Positions in Europe: Long British Pound (FXB); Germany (EWG)

As we discussed in a note on Friday titled “Greece Leaving the EURO, Not so Fast”, fears swirled on Friday afternoon that Greece had plans to leave the Eurozone based on unconfirmed sources reported by the German publication Spiegel Online. As we expected, and as was confirmed over the weekend, this claim was a complete fabrication. However, the abruptly called meeting of finance minister on Friday in Luxembourg did focus on Greece’s persistent public debt imbalances. Of the few remarks we’ve received out of the meeting, it appears that a modification of Greek debt (either through lower interest rates on outstanding debt or more favorable maturities) could be in the cards in the near term. One issue outstanding, and oft pressed by fiscally stronger peers, is increased collateral on Greece's existing debt and future issuance.

Is all the Greek news baked into the cake? The short answer is no, however Greek equities and bonds have seen a significant plunge after an eerie rise in the beginning of the year. The Greek Athex (equity) is down -21.3% since a high on February 18th (and hitting ytd lows today, trading down -1.5%) and the yield on the Greek 10YR bond has gained steadily ytd, trading at 15.6% today!

While the EUR-USD corrected -3.4% last week, the common currency has remained resilient in the face of glaring risks over the last weeks. We attribute a fair amount of this strength to the weakness in the USD, which we expect to persist as the US government wrestles with the debt ceiling debate (decision scheduled for August 2nd). We still expect to see volatility in the EUR-USD over the coming weeks, but within a tight trading range.

As Keith signaled to clients this morning, “the Euro has a ton of support at our immediate-term TRADE line of $1.43 and immediate-term upside to $1.47. Commodity markets (oil in particular is holding our TREND line of $98.63 like a champ) are betting USD down and EUR up from here in the very immediate term.” As the EU continues to throw its weight (both in terms of capital and in principle) behind maintaining the Eurozone, we expect the EUR to continue to largely shake off sovereign debt contagion fears across the region.

Catalysts to keep in minds are Eurozone Q1 GDP reports this week and next week’s meeting of Finance Ministers on May 16th.

As is typical for Mondays, below we show our European Risk Monitor charts. The first chart of sovereign cds shows that risk premiums continue to heighten in the periphery, especially from Greece, Ireland, and Portugal. With Portugal receiving a €78 billion bailout early last week, Ireland is taking the opportunity to once again plea for more favorable terms on its bailout funds, a development we don’t think the European community will acquiesce to, but is worth monitoring.

Our European Financials CDS Monitor shows that bank swaps in Europe were mostly wider week-over-week, widening for 31 of the 39 reference entities and tightening for 8. This shows a reversion from last week’s tightening, and is a reflection of the ever-present (but fluctuating) risk trade as debt contagion looms.

Today we bought back our position in Germany via the eft EWG in the Hedgeye Virtual Portfolio. We continue to see confirmation of Germany’s fundamental strength, including impressive export numbers of 7.3% in March month-over-month (vs 2.8% in February) reported today. Germany’s GDP is expect to grow around 2.6% this year, a healthy premium over many of its peers, while the country’s fiscal conservatism leaves it in a strong defensive position as sovereign debt contagion within the region persists.

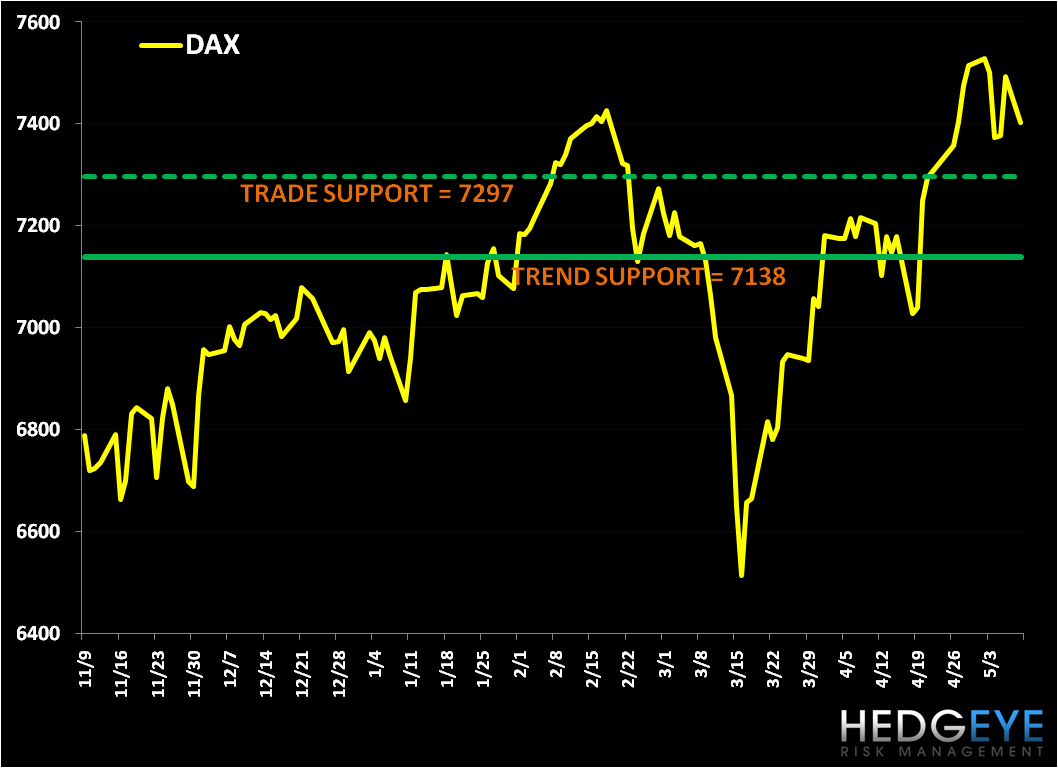

Our levels on the DAX are immediate term TRADE support at 7,297 and intermediate term TREND support at 7,138 (see chart below).

Matthew Hedrick

Analyst