Macy’s quarter was impressive in so many ways. But we wonder if doubling its dividend will be its ‘Jump the Shark’ moment given imminent industry margin pressures. GIL beat, and showed us how a big slowdown in the core can be masked by an acquisition.

Two events this morning that are notable.

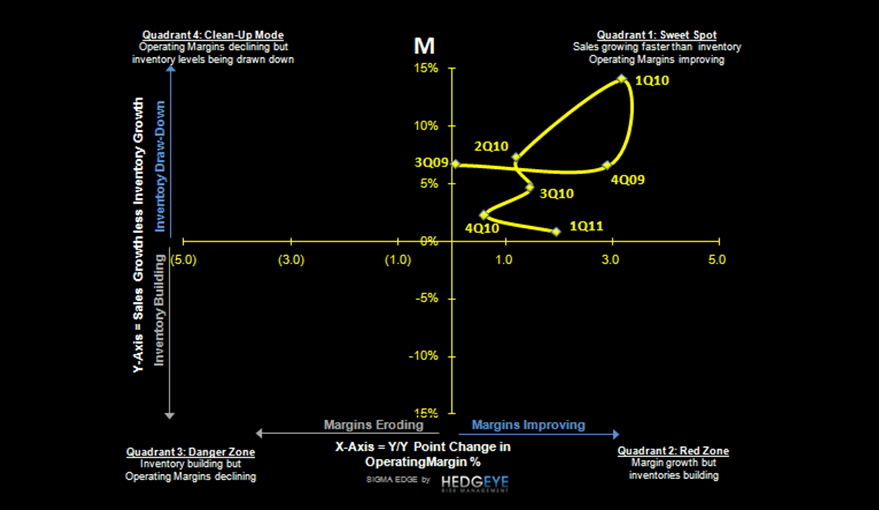

1) Macy’s blowing out the quarter. This has been a consensus long, but even the numbers put up today beat the high end of expectations. Take note of the SIGMA, specifically. The company ended its FY11 with the triangulation between sales, inventories and margins headed in a downward slope, and directed clearly towards the lower left quadrant – which is like death from a profitability standpoint. But instead, it acted like a well-run, mature business by matching sales and inventories very tightly, keeping gross margins in check and leveraging a lsd growth rate in SG&A. Financial management has always been strong at Macy’s. But this one really stands out.

So here’s the question. Due to its success, Macy’s doubled its dividend. Are we going to look back at this day in another six months (and thereafter) and view this as the watershed moment when a management team from a major company was so confident in the path that lies ahead that it committed to permanently deploy capital in a way that it COULD, rather than when it SHOULD?

2) Gildan printed $0.53 vs the Street at $0.49. Netting out a $0.05 tax benefit, and adding back about a $0.03 disposal charge for a corporate jet, they came in at $0.51. The company guided up for the year due to amongst other things its recent acquisition of Gold Toe and lower tax rate, both of which are nice. But three things on a collective basis were quite frightening: 1) socks were down 24% due to lower retailer replenishment – showing how volatile that category can be, 2) the screenprinting business softened in April. Broder indicated it on its call, and Gildan confirmed it today, 3) though GIL seems to have a better handle on cotton procurement, gross margin risk is still clearly present. GIL in aggregate had 29% inventory growth for the quarter, showing the worst spread relative to sales we’ve seen in years. And this comes in conjunction with distributor inventories up 52% and in a category where GIL has 63% market share.

When the Gold Toe acquisition was announced, we raised questions about the base business, and whether this deal was made to mask a slowdown in its core. We now think the answer is ‘Yes.’ It’s still a good deal, but the timing still smells punk to us. Management is still aggressively looking for more deals. The big question from here is if the market will pay for these new brands to come in and, in part, cannibalize and upgrade existing product. We’re not sure. The beauty of this model in the past has been one of executing a commodity business. They’ve done it masterfully, but are now headed into uncharted waters. We’re taking up our risk premium in this model.