TODAY’S S&P 500 SET-UP - May 6, 2011

In the Correlation Risk post earlier this week we called out this 73.40 USD Index level as a very immediate-term trigger line. The good news is that as of yesterday, we’re through that line and the biggest wave of guys being forced to take down exposure to the most crowded macro trade (net long and gross exposure) in hedge fund history (The Inflation trade, brought to you by The Bernank). As we look at today’s set up for the S&P 500, the range is 20 points or -0.31% downside to 1331 and 1.19% upside to 1351.

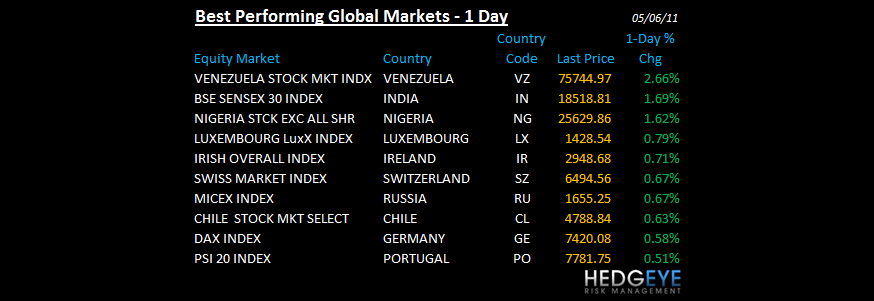

SECTOR AND GLOBAL PERFORMANCE

After yesterday’s downdraft, the Hedgeye models now have 3 of 9 S&P Sectors bearish TRADE and TREND (XLF, XLE and XLB) – they were the 1st 3 sectors to crack when we made our May Showers call in 2010 too. In order of preference, the best places to hide are long Tech (XLK) and Healthcare (XLV).

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -738 (+400)

- VOLUME: NYSE 1113.48 (+4.11%)

- VIX: 18.20 +6.56% YTD PERFORMANCE: +2.54%

- SPX PUT/CALL RATIO: 1.94 from 2.08 (-6.77%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 26.32 0.507 (1.964%)

- 3-MONTH T-BILL YIELD: 0.02% -0.01%

- 10-Year: 3.18 from 3.25

- YIELD CURVE: 2.60 from 2.65

MACRO DATA POINTS:

- 7:30 a.m.: Fed’s Yellen speaks on economic growth in Finland

- 8:30 a.m.: Payroll report

- 10 a.m.: Fed’s Dudley to speak at economic briefing in NY

- 11 a.m.: Fed’s Bullard to speak to bankers in Little Rock, Ark.

- 1 p.m.: Baker Hughes Rig Count, prior 1818

- 3 p.m.: Consumer credit, est. $5b

WHAT TO WATCH:

- US manufacturers of all sizes having trouble finding skilled workers - WSJ

- Sen Charles Schumer leaning toward backing Deutsche Boerse bid for NYSE Euronext - WSJ

- China is closely watching the debate over raising the U.S. debt ceiling and wants the Obama administration to do more to curb the deficit - Vice Finance Minister Zhu Guangyao

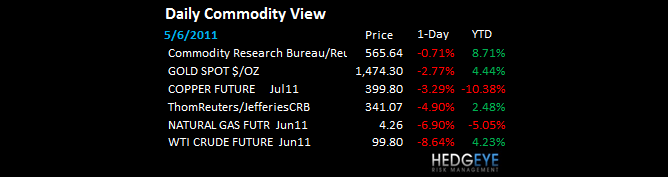

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Commodities Plunge for a Fifth Consecutive Day on ‘Panic’ Among Investors

- Crude Oil Falls a Fifth Day; Poised for Biggest Weekly Decline Since 2008

- Silver Set for Worst Weekly Drop Since 1975 Amid Rout in Commodity Prices

- Copper Heads for Largest Drop in Eight Weeks as Central Banks Raise Rates

- Corn, Soybeans Drop as Investors Bet Demand Will Dry Up on Higher Prices

- Coffee Falls as Rising Robusta Stockpiles Cap Rally; Sugar, Cocoa Slide

- Oil Bubble Pops as Bin Laden Death Triggers Four-Day Rout: Energy Markets

- Palm Oil Futures Plunge for a Third Day, Tracking Decline in Commodities

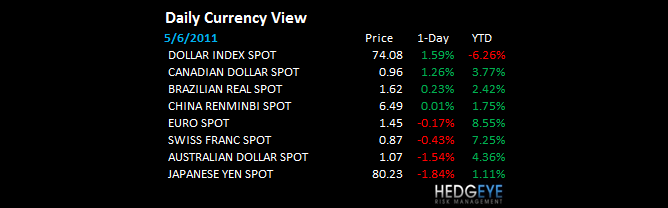

CURRENCIES

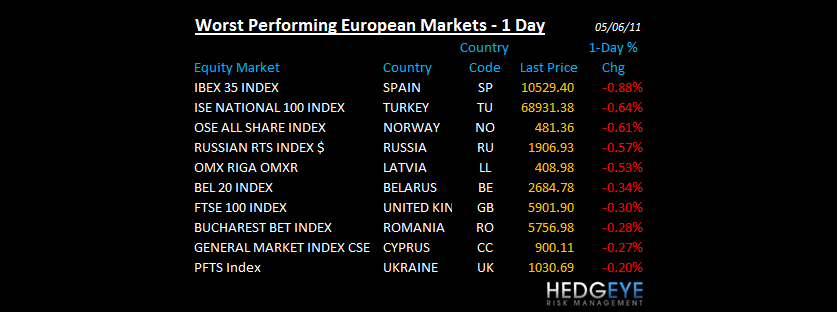

EUROPEAN MARKETS

- European equity markets trading flat to lower

- Germany Mar Industrial output +0.7% m/m vs consensus +0.5% and prior +1.7% revised from +1.6%

- UK Apr PPI: input +17.6% vs consensus +16.3%; output +5.3% vs consensus +5.1%; core output +3.4% vs consensus +3.0%

- Spain GDP +0.2% in 1Q11, matching the 4Q10 growth rate, and +0.7% YoY - The Bank of Spain

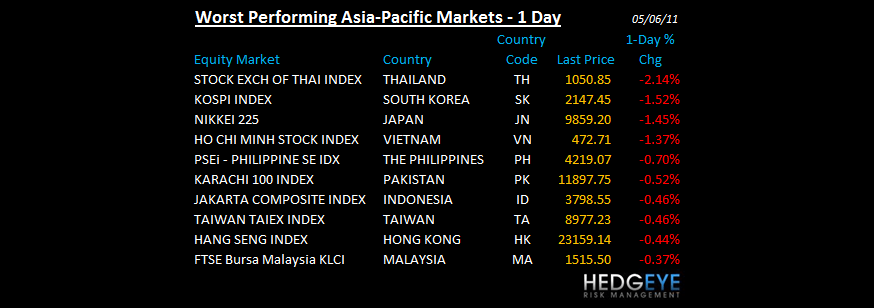

ASIA MARKETS

- Asian markets mostly lower, with commodity stocks hurt by lower oil and metals prices.

- Australia’s dollar strengthened the most in two weeks after the Reserve Bank increased forecasts for inflation and said higher interest rates may be required “at some point.” @Bloomberg

MIDDLE EAST

Howard Penney

Managing Director