TODAY’S S&P 500 SET-UP - May 11, 2011

The three items of focus this morning;

- Chinese Growth Slowing is a year old – Chinese inflation slowing sequentially is new “news” to the Street, but a core component of why we are bullish on China for the back half of 2012 (CPI and PPI slowed sequentially in April to +5.3% and +6.8%, respectively)

- Growth oriented inflation readings in the commodity market (supply/demand, Copper, Cotton, etc) continue to negatively diverge from monetary inflation (Gold up again this morning to $1524, breaking out above an important line of resistance at $1521)

- US stock market sentiment comes in hot from what I called out in my midweek note last week (that’s bullish on the margin); Investor Intelligence spread narrows by 400 bps w/w to 32.5 w/ Bulls dropping w/w to 51% from 55% (after stocks and commodities sold off)

As we look at today’s set up for the S&P 500, the range is 35 points or -1.56% downside to 1336 and 1.02% upside to 1371.

SECTOR AND GLOBAL PERFORMANCE

The Hedgeye models now have 7 of 9 S&P Sectors bullish TRADE and 8 of 9 bearish TREND. The XLF is the only sector broken on both durations.

<CHART11>

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1895 (+714)

- VOLUME: NYSE 835.48 (7.27%)

- VIX: 15.91 -7.28% YTD PERFORMANCE: -10.37%

- SPX PUT/CALL RATIO: 1.54 from 1.94 (-20.5%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.87

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 3.23 from 3.17

- YIELD CURVE: 2.64 from 2.60

MACRO DATA POINTS:

- 7 a.m.: MBA Mortgage Applications, prior 4.0%

- 8:30 a.m.: WASDE grains

- 8:30 a.m.: Trade balance, est. (-$47.0b), prior (-$45.8b)

- 10:30 a.m.: DoE inventories

- 12:15 p.m.: Fed’s Lockhart speaks in Atlanta

- 1 p.m.: U.S. to sell $24b in 10-yr notes

- 1 p.m.: Fed’s Kocherlakota to speak in N.Y.

- 1 p.m.: Fed’s Pianalto speaks in Cincinnati

- 2 p.m.: Monthly budget statement, est. (-$41.0b)

WHAT TO WATCH:

- Bullish sentiment decreases to 51.1% from 54.9% in the latest US Investor's Intelligence poll

- BOE says later in 2011 there's a good chance CPI will reach 5%; more likely than not to exceed 2% throughout 2012 -- wires

- FDA orders hip makers to conduct studies of the implants - NYT

- Record labels asked Google for upfront payments of $75-100M for licenses for Music Beta - NY Post, citing source

- AIG offering to be about $9B - WSJ

- Banks put forward $5B number to end foreclosure probe - WSJ

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- World Sugar Market to See Surplus for Second Year, Lowering Costs for Coke

- Biggest Oil-Gas Premium May Spur North America LNG Exports: Energy Markets

- Copper Drops as Chinese Inflation Figures Stoke Policy-Tightening Concern

- Gold Climbs for a Fourth Day on Chinese Inflation, European Debt Concern

- Corn Advances Before USDA Stockpile Estimate; Wheat Gains for Fourth Day

- Sugar Falls as Production Rises in India, Thailand; Cocoa, Coffee Slide

- Sugar Output in India’s Top Producer May Reach a Record on Cane Harvests

- Rubber in Tokyo Reaches One-Week High as Oil Gains, China May Boost Orders

- Brazil May Become Net Aluminum Importer on World Cup-Fueled Metals Demand

- Sugar Production in China Almost Flat Spurs Speculation of Rising Imports

- Barrick’s Munk Says ‘Unorthodox’ Equinox Deal Will Help Fund Gold Mines

- Silver Still Poised to Rally to $50, Merrill Forecasts: Technical Analysis

- Ethiopia May Ban Coffee Exporters Caught Hoarding, Defaulting on Contracts

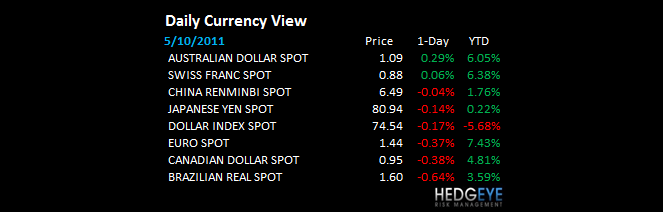

CURRENCIES

EUROPEAN MARKETS

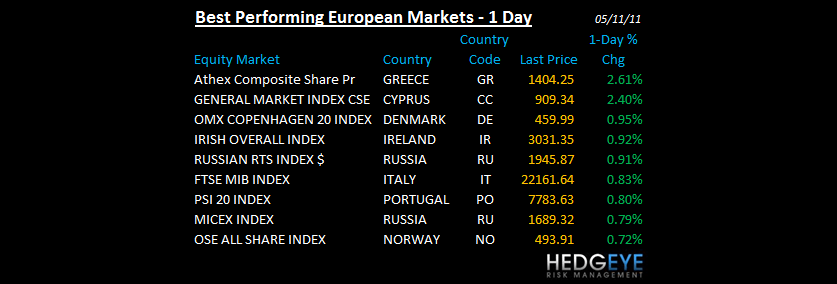

- European markets are generally higher with Greece and Spain two of the best performing markets

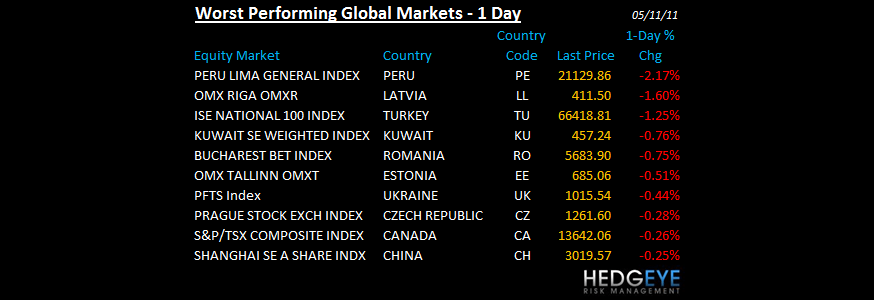

- Latvia and Turkey are notable underperformers

- Germany Apr final CPI +2.4% y/y vs consensus +2.4% and prior +2.4%; Germany Apr final CPI +0.2% m/m vs consensus +0.2% and prior +0.2%

ASIAN MARKETS

- China April CPI +5.3% y/y vs consensus +5.2% - Dow Jones; April PPI +6.8% y/y vs consensus +7.0%

- Asia traded higher; China was a notable underperformer

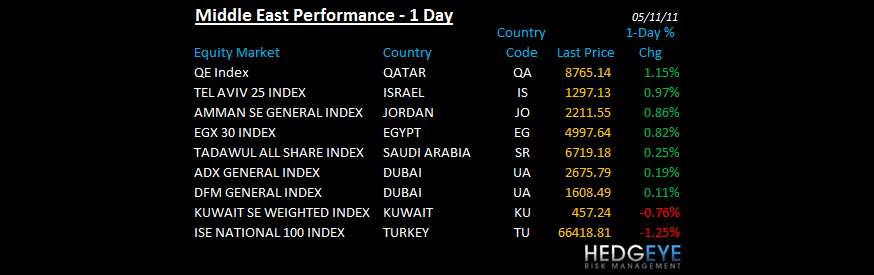

MIDDLE EAST

Howard Penney

Managing Director