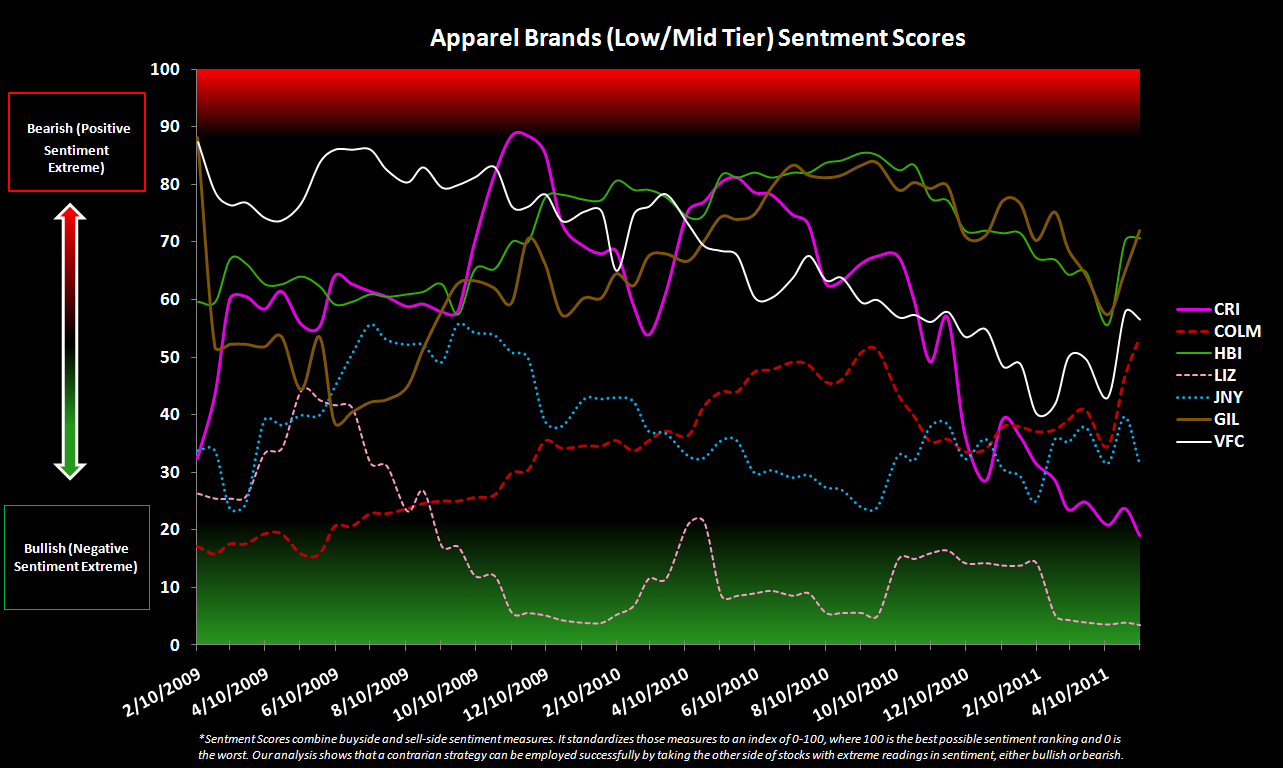

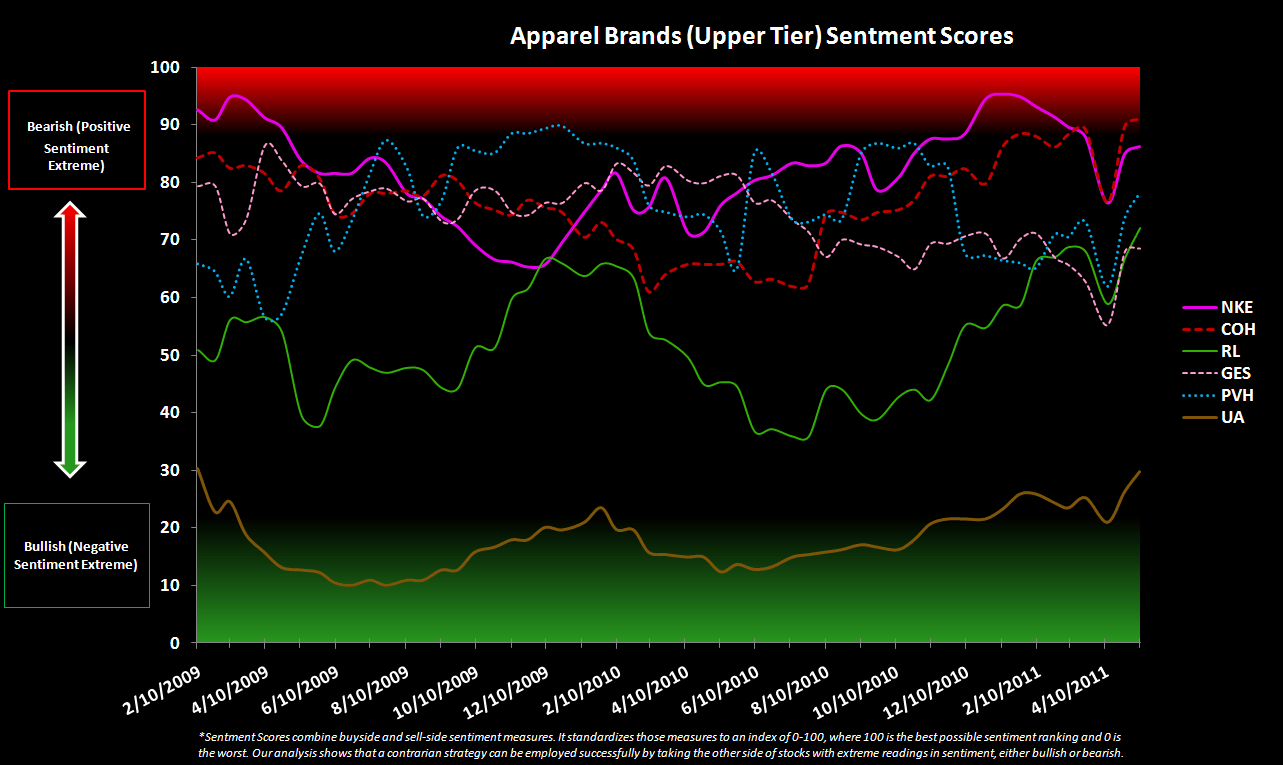

Our Hedgeye Retail Sentiment Scorecard flagged some interesting changes on the margin. Those with a rapid rise in sentiment -- TGT, GIL, HBI, COH, KSS, FL, HD, LOW are paired against those with sequential erosion, like URBN – or no sentiment at all. Yes, that’s LIZ.

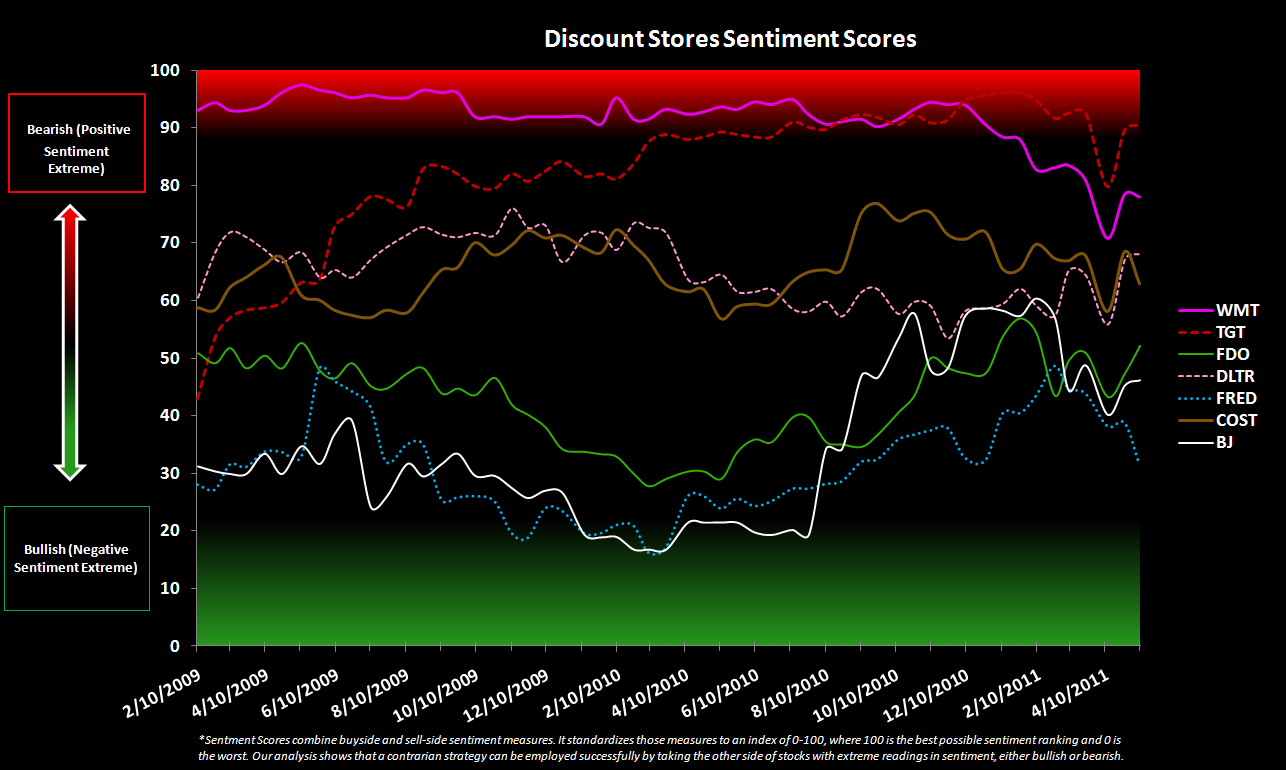

Today we are publishing our Hedgeye Sentiment Scoreboard in conjunction with the release of short interest data last night. Our Scoreboard combines buyside and sell-side sentiment measures. It standardizes those measures to an index of 0-100, where 100 is the best possible sentiment ranking and 0 is the worst. It’s probably no surprise that once sentiment reaches these extreme levels, it becomes a very asymmetrical setup wherein expectations become sky high or rock bottom and failure to meet those expectations is more probable than not. They’re not perfect, but they definitely give us a better sense to “fish where the fish are” across the retail landscape. Thanks to Josh Steiner and Allison Kaptur who created this system for the Financials group.

Here are some important notables:

TGT: The street continues to cling on to hope here. With a sentiment score of 90, TGT pierced the 9-barrier.

URBN: You can drive a truck through the bull vs bear case on this one. With a 10 point decline in sentiment over the past 2 weeks, the ‘expectations pendulum’ is starting to swing into favor for a potential bull case.

LIZ: This thing has a score of 5. No kidding. Hardly anyone comes close. Even after the company’s earnings release and analyst meeting – people still won’t give it a second look. Still one of our favorites.

GIL/HBI: As evidence that the market is looking right through raw materials as ‘yesterday’s news’ HBI and GIL are sitting there with sentiment scores of around 70.

COH: The only company to have a higher score than TGT with a 91 ranking.

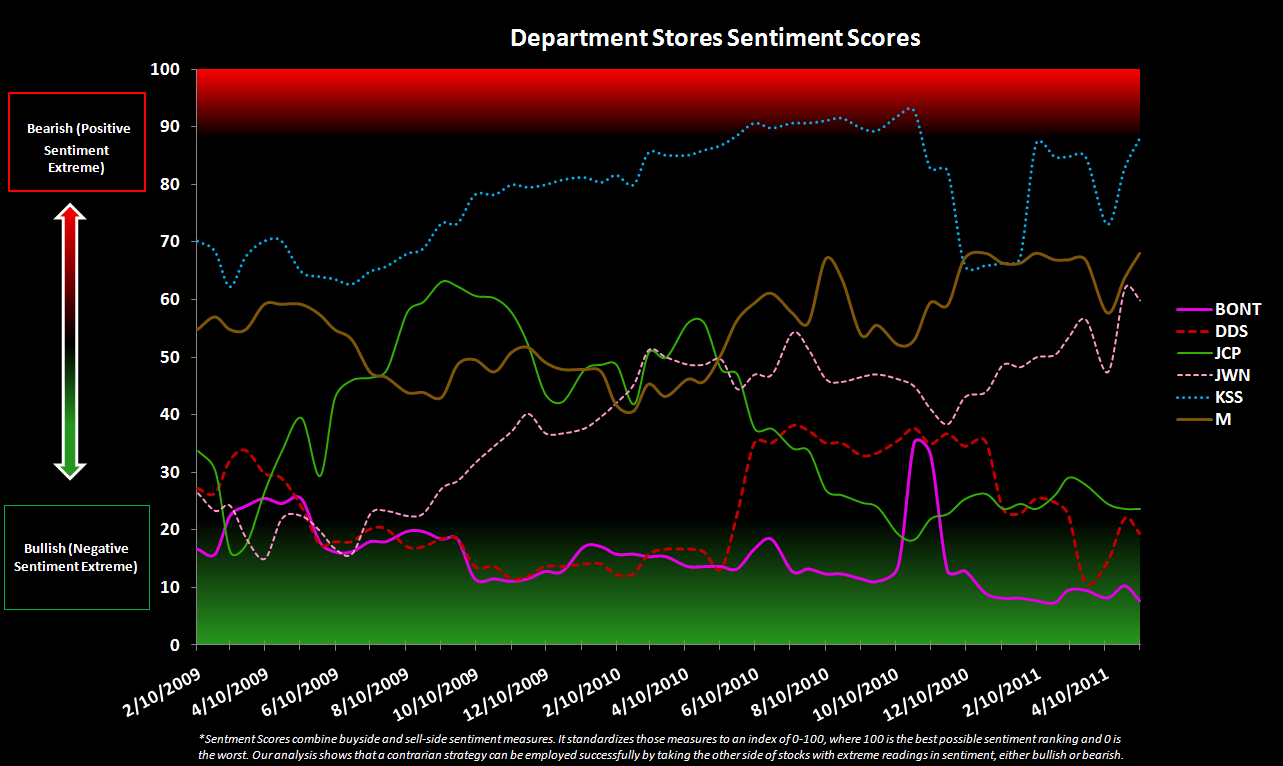

KSS: Score of 89, and recently headed higher. Recent trend mirrors Macy’s, actually, but 20 points higher. KSS is a great retailer, but it is very close to a sentiment level that our model suggests is ‘extremely positive.’

FL: At its highest level in recent history – though still at just 67. If the story works like we think it will, then more people will climb aboard. This does, however, put pressure on Foot Locker next week to put up something better than the Street’s 5% comp expectation.

Home: While not a massive divergence, it’s interesting to see that HD and LOW have turned in sequentially higher sentiment scores, while BBBY, WSM and even BBY all turned down.