +2.8% and prior +4.9%; UK March Manufacturing output +0.2% m/m vs consensus +0.3% and prior +0.0%

- UK Mar Industrial output y/y +0.7% y/y vs consensus +1.1% and prior +2.4%; UK Mar Industrial output m/m +0.3% y/y vs consensus +0.8% and prior (1.2%)

- France Apr CPI +2.2% y/y vs consensus +2.2% and prior +2.2%; France Apr CPI +0.4% m/m vs consensus +0.4% and prior +0.9%

- Markets are weal across the board; Oil markets are leading the way down.

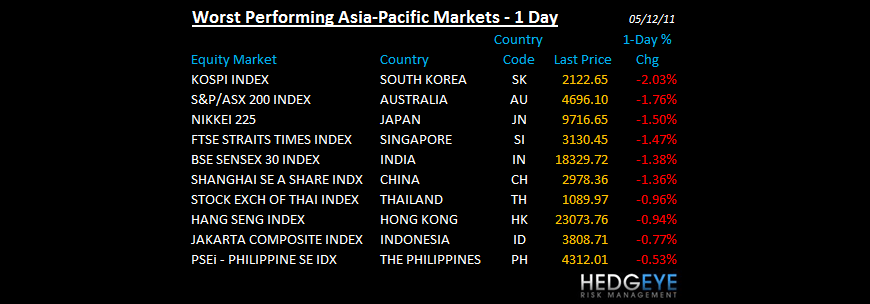

ASIAN MARKETS

- Asian market were weak across the board

- Japan April M3 +2.1% y/y. March trade surplus (77.9%) y/y. March current account surplus (34.3%) y/y to ¥1.679T vs consensus ¥1.731T.

- Australia April employment (22,100) m/m vs consensus +17,000; April unemployment 4.9%, matching expectations..

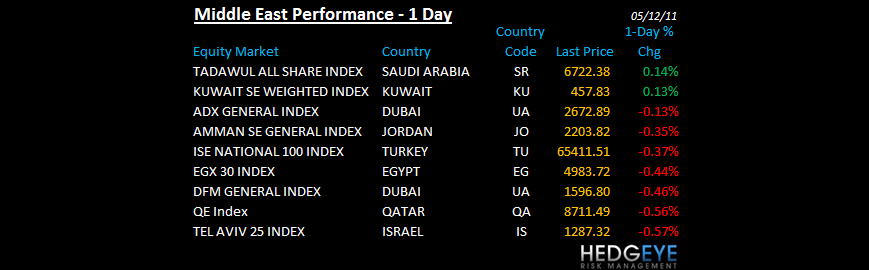

MIDDLE EAST

Howard Penney

Managing Director