If you were short WEN going into yesterday’s earnings release purely based on the company missing the quarter, it proved to be a mistake. For the most part, the market is shrugging off declining numbers due to commodity inflation. What can’t be ignored is the trend in top line sales. For now, WEN is given a pass on current sales trends because its core momentum should appear in 2H11.

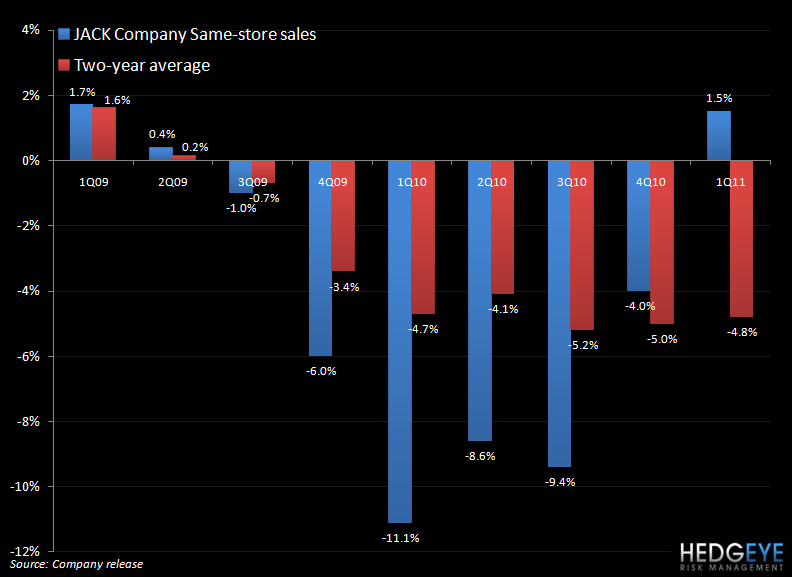

I’m not so sure that is the case with JACK. Yes, management’s number one priority this year is to drive sales and traffic at Jack in the Box through investments to enhance food, service and facilities. The current investments are depressing margins, so without a corresponding lift in sales the stock will be in the penalty box. In 2Q11, same-store sales comparisons are easy; comps declined -8.6% in 2Q10. However, the competition is strong, and gaining incremental share will be difficult for JACK.

For 2Q11, guidance is for same-store sales for Jack in the Box company restaurants to range from flat to down 2% and system-wide same-store sales for Qdoba to increase 3% to 5%. Management guidance reflects sales trends early in the quarter, which has included some unfavorable weather in many markets, particularly Texas which represents 27% of Jack in the Box company restaurants.

RELAVANT EARNINGS CALL COMMENTARY

“In 1Q11 operating margin decreased 170 basis points to 12.6% of sales, driven by commodity inflation of approximately 2.3% compared to 7% deflation in last year's first quarter. Rising beef costs were the biggest contributor, up 10.6% versus our expectations of 9% inflation and compared to 19% deflation in last year's first quarter. We also saw significant increases for cheese, pork, dairy and shortening.”

“In November, we were forecasting commodity costs for the full year to increase by 1% to 2%. Based on the increases we've seen in most commodities since that time, we are now expecting full year commodity inflation to be 3% to 4%.”

“Specific to our major commodity purchases, produce is having the biggest single impact on our expectations. Beef accounts for more than 20% of spending. For the full year, we are now anticipating beef costs to be up nearly 9% versus our previous expectations of 6% to 7% inflation. We expect beef costs to be up approximately 10% in the second quarter compared to a decrease of 9% in the second quarter 2010.”

“We expect 50s to average in the $0.85 per pound range in Q2 versus $0.78 last year. Cheese also accounts for about 6% of our spend and is now expected to be up 13% for the year versus our forecast of 7% to 8% inflation due to higher butter prices, which are up 43% year-over-year and stronger cheddar prices overseas. Dairy costs, which are over 3% of our spend, are also being impacted by the higher butter prices and are now forecasted to be up 5% for the full year.”

“Overall commodity costs are now expected to increase 3% to 4% for the full year. Restaurant operating margin for the full year is expected to range from 13% to 14%, depending on same-store sales and commodity inflation. And while the closure of the 40 restaurants last year will have a positive impact on margins, we expect this to be more than offset by commodity inflation, improvements to our core products and guest service initiatives.”

"When looking at the guidance and how that relates to pricing, guidance implies a significant improvement in that year-over-year company restaurant margin trend from down 170 in first quarter to get to the - in the next three quarters in order to get to the midpoint of the margin guidance."

Howard Penney

Managing Director