Notable news items and price action from the past twenty-fours along with our fundamental view on select names.

- MCD Global sales results were released this morning. Global comps came in at +6%. U.S. comps gained 4% while Europe and APMEA both produced comps of +6.5%. The results were impacted by a calendar shift that impacted results by between 0.9% and 1.0%, depending on the area of the world.

- MCD Japan sales results revealed that April comps came in +3.6% year-over-year. 24 of the 264 doors closed due to the March earthquake/tsunami disaster.

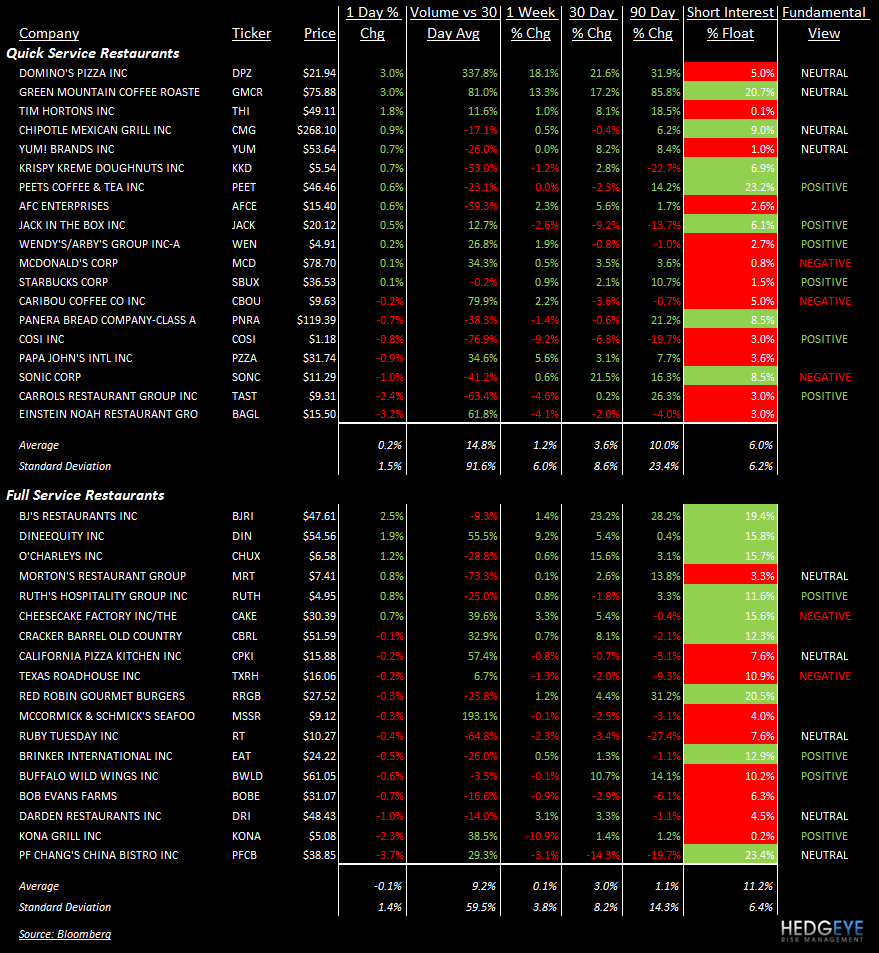

- DPZ gained 3.7% on accelerating volume. GMCR, THI, and DIN were other gainers that traded with high volume Friday.

- BAGL, KONA, and PFCB all declined on accelerating volume Friday.

Howard Penney

Managing Director