Commodities are taking center-stage this earnings season with many companies raising commodity inflation targets for the year.

Specifically this earnings season, we have seen the vast majority of companies increase guidance for 2011 commodity inflation. This past week saw a downturn in many commodities as precious metals led the way with a violent snap back. From Friday, however, commodities have bounced back and for agricultural commodities at least, the preponderance of the fundamentals point to the upside.

WEN increased the mid-point of its inflation target for 2011 by 250 basis points to 5-6% on the back of beef cost concerns. With grains moving higher, the outlook for beef is not favorable and many companies may have guided conservatively in this regard. Of course, the direction of the US Dollar is critical in this discussion and – for now – our Macro Team’s view is that the policy, rhetoric, and calendar all point to further weakening of the buck over the intermediate term TREND.

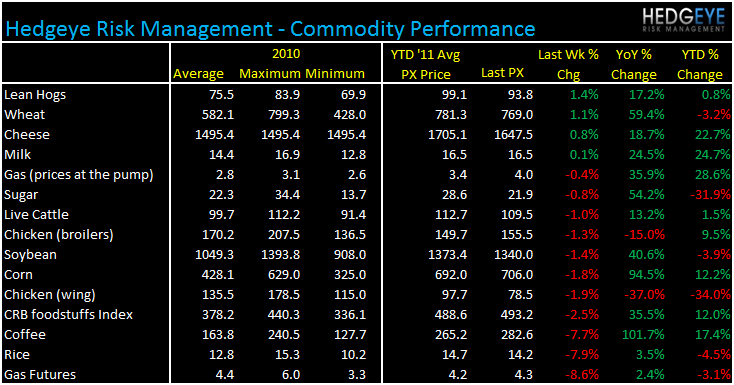

The table below details the commodities we track, ordered by magnitude of the most recent weekly price move:

Below I detail three significant commodities that have made significant moves week-over-week.

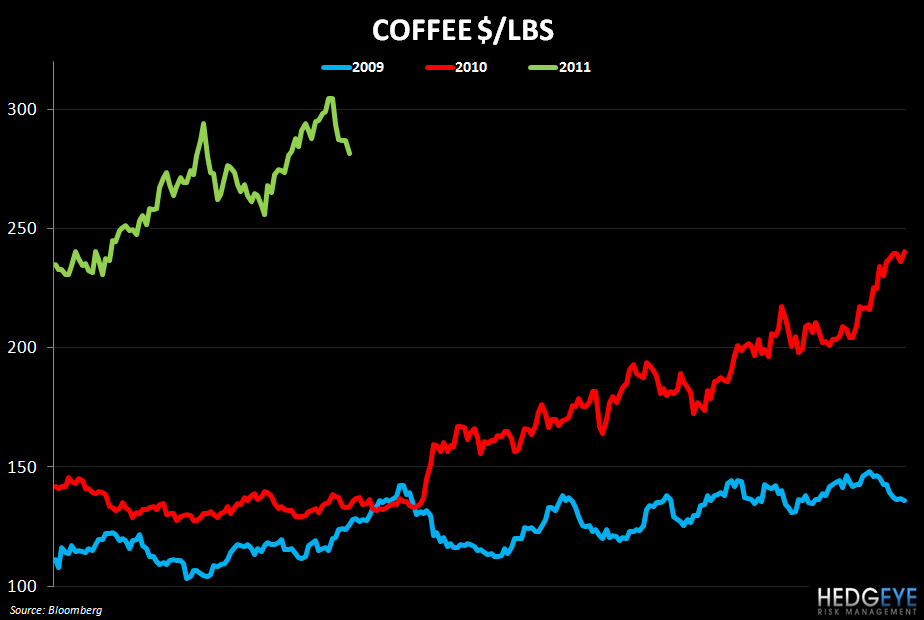

Coffee

Coffee prices abated somewhat over the last week, declining by 7.7% as numbers from Brazil suggest that production during the 2011/2012 Arabica Season may exceed expectations. However, near-term catalysts may still cause additional volatility such as mudslides in Venezuela and other weather-related events. In general, consensus is suggesting that the upcoming crop will be far better than last year’s. However, as the chart below shows, there is a severe level of inflation in the price of coffee and any near-term shocks could further squeeze the coffee concepts and bring about further price increases.

Wheat

Wheat prices gained on what was a soft week, overall for commodities. A severe drought in Russia had a severe impact on wheat prices in 2010 and now, it seems, adverse weather conditions from Asia to Europe to North America is impacting global wheat crop yields. Due to excess rain, corn planting in the U.S. is advancing at half of last year’s pace because of excess rains, according to government data. PNRA has its wheat costs locked for 2011 but, to the extent that prices continue to gain, the laddering mechanism by which they purchase their wheat could bring pressure to the cost of sales line.

Chicken wings

Chicken wings continue to March lower week-over-week. Wings are down 37% year-over-year. Excluding chicken wings and broilers, the commodities in our commodity monitor table are up an average of 39% year-over-year.

Howard Penney

Managing Director