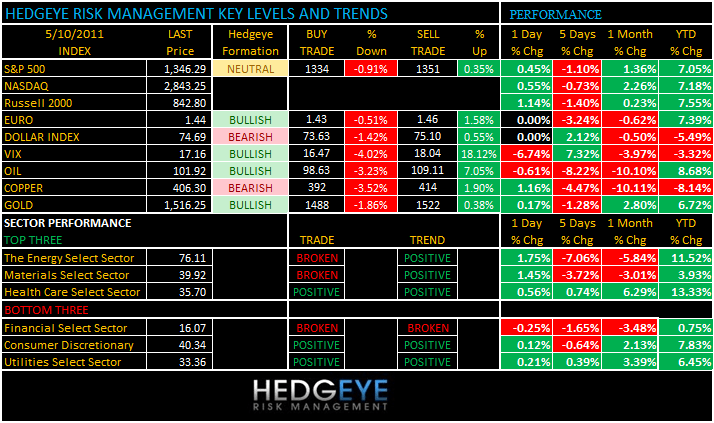

TODAY’S S&P 500 SET-UP - May 10, 2011

Yesterday, we saw the USD down to start the week (down for the 15th week of the last 20), which had CRB Index ripping yesterday (+2.1%) after getting crushed last week (down -8.9% for the wk). Oil moved back above our intermediate-term TREND line of support = $98.63 and Gold continues to look better than almost everything that’s big and liquid other than maybe the German DAX. As we look at today’s set up for the S&P 500, the range is 17 points or -0.99% downside to 1334 and 0.35% upside to 1351.

SECTOR AND GLOBAL PERFORMANCE

The Hedgeye models now have 7 of 9 S&P Sectors bullish TRADE and 8 of 9 bearish TREND. The XLF is the only sector broken on both durations.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1181 (+188)

- VOLUME: NYSE 778.48 (-24.18%)

- VIX: 17.16 -6.47% YTD PERFORMANCE: -3.32%

- SPX PUT/CALL RATIO: 1.94 from 1.85 (+4.61%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 24.55 -1.521 (-5.834%)

- 3-MONTH T-BILL YIELD: 0.03% +0.01%

- 10-Year: 3.17 from 3.19

- YIELD CURVE: 2.60 from 2.62

MACRO DATA POINTS:

- 7:30 a.m.: NFIB Small Business, est. 91.8, prior 91.9

- 7:45 a.m.: ICSC-Goldman weekly retail sales

- 8:30 a.m.: Import price, est. 1.8% (M/m), prior 2.7%

- 9:30 a.m.: Fed’s Duke speaks in St. Louis

- 10 a.m.: Wholesale inventories, est. 1.0%, prior 1.0%

- 11:30 a.m.: U.S. to sell $28b 4-wk bills

- 12 noon: DoE short-term energy outlook

- 12:45 a.m.: Fed’s Lacker speaks on Arlington, Vir.

- 1 p.m.: U.S. to sell $32b in 3-yr notes

- 4:30 p.m.: API inventories

WHAT TO WATCH:

- China’s April inflation data due out tomorrow.

- Microsoft close to completing $7B for Skype - WSJ

- Google online music service to probably be announced tomorrow at Google I/O developers conference - WSJ

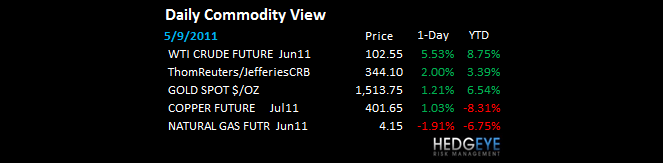

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Crop Weather Damage Grows as Europe Drought, Canada Rain Boost Grain Costs

- Oil Inventories Increase to Near a Two-Year High in Survey: Energy Markets

- Sugar Rises Most in Six Weeks as Imports Into China May Jump; Cocoa Gains

- Wheat Gains for Third Day as Adverse Weather Threatens Harvests Worldwide

- Copper Climbs for a Third Day Before Release of Figures on China Inflation

- Copper Imports by China Decline on Ample Supplies, Higher Overseas Prices

- Gold May Advance as Sovereign-Finance Concern Stokes Demand; Silver Gains

- Malaysia Smelting Climbs to Three-Month High as Tin Prices Produce Profit

- Mississippi Flooding Threatens Cropland, Refineries and Shipping Traffic

- Soybean Imports by China Tumble on Canceled Orders as Stockpiles Stay High

- Palm Oil Stockpiles, Output Reach Six-Month High in Malaysia on Weather

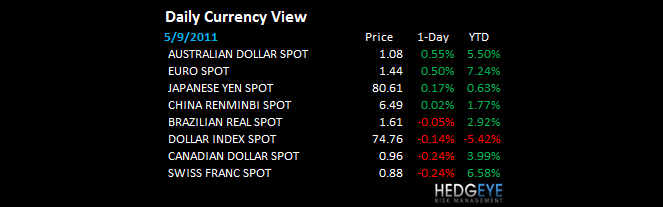

CURRENCIES

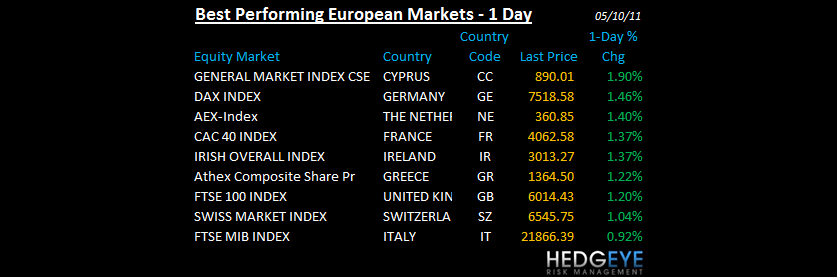

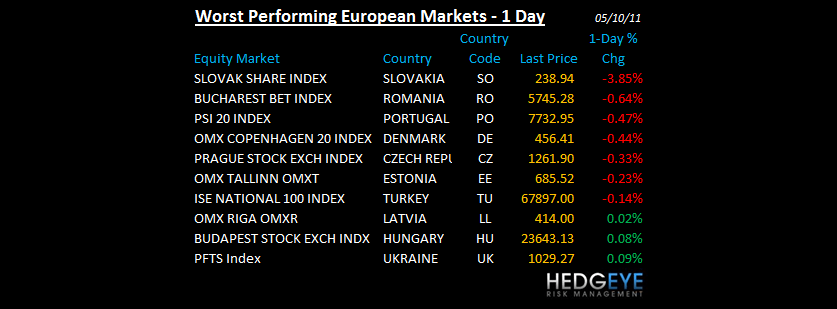

EUROPEAN MARKETS

- Greek banks jump on talk country to avoid debt restructuring. But…

- Greece denies report it is discussing new aid package -- Reuters, citing Greek Finance Minister

- France Mar Industrial output (0.9%) m/m vs consensus +0.4%

ASIAN MARKETS

- Most Asian markets that were open today ended a higher

- Hong Kong was closed for Buddha’s Birthday.

- South Korea was closed for Sukka Tansin II.

- China April trade surplus $11.4B vs consensus $1-3B. Australia March trade balance A$1.74B vs consensus A$500M.

MIDDLE EAST

Howard Penney

Managing Director