Notable news items and price action from the past twenty-fours along with our fundamental view on select names.

- DRI’s Olive Garden received a warning but no fine following a Florida state investigation into how a toddler was accidentally served sangria at a Lakeland restaurant.

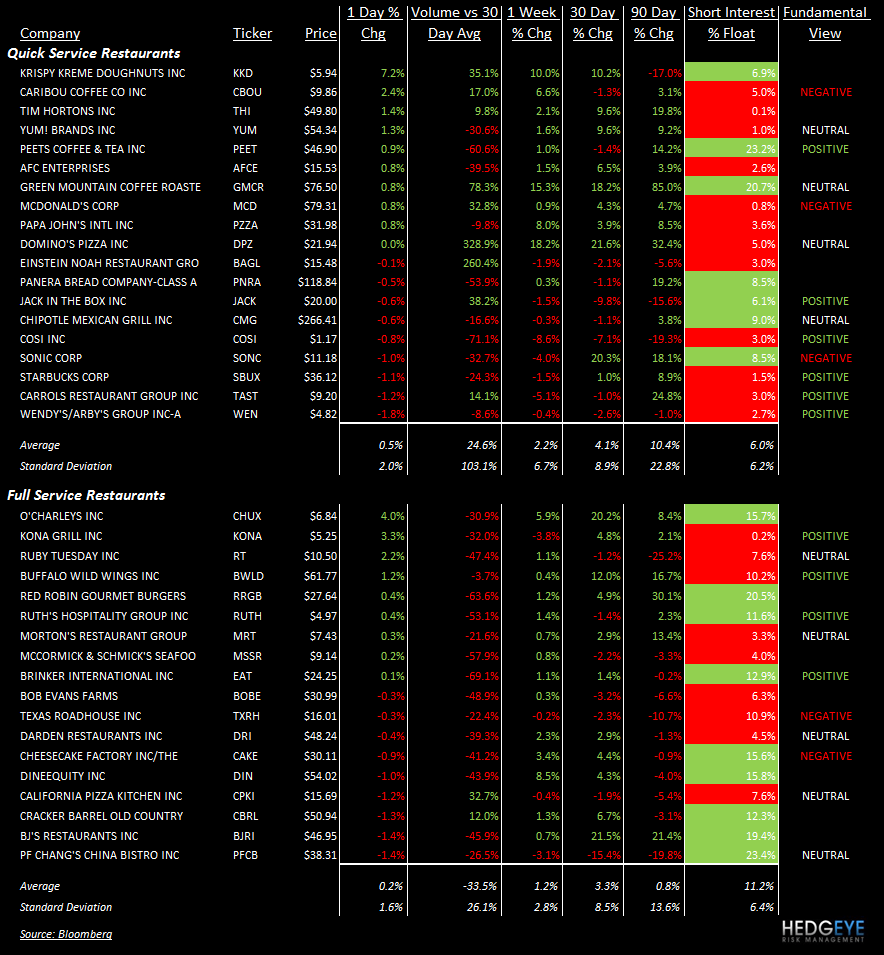

- TAST reported 1Q11 EPS of $0.10 versus consensus at $0.12. Comparable restaurant sales increased 13.5% at Pollo Tropical, 2.0% at Taco Cabana, but decreased 5.0% at Burger King. Guidance is for comps to come in at +6-8% at Pollo Tropical (versus 3-5% previously) and to increase 2-3% at Taco Cabana (versus 1-2% previously). Burger King comparable sales are expected to be negative for the full year but improving in 2H11.

- TAST declined 1.2% on accelerating volume yesterday, ahead of the earnings miss.

- KKD gained 7.2% on accelerating volume.

- CPKI and CBRL declined on accelerating volume.

Howard Penney

Managing Director